U.S. economic data remain strong with the third quarter’s 3.5 percent GDP growth signaling that the economy is doing pretty well across the spectrum. Net exports were strong, unemployment has fallen much faster than expected, and consumer confidence is at seven-year highs. The fact that the government is contributing to GDP growth tells us that a major headwind for the economy—contracting government spending—has gone away, and I do not expect it to return.

Japan and Europe remain the train wrecks they were advertised to be. Interestingly, the slowdown in the euro zone is now concentrated at the core rather than on the periphery. As a result, we could soon witness a dramatic shift in the European political dynamic. If German politicians are worried about their own economy they will be much more willing to accept accommodative European Central Bank policies than if they are concerned about Italy.

Japan’s major increase in monetary accommodation surprised markets last Friday and came just days after the U.S. Federal Reserve ended its own quantitative easing program. The night before the so-called Halloween surprise, I was looking over some Japanese data and thought to myself that it was surely inevitable that Tokyo would increase accommodation and that doing it sooner rather than later would give them the added benefit of surprise. I never expected the announcement to come the very next day.

The takeaway from all this is that while the Fed has ended QE, the great global monetary expansion is far from over as other central banks take up the slack. The sell-off in U.S. high-yield bonds and leveraged bank loans during the third quarter has made for an attractive entry point, and while I expect to see some sort of consolidation in U.S. equities, the near-term risk is that stocks are headed higher.

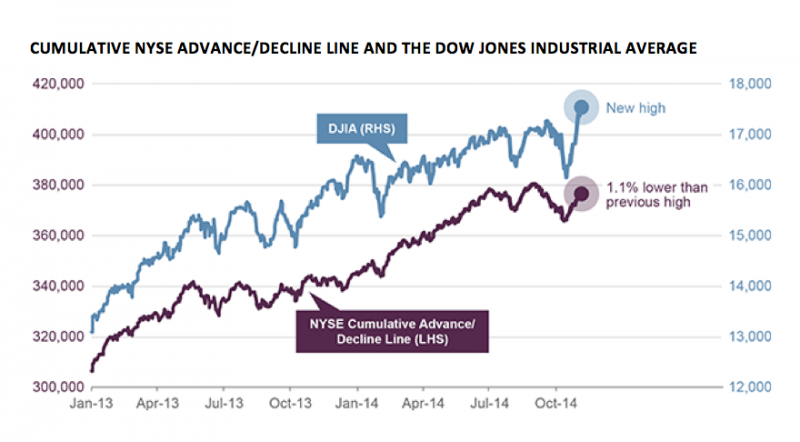

I would caution that the current rally in U.S. equities has not been confirmed in the NYSE Cumulative Advance/Decline Line and investors would be well advised to monitor this closely. The United States will likely do very well in the next six months thanks to overseas policies, but there are obstacles ahead. As the U.S. dollar strengthens and without the support of the Fed’s asset purchases, the U.S. economy will be challenged heading into the second half of 2015 to sustain its growth based on employment and wage expansion. While it would be premature to draw conclusions beyond the first quarter of next year, for now, risk assets remain the place to be. U.S. economic data remain strong with the third quarter’s 3.5 percent GDP growth signaling that the economy is doing pretty well across the spectrum. Net exports were strong, unemployment has fallen much faster than expected, and consumer confidence is at seven-year highs. The fact that the government is contributing to GDP growth tells us that a major headwind for the economy—contracting government spending—has gone away, and I do not expect it to return.

Japan and Europe remain the train wrecks they were advertised to be. Interestingly, the slowdown in the euro zone is now concentrated at the core rather than on the periphery. As a result, we could soon witness a dramatic shift in the European political dynamic. If German politicians are worried about their own economy they will be much more willing to accept accommodative European Central Bank policies than if they are concerned about Italy.

Japan’s major increase in monetary accommodation surprised markets last Friday and came just days after the U.S. Federal Reserve ended its own quantitative easing program. The night before the so-called Halloween surprise, I was looking over some Japanese data and thought to myself that it was surely inevitable that Tokyo would increase accommodation and that doing it sooner rather than later would give them the added benefit of surprise. I never expected the announcement to come the very next day.

The takeaway from all this is that while the Fed has ended QE, the great global monetary expansion is far from over as other central banks take up the slack. The sell-off in U.S. high-yield bonds and leveraged bank loans during the third quarter has made for an attractive entry point, and while I expect to see some sort of consolidation in U.S. equities, the near-term risk is that stocks are headed higher.

I would caution that the current rally in U.S. equities has not been confirmed in the NYSE Cumulative Advance/Decline Line and investors would be well advised to monitor this closely. The United States will likely do very well in the next six months thanks to overseas policies, but there are obstacles ahead. As the U.S. dollar strengthens and without the support of the Fed’s asset purchases, the U.S. economy will be challenged heading into the second half of 2015 to sustain its growth based on employment and wage expansion. While it would be premature to draw conclusions beyond the first quarter of next year, for now, risk assets remain the place to be.

Can U.S. Equities Sustain this Rally?

Despite the Dow Jones Industrial Average high made on Nov. 6, the New York Stock Exchange Cumulative Advance/Decline Line remains 1.1 percent lower than its peak on Aug. 29. Historically, a persistent divergence between the DJIA and the Advance/Decline Line usually leads to a major correction in equities. Whether or not the Advance/Decline Line can catch up with the increase in equity prices over the next few weeks will determine whether the current rally is sustainable.

Source: Bloomberg, Guggenheim Investments. Data as of 11/6/2014.

This material is distributed for informational purposes only and should not be considered as investing advice or a recommendation of any particular security, strategy or investment product. This article contains opinions of the author but not necessarily those of Guggenheim Partners or its subsidiaries. The author’s opinions are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. ©2014, Guggenheim Partners. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

Scott Minerd is Chairman of Investments and Global Chief Investment Officer at Guggenheim Partners

{kind=link}