A popular lemon-lime flavored soda once adopted an advertising slogan positioning the product as the “uncola.” That slogan was powerful in the 1970s to set the product apart – and can have value for us today when it comes to retirement planning. Think of “uncola” as no-COLA or low-COLA – as in retirement plans with no (or low) Cost of Living Adjustments (COLAs). COLAs can have a big impact on income streams in retirement and have implications for their portfolio. Don’t let your clients get caught-out for not having factored them in when planning.

When modeling a retirement income plan, the importance of long-term assumptions – such as capital market forecasts and longevity – are obvious. It’s clear that market returns and the time horizon the plan is designed to cover will influence the sustainability of the plan. Less obvious, but still critical, are assumptions about inflation and cost-of-living-adjustments (COLAs).

Inflation ≠ COLA

First, let’s be clear that inflation and cost-of-living-adjustments are not one and the same, even though the terms are often used interchangeably. There are important distinctions between the two.

- Inflation is an increase in future prices that erodes the purchasing power of a consumer. It’s typically assessed on an ongoing basis through mechanisms like the Consumer Price Index (CPI).

- A cost-of-living-adjustment (COLA) is a periodic adjustment made to an income stream or a spending goal that is designed to offset some or all of the effects of future inflation. COLAs may be assessed and applied to income streams each year (e.g., Social Security payments) or specified in advance and applied each year regardless of the actual level of inflation (e.g., lifetime income annuities). Pensions may follow either path – or not offer any COLAs at all.

Factoring COLAs into Retirement Planning

When you’re planning, you should make sure you understand whether or not the income streams your client will receive will have COLAs. You should also assess whether or not the spending goal should have a COLA as well. It’s especially important to understand if there’s a gap between the two. The tricky thing about COLAs is that small differences compound through time, so it’s important to gauge them properly.

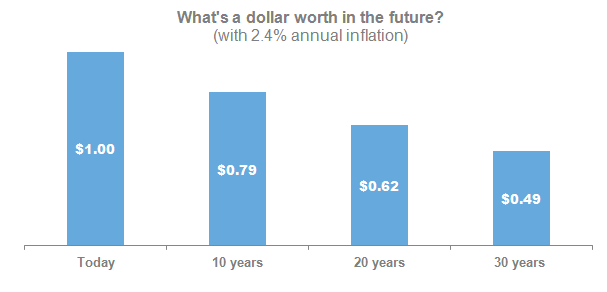

The chart below shows how much less a non-COLA-adjusted dollar of income would be worth 10, 20, or 30 years in the future. Most investors have some idea about inflation’s erosion of their purchasing power, but they may not think about the impact no-COLA or low-COLA income streams will have on their portfolios and spending goals.

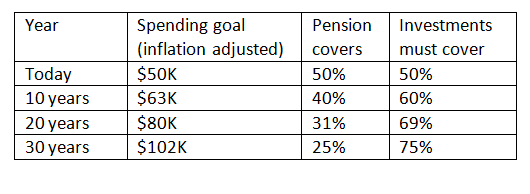

For example, consider a client who receives $25,000 a year from a pension, but the payment does not have a COLA. Assume her spending target (ignoring taxes and other complexities to keep things simple) is $50,000 a year. The amount the pension doesn’t cover will need to be met by investments. Lastly, assume that long term inflation is 2.4% (Russell’s current forecast as of 12/31/13).

In the first year, half of the $50,000 will be met by the pension benefit and half will need to come from their portfolio. In 10 years, the client will need $63,000 to maintain spending power. Pension income will only cover 40%, leaving her investments responsible for 60%. As time passes that trend magnifies.

If your clients have income streams without COLAs and you want to attempt to maintain their purchasing power through time (or at least slow down its erosion), it’s important to account for the fact that their portfolio may have to bear an increasing burden to cover the difference between their spending goal and the outside income streams they’re receiving.

Rod Greenshields is a consulting director for Russell’s U.S. advisor-sold business. To see this post in its original form, with more information and full disclosures, visit Russell's Helping Advisors blog.