Bond Market Outlook

Global Interest Rates: With valuations rich and yields biased higher, we are strategically negative on rates.

Global Currencies: The relative strength of the U.S. economy will continue to support the dollar versus other DM currencies. We continue to favor higher-yielding EM currencies with strong fundamentals.

Corporates: Fundamental remain healthy, as issuers continue to benefit from improving U.S. economy; however, valuations have richened.

High Yield: Valuations have richened, but the asset class is poised to outperform most others in 2014.

Mortgages: QE3 remains supportive in general, but performance is likely to vary across sectors.

Emerging Markets: Headwinds will continue; remain focused on countries with strong fundamentals.

Macro Overview

-

Nothing says “Happy New Year!” like a polar vortex and similarly chilling payroll number, eh? As arctic temperatures swept across the continental U.S. in January, markets got a case of the willies inspired in part by sub-trend U.S. jobs growth in December. Was this disappointing report an ominous barometer of failing economic health, or just an anomalous consequence of Old Man Winter flexing his icy muscles? An optimist would suggest that blustery conditions temporarily depressed job gains in what otherwise has been a positive cyclical upswing for employment. The realist, meanwhile, would point to the falling labor force participation rate as a sign of a long-term structural trend. While the global economy improved in fourth quarter 2013 and leading economic indicators, while mixed of late, suggest the potential for sunnier days ahead in 2014, unfavorable demographics across the developed world will suppress the longer-term U.S. growth and productivity outlook.

-

The good news is that inflationary pressures should remain subdued, as globally the impulse to save continues to outweigh the impulse to consume, with real wage growth lacking. Despite the very poor payroll report and a disappointing durable goods reading, it’s very unlikely the FOMC will pause its tapering efforts at its late-January meeting, particularly given the personnel changes that have watered down its dovish bias. However, the negative payroll data support our view that the Fed will be late, not early, in unwinding zero interest rate policy as other major central banks remain steadfastly accommodating.

-

Emerging markets will continue to feel the chill of the developed markets’ prolonged impulse to under-consume, a chill that will be more deeply felt in countries with fundamental vulnerabilities, weak current accounts and an over-reliance on foreign demand. As such, we expect sectors impacted most acutely by Fed tapering and the gradual move higher in U.S. rates — like mortgages and emerging markets — to remain under pressure. However, healthy U.S. economic growth in 2014 despite longer-term structural concerns will keep interest rates relatively contained and thus support the appetite for assets tied more to credit risk, such as high yield bonds, floating-rate bank loans and CMBS.

Sector Overviews

Global Interest Rates

-

Valuations are rich, and economic fundamentals at the current stage of the business and monetary cycle argue for a strategic negative view for developed market rates. Global data has surpassed expectations at an accelerating rate through the fourth quarter, and first quarter growth expectations in the U.S., Europe, Japan and elsewhere remain consistent with rising yields over the course of 2014.

- However, rates are likely to rise gradually, as near-term momentum seems to be waning — if the recent negative surprise in U.S. payrolls is any indication. From a positioning standpoint, we are negative on the U.S. and Japan, with a more positive strategic outlook for European sovereign credit as the region’s tail risks abate and countries with reasonable growth prospects post-austerity — like Ireland — issue long-term debt at sustainable yields.

Global Currencies

-

The relative fundamental strength of the U.S. economy will continue to support the dollar versus the rest of the developed world and the Japanese yen in particular. However, given that the developed market central banks — including the Fed and ECB — are likely to remain accommodative for some time given longer-term structural concerns, we continue to selectively favor higher-yielding emerging market currencies with strong fundamentals that likely will benefit from the positive growth momentum in the developed world. These include the Mexican peso, Malaysian ringgit and Russian ruble.

Investment Grade Corporates

-

While we remain constructive on the corporate credit market for the first quarter, richer valuations suggest caution is warranted. Corporate spreads will continue to benefit as the U.S. economy improves and underlying credit fundamentals remain healthy. Cash balances are high, and interest coverage is strong. And while M&A and shareholder-friendly activities are picking up, leveraged buyouts are still depressed. We continue to favor financials, which we think offer better visibility on earnings growth and lower levels of event risk compared to other sectors. We also prefer BBB rated securities over A rated securities from a valuation standpoint.

High Yield Bonds

-

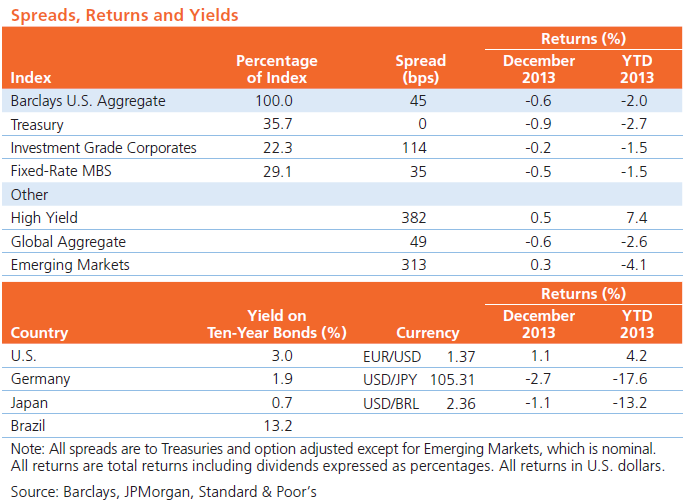

The U.S. economic recovery continues to support tighter credit spreads, and the market has already absorbed a meaningful portion of the likely cyclical move higher in longer-term rates. Corporate balance sheets remain healthy enough to limit the risk of a meaningful increase in defaults for some time to come, with financing — while becoming more aggressive in the second half of 2013 — still not supporting the aggressive capital structures we saw at the peak of the last credit cycle. At more than 400 basis points above Treasuries, high yield spreads offer adequate compensation for likely credit losses and the ability to absorb at least a portion of any additional increase in interest rates; this positions high yield to outperform most other fixed income asset classes over the coming year.

Mortgages

-

Agency RMBS performed very well over the past several months, and some MBS pools no longer appear cheap. Nevertheless, the technical environment has remained strong even as fundamental value has declined, as quantitative easing remains a major driver of near-term performance. We continue to see an interesting balance in the mortgage market, finding value in certain areas while reducing exposure in others. Although the Fed’s purchase program should keep some MBS spreads anchored in early 2014, not all agency RMBS spreads are created equal; 30-year GNMA 3.0% pools, for example, may underperform, as they are not actively being purchased by the Fed and fundamental value is less compelling. Activity across other securitized products like non-agency RMBS, CMBS and ABS has picked up sharply to start the year, dominated by risk-seekers; we expect this momentum will continue to support valuations.

Emerging Markets

-

Economic activity has improved across the developed markets as evidenced by a relatively broad-based pickup in manufacturing PMI indicators. We expect near-term economic activity in the emerging markets to show some improvement based on spillover effects from stronger developed market economies, but the pickup will not necessarily be uniform. Chinese GDP growth slowed in the fourth quarter, and January’s contraction in manufacturing suggests the negative trend has spilled over into 2014. As outflows persist, the forecast for EM as an asset class appears to be spotty at best, particularly in local-currency investments. Given these headwinds, we continue to favor sovereigns over corporates, with a selective bias for export-based economies with strong fundamentals while avoiding countries with weaker fundamentals and larger external funding needs.

ING U.S. Investment Management’s fixed income strategies cover a broad range of maturities, sectors and instruments, giving investors wide latitude