As we return to work after the holidays, a sharp sell off in global equities and escalating geopolitical tensions in the Middle East beg the question whether this New Year will be a happy one for investors. I believe the recent market swings are no more than passing disruptions. For U.S. equities and credit, in particular, evidence is mounting that 2016 will prove happier than 2015 for investors. In fact, the global factors currently roiling the markets are easy to discount, and could lead to investment opportunities.

In China, for example, many point to the drop in the Caixin Purchasing Managers' Index (PMI) as the cause for the volatile equity market’s start to 2016. The more likely catalyst is the pending expiration of an insider selling ban imposed in July 2015 by the China Securities Regulatory Commission that was issued to stave off a market collapse. Chinese regulators are likely to extend the ban beyond this week in response to the current sell off, but as expiring restrictions enable market participants to finally escape unwanted positions, a sell off is inevitable. Until China’s market is free from political interference, these kinds of swings are to be expected.

Meanwhile, the Middle East remains the world’s most ominous geopolitical fault line. If tensions escalate, the impact on the region’s oil reserves could be the catalyst that leads to a sudden rise in oil prices. However current events play out, it is clear that we are approaching the end game in oil’s decline. At this time last year, we predicted a prolonged period during which oil would trade in the $40 to $50 range with a downside price target of $34 per barrel, both of which have now more or less materialized. While I still see more near-term downside, oil prices should start to rebound toward the second half of the year. This means now may be a good time for investors to start selectively increasing exposure to energy, particularly if seasonal factors exert further downward pressure on oil prices in the near term.

In the United States, the good news is that U.S. economy may not be fast moving, but it certainly has a lot of torque, which is creating strong tailwinds as we move into 2016. MasterCard Advisors’ data on holiday spending indicates that sales were up nearly 8 percent year over year. All told, the risk to fourth-quarter gross domestic product (GDP) is probably to the upside, even as most tracking estimates have been trimmed to around 1 percent. In addition, the El Niño weather pattern is moving into its most impactful period. Our research indicates that a strong El Niño can add 1 percent or more to GDP in the first quarter of the year. Factor in seasonal dynamics and the impact of the change in spending policies coming out of the Capitol and 2016 could easily experience growth of between 2.5 and 3 percent, with the prospect that the first and second quarters could see numbers as high as 4 percent. Finally, history indicates that the year following the type of flat market performance we experienced in 2015 typically sees a rally in equity prices. While U.S. equities could have an upside of 5–15 percent in 2016, I expect volatility will remain elevated. Risk-adjusted returns look better in below-investment-grade credits, especially bank loans and B-rated collateralized loan obligations (CLOs). Yields in single-B CLOs can be in excess of 10 percent. Short of a recession, which I do not anticipate anytime soon, these securities should prove winners even if stocks fall.

The bottom line is that I do not believe the painfully low returns across asset classes that investors endured in 2015 will be replayed in 2016. Currently, investors are being well compensated to take on risk, especially in credit. I am reminded of a commentary I wrote in 2011 at the height of the European sovereign debt crisis, where my punchline was “Keep Calm and Carry On.” Despite a rocky beginning to the year, investors should keep their composure and their exposure—there are many reasons to be optimistic that 2016 will be a better year for risk assets than 2015.

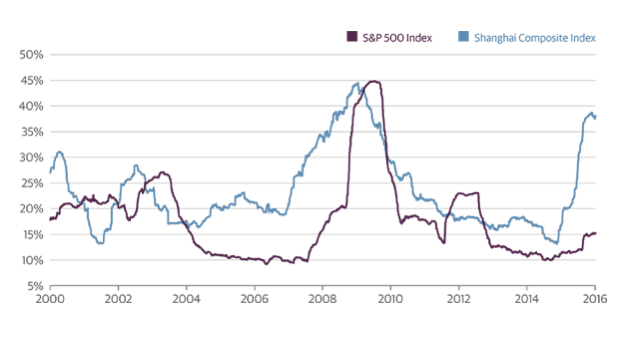

Volatility in Chinese Stocks Has Risen to Levels Not Seen Since 2009

Global markets are off to a turbulent start in 2016, with all major equity markets posting negative returns to start the year. Geopolitical risks in the Middle East and Asia have been pointed to as culprits, but the main source of concern lies in China. Chinese stock market volatility has spiked over the last year amid worries over a slowing economy, a boom-bust cycle in margin debt, and unpredictable and unorthodox moves by local financial regulators. Until conditions stabilize in China, global markets are likely to experience continued uncertainty.

Trailing 12-Month Annualized Daily Volatility

Source: Bloomberg, Guggenheim Investments. Data as of 1.6.2016.

--

This material is distributed for informational purposes only and should not be considered as investing advice or a recommendation of any particular security, strategy or investment product. This article contains opinions of the author but not necessarily those of Guggenheim Partners or its subsidiaries. The author’s opinions are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. ©2016, Guggenheim Partners. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

Scott Minerd is Chairman of Investments and Global Chief Investment Officer at Guggenheim.