The cool and trendy hot topic five years ago was technology, which then turned to integrations just a few years back. Today’s hot topic isn’t sexy but worth discussing in length: lean operations planning. Operations Planning and Lean Six Sigma are the keys to succession planning, profitability, and creating a firm that attracts both clients and the next generation of young, eager advisors.

Many advisory firms feel they are managing their business reactively rather than proactively. Advisory business owners don’t feel they have the time to develop a lean operations plan, as they are consumed with prospect engagements, assisting clients, tweaking service offerings and pricing, updating marketing, managing employees, and more. What gets lost in the shuffle is the client experience, and that translates to a loss of future revenue and referrals. The industry has seen client profitability slip from 37% to lower than 25% between 2010 and 2012. This dilemma is a common trend today in advisory firms from $50m to over $1+ billion, and it is especially rampant in the firms offering full wealth management services.

What is the solution?

The most frequent recommendations are to maximize the potential of the CRM, integrate new technologies, outsource, and hire. While these are all beneficial ideas, they are only pieces of the greater solution - the development of a lean operations plan. Successful, profitable advisory firms are implementing their customized plan to increase capacity and client profitability, and proving that the effort is not impossible, despite how overwhelming it might sound.

Why consider this lean operations plan?

Content is pouring from all sources to try and help firms achieve the success that can be read about in Good to Great by Jim Collins. Advisory firm experts Eliza De Pardo and Dan Inveen state: “How a firm structures and manages its operations is essential for delivering on the firm’s value proposition in order to retain target clients and attract more like them”. Envestnet entices you to consider technology integrations as a solution and states that firms with some integration “earn 20% more income than their peers and spend 32% less time on operations work”. Wealthmanagement.com’s 2013 AdvisorBenchmarking RIA Trend Report study analyzes top performing firms and their client profitability, operations, and best practices. Lean Six Sigma for Service by Michael L. George proclaims that “30-80% of servicing costs are a waste and add no value from the perspective of the client”. Advisory firms are finally capitalizing on these facts and moving forward to resolve the capacity profitability conundrum.

Here is what you need to get started on creating your own lean operations plan:

First, start getting excited about the word “Operations” and then set your firm on a course to develop an operations plan. This is a fluid document that details the following:

1. Company's objectives for creating the plan

2. Beginning benchmark to gauge ROI of the improvements

3. List of the improvements and benefit of each

4. Timeline of when to start and finish implementation of each improvement

5. Cost

While creating this Operations document, be aware that there are five stages to acknowledge (IDEOS TM): Integrations to reduce the work, Delegation through processes, Elimination of work, Outsourcing of work, and Staff restructuring. This five-stage concept is aimed at increasing capacity to service more clients, keeping operational costs from climbing, and creating a more enjoyable work environment for all. Here are the steps to getting your lean operations plan started:

1. Schedule your first Operations Meeting with your core staff and executives. The meeting should last approximately two hours and should include those in your practice who can offer ideas and be held accountable to manage certain projects and initiatives. Assign one person to record minutes.

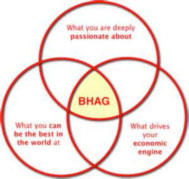

2. In the first meeting, identify at least one lofty goal and determined how it can be measured. These can often be referred to as big hairy audacious goals or BHAG (Good to Great by Jim Collins).

These are long term goals and are often related to profitability and gross revenue. For example, you decide you want to increase client profitability. Your firm has 175 client relationships, gross revenue of $560,000, and annual operating expenses of $450,000 before owners’ compensation. The math on profitability isn’t attractive so you set a goal to increase profitability per client from your current $628 to a goal of $3,000 by reducing operating expenses or doubling your client base without increasing operating expenses. This metric of $628 becomes your benchmark and metric to reassess on a continually basis.

3. List every project that you believe will help your firm reach those goals. This can be as miniscule as assessing your office supply inventory and ensuring you are getting good prices. It can be as big as adding or changing a service to better fit your ideal clients’ needs or adding new technologies to reduce the human labor. No matter how big or how small, list it! Then move on and do not discuss each item but leave the conversation for another day or your meeting will last for days or come to a screeching halt.

4. Classify each project under these main categories of IDEOS™: Integrations to reduce the work, Delegation through Processes, Elimination of Work, Outsourcing of Work, and Staff Restructuring.

5. Assign someone as project manager to each project.The person assigned should be passionate about this project and see the benefit of completing it.

6. Establish a system to track progress. This system may be as simple as scheduling a weekly meeting to discuss progress and roadblocks on each of the initiatives, setting up a running task for each project in your CRM, or using a project management tool.

7. Schedule the second meeting for project managers to present their game plan for how they will tackle their assignment. This game plan should include the cost of the project (labor, tech, etc), timeline that works best for starting and finishing the project around the firm’s normal workload and servicing cycles, and 1-3 next steps that need to be done to move the project forward.

8. Create a master project timeline that includes all the projects in chronological order.

9. Schedule the next meeting so share your decision on what project should be started and when.

10. As always, continually adjust the master operations plan and re-run your metrics and compare to your original benchmark.

Resources to help you create and implement your operations plan.

There are great resources that can help build your lean operations plan and you should consult your peers and well-respected advisory firm owners for advice. You could also invest ON your business and employ the input of a third party to help you streamline your thoughts and assess your technological and human resource inventory. Finally, you should take advantage of the great workbooks provided by your custodian or join a study group of CEOs at your custodian or within an industry association.

Whether you ask for help, or you and your team tackle this on your own, one thing is for certain: You will be able to relax and focus on what you are really passionate about once the lean operations plan is in place, and you will experience increased capacity, profitability and a more enjoyable work environment.

Footnote: Jennifer Goldman, CFP® is the Founder of MyVirtualCOO.com, a nationally recognized operations consulting and implementation firm and creator of the largest directory of USA-based outsourcers in the financial advisory industry.