This blog could be an easy one: cut and paste. Not much has changed since we laid the foundation for our first edition of Pump Up the Vol in October of last year, at a time when financial markets appeared to be falling apart. It was also an attempt to clean up my perceived image as a negative market observer; let’s start with this point for our sequel, before revisiting “American exceptionalism” with respect to domestic economic performance, and a seemingly crumbling world around us.

Some of the smartest people I know in finance, who I have come to respect and appreciate over the years, have failed in their assessment of the tremendous bull market in stocks since 2009. Sure enough, everyone that called for being “all in” is considered today's genius—fair, but so far inconclusive. At one point, we all must recognize that we are still participants in one of the greatest financial experiments ever conducted, and that many of the outcomes have not been anchored in sound fundamentals, but rather in the availability of inexpensive money along with global policymakers’ suppression of “natural” market outcomes and volatility. The process of normalization will have to take place, sooner or later.

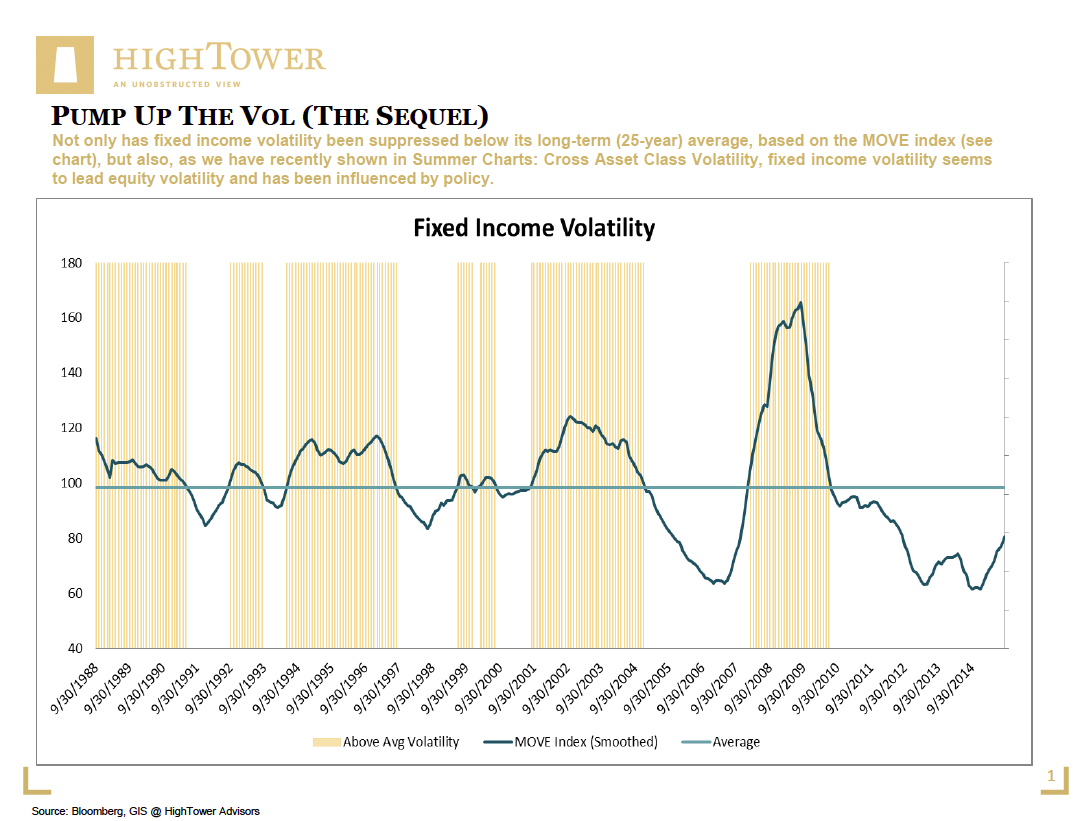

It is almost laughable how investors have become fearful over the past weeks, thinking we have just seen the “big one” (i.e., a correction of severe magnitude), but at the time of my writing, the market (when measured by the S&P 500) is only trading about 8.5 percent below its record closing high of 2132 points set on July 20th of this year. In fact, in measuring volatility patterns over long periods of time, financial markets in the U.S. (equity and fixed income alike) are destined to adjust to more realistic (higher) levels. Not only has fixed income volatility been suppressed below its long-term (25-year) average, based on the MOVE index (see chart), but also, as we have recently shown in Summer Charts: Cross Asset Class Volatility, fixed income volatility seems to lead equity volatility and has been influenced by policy. With the Fed being less accommodative, risk now originates from the bond market. To demonstrate that our assessment is not “off,” please also see the work done by my brilliant partner Adam Thurgood, making the case we have recently experienced relatively “muted” equity volatility.

Whereas the IMF (and most market observers) granted an “exceptional” status to the U.S. economy last year, the facts are less clear today. U.S. corporate earnings, which have been largely driven by margin expansion (not actual revenue growth), continue to be adjusted downwards, and the consumer—typically a steady pillar of the domestic economy—has been exactly that: steady, but without the material spending uptick economists had expected as a result of lower energy costs. Worse, recent consumer sentiment readings are in sharp decline. Export volume, as an important last anchor to a resilient economy, should also be expected to move lower, given the continued strength of the U.S. dollar.

Common wisdom explains that recent volatility and related stock market corrections are likely not a lasting issue, as long as the U.S. economy is not entering a recession. Given the above, this is where my concern comes in, as the last pockets of opportunity have to be questioned. Although the labor market continues its recovery (not necessarily accounting for the large “drop-out” rate in the labor force), employment increases linked to growth in the shale gas (energy) and real estate sectors are questionable. With continued pressure on oil prices, shale may not recover for years to come, and building activities have been tilted heavily towards multi-housing units, mixed retail, etc.—a rather interest-rate sensitive business.

It is fair to say that cheap money made available by the Fed has “fueled” industries and investments that would have otherwise not come off the ground and created employment as a byproduct. It will be important to understand whether investors in financial and real assets will still view conditions as opportune, if and when rates rise¾not only as a matter of policy adjustment, but also due to volatility affecting market prices. Even though we postulated that this year would benefit the real rather than the financial economy, we have to recognize that the correlation of the two has become much tighter over the past years; once again, this is a product of misplaced policy activity and related expectations.

However we interpret the facts, what remains is not a promising picture in the short term. As much as investors and the financial industry do not want to acknowledge the risk (and somewhat related necessity) of a corrective element in markets, it is time, not only to remove speculative aspects from our economy, but to refocus investing on value considerations; this should also help to restore order in my line of business, where critical thinking will once again be necessary to help clients achieve their objectives.

Matthias Paul Kuhlmey is a Partner and Head of Global Investment Solutions (GIS) at HighTower Advisors. He serves as wealth manager to High Net Worth and Ultra-High Net Worth Individuals, Family Offices, and Institutions.

{kind=link}