MLPs (Master Limited Partnerships) are rather complex animals in the investment world. Basically, they are companies which own pipelines, the highways in which the majority of our nation’s oil, gas and petroleum-based liquids flow. MLPs tend to pay out high dividends. The business structure they employ deems it appropriate for high-dividend payments. Indeed, the MLP business structure should only be used by organizations whose cash flow is very predictable as retained earnings (the equivalent of a business safety net) are very small in the typical MLP structure as compared to normal corporate structure.

The drivers behind revenue generation for MLPs are primarily tolls paid by purchasers of petroleum products to move these products from one point to another. As an example, oil imports coming into the Houston docks need to be moved to refineries across our country. Oil being produced in the fracking fields of North Dakota, Texas and other locations needs to be moved to refineries is another example. Natural gas also needs to be moved from wellheads to the users of it (industry, utilities and homes). The vast majority of the movement of petroleum products in our country occurs in pipelines. Many, if not most of these pipelines, are owned by various MLPs.

The demand for oil and gas is rather stable in the United States. Most of us need to drive cars (oil demand) and heat our homes (natural gas demand) irrespective of economic conditions. Economists label this type of demand as inelastic demand, or demand which doesn’t change radically with a given price change. However, on the margin, demand can change and specifically the long-term view of demand for transportation services can change given a change in the outlook for long-term fundamentals. This is what has been happening in the MLP space.

Changing Long-Term Outlook for MLP Revenue Growth

Revenue generation (and cash flow) in the MLP space normally is translated into higher dividends to shareholders. MLP market pricing has been driven by two main factors over the last 20 years – dividends paid (yield) and expected growth profile (higher revenues and cash flow). Normally, dividend yields are compared to another alternative yield vehicle (U.S. Treasury bonds as an example). When the available MLP yields are high in relation to U.S. Treasuries, MLPs tend to rise in value.

This condition is currently the case as MLP yields are in the 6.5 percent range. The 10-year U.S. Treasury is currently yielding 2.15 percent. The 4.35 percent spread between MLP yields and Treasury yields is higher than normal. Over the last 20-year period, this spread has averaged 3.07 percent. Historically, when this spread has been higher than normal, MLPs have generated an annual total return of 9.6 percent. The normalization of this spread has tended to be a short-term driver of price performance for MLPs and not a long-term determinant of value. Nonetheless, this spread is currently reasonably high. Yield-oriented investors may wish to take notice.

But the real generator of long-term relative performance for MLPs is growth of revenue and cash flow. This is the “raw stuff” of higher dividend payments in the future.

Growth Drivers – Domestic Drilling Activity

Since hitting a high price in August of last year, the Alerian MLP Index has seen a price contraction of more than 32 percent. More than half of that decline has occurred since May of this year. Have MLPs cut their dividends by 32 percent? No. What has changed over the last year? Oil and gas prices have declined and many analysts (including this one) believe the day of oil trading consistently above $100 per barrel is over for some period of time. This creates a two-edged sword regarding projected growth rates for MLP revenues and cash flows.

On one hand, stable oil and natural gas prices bring more predictability to the energy patch, including the development of new oil and gas wells. On the other hand, a lower overall price picture brings with it the lack of drilling activity in the oil patch, which could have occurred but may not, due to lower overall prices.

Some say MLP revenues don’t have a long-term attachment to oil and gas prices, but they do. Higher oil and gas prices bring additional drilling activity to domestic production fields. As petroleum products need to be transported from the oil/gas fields to refineries, pipeline capacity is utilized, bringing additional revenue to the MLP complex. High oil prices, along with technological advancements, drove the explosion in drilling activity in the fracking fields over the last five years.

Oil imports have changed dramatically over the last seven years. In 2008, the United States imported 5.8 million barrels of oil per day from OPEC producers. Today we import 2.7 million barrels per day from OPEC. The decline of OPEC oil imports has been made up by imports from Canada (up 1.5 million barrels per day from 2008 - current) while the rest has been made up by domestic oil production. This additional oil needs to be transported, with MLPs being the beneficiaries.

