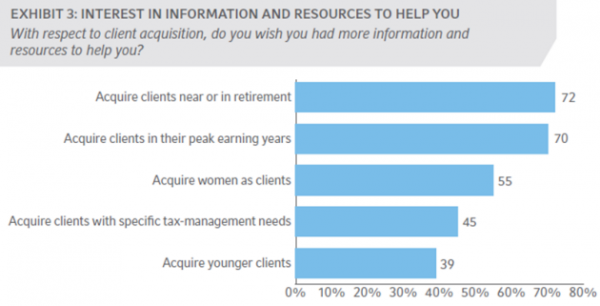

Our recently released Financial Professional Outlook survey uncovered some interesting things about advisor behavior. For example, nearly three quarters (72%) of respondents said they wanted more resources to help them acquire clients near or in retirement, or those in the decumulation phase of “net spending.” What was surprising to us was that only 39% are looking for more to help them acquire younger clients at the other end of the continuum who are in accumulation mode (net savers).

Of course, there’s nothing wrong with taking on net spenders as clients. For many advisors, retired clients represent a valuable portion of their books of business. However, there are several key risks that clients near or in retirement can pose to your business, including:

- “Decumulation risk” (the risk that clients will draw down their account to support their lifestyle in retirement at a faster rate than investment returns are able to keep growing the account value)

- “Asset flight risk” (while high net worth clients may not be subject to decumulation risk, they may be tempted to pursue private investment opportunities outside of their primary advisor’s purview)

- “Generational risk” (the risk that the primary advisor may not retain the assets after an “estate event” – i.e. when the assets transfer to the next generation).

Advisors know they can’t just focus on today – you also need to be thinking about what you want your business to look like in the future. Depending on how far out into the future you’re looking, that future might include conversations about intergenerational wealth transfers – or lack of transfers. According to Doolin, Preisser and Williams, advisors cannot afford to ignore that reality. Their 2011 research found that “more than 95% of inheritors promptly change advisors. (1) So as you might expect, the transfer of generational wealth presents huge opportunities, as well as huge challenges for the advice industry. The main takeaway here is that if you hope to retain assets after a wealth transfer, you have to work for it. It is not a “given.”

What can we learn from Arthur?

For me, our survey findings prompted a memory of a man named Arthur Lashinsky, a stock broker at one of the great old line firms. When I first met him, he was my grandfather’s broker, my father’s, and by virtue of a gift, mine as well. I don’t know if it was his nature, how he was taught, or something else but Arthur took me under his wing. He taught me some things about investing and, most importantly, took it upon himself to make sure I didn’t do something dumb (like sell low and buy high).

Arthur was old school but it seems to me that he was also ahead of his time. He was paid as a broker but acted like an advisor. He solved the generational wealth transfer problem because he figured out a way to be a partner to one generation (he and my grandfather loved to pick stocks together), an advisor to another (my dad wasn’t as interested in stock-picking), and a Dutch Uncle to a third (me).

As a result, when my grandfather died, the money changed hands but not brokers (remember, that’s what Arthur was). He continued to work with my father and me until his own death some years later. The investments he made in my father were truly no brainers. My father was at that time a very successful attorney and the inheritance simply added wealth to wealth. It wasn’t so obvious why he should invest in me − but he did. And it seems to me that it paid off for both of us.

The bottom line

How much energy should you put into winning over the children and beneficiaries of your current clients? That depends on your own time horizon because it certainly represents an investment. But whatever you do, don’t assume that you will keep the next generation and their inheritance as a matter of course.

For more findings from the latest Financial Professional Outlook, please read the full survey report.

(1) Diane Doolin, Vic Preisser, and Roy Williams, 2011. Engaging and retaining families. https://www.imca.org/sites/default/files/file_2288.pdf

Russell Financial Professional Outlook is a product of Russell Investments, produced independently of Russell’s investment and manager research services. The latest survey was fielded from June 11, 2014 and June 23, 2014.

The information contained herein has been obtained from sources that we believe to be reliable, but its accuracy and completeness cannot be guaranteed. The information, analysis and opinions expressed herein result from surveys of persons outside Russell Investments and may not represent the opinion of Russell Investments, its affiliates or subsidiaries. This report is provided for general information only and is not intended to provide specific advice or recommendations for any individual or entity.This is not an offer, solicitation or recommendation to purchase any security or the services of any organization.

Kevin Hoffberg is Managing Director of Marketing for Russell Investments’ U.S. advisor-sold business. To see this post in its original form, with more information and full disclosures, visit Russell's Helping Advisors blog.