Oil prices act as a double-edged sword in this analysis. Lower oil/gas prices slow drilling activity which eventually slows the growth rate of MLP cash flow. This lowers the dividend growth potential. This is exactly what has been happening in the MLP space over the last year as oil and natural gas prices have declined significantly. Lastly, oil and gas development companies have been lowering their expected oil/gas drilling budgets significantly since late last year, confirming that the growth rate of both drilling activity and eventual oil/gas production will slow as compared to the rapid growth rate witnessed over the last number of years.

Growth Drivers – Economic Growth and Disintermediation

Increased economic activity has historically brought the need for higher levels of energy consumption. However, due to a rising level of energy efficiency and a raw change in how the U.S. economy functions, (more services, less industrial activity), GDP has grown more rapidly than our energy consumption levels. For example, from 1980 through 2012, the U.S. GDP grew by 137.6 percent while our energy consumption (when measured by Btu equivalent) grew by 21.7 percent. Our economic growth-to-energy consumption ratio has been 6.3 to 1. If anything, that ratio will continue to expand as most users of petroleum products continue on their efficiency quest.

If the long-term ratio holds, our economy can grow by 3 percent and our energy consumption will only grow by .5 percent. Remember, MLP pipeline operations tend to act as toll roads and receive revenue based on volumes pushed through the pipelines.

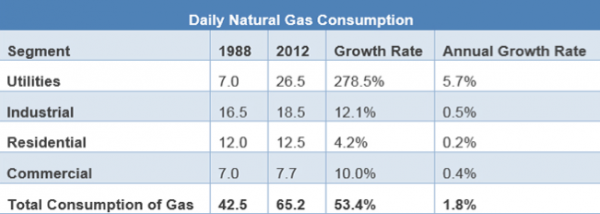

Another fundamental growth driver has been the disintermediation of gas for coal by our nation’s electric utility complex. There are four main segments of the U.S. economy which utilize natural gas as a fuel of choice. The four segments are listed below along with data showing natural gas consumed per day from 1988 to 2012 (measured by billion cubic feet per day). Data is provided by Ned Davis Research (NDR).

So, over the last 24 years, U.S. natural gas consumption has risen by 53.4 percent, or a little less than 2 percent per year. This growth has been driven by the electric utility industry as disintermediation has occurred due to fuel preference shifting from coal to natural gas. This has happened for various reasons, including mandates/concerns regarding pollution emissions.

I don’t see ecological concerns abating to any great degree in the future. Consequently, the switch from coal consumption to natural gas consumption should continue.

Bottom Line – Growth to Slow, but Long Term Opportunity Solid

With everything mentioned above, it is hard to not come to the conclusion that growth rates for MLP revenues will probably slow in the future. This is indeed what market prices for MLP shares have been telegraphing over the last year. What growth rate seems rational going forward? Natural gas MLP revenue growth rates should be in the 4 - 5 percent range (volume growth of 2 percent and inflation adjustments in the 2.5 percent area). Oil pipeline revenue growth may slow to the 3 - 4 percent level if oil prices trade between $40 and $70 per barrel.

With this in mind, I suggest top-line growth for many MLPs may be 3 - 4 percent going forward. Combine this number with current dividend yield rates of 6.5 percent and it brings expected total return for the MLP space to around 10 percent over the long-term.

Final Word

Have MLPs hit bottom? I don’t know, but if oil and natural gas prices fall further, MLP prices may fall accordingly. From May 1 - current, oil prices have fallen from $61 per barrel to $44, a decline of 28 percent. At this same time, the Alerian MLP Index has fallen by 19 percent. Additionally, from peak valuation last September, the Alerian Index has fallen by 32 percent in value (oil prices have declined by 55 percent over that same period).

On the other hand, MLPs are out of favor and provide high solid yields. Yield hungry, value oriented investors may want to take notice.

William B. Greiner, CFA, is Chief Investment Strategist at Mariner Holdings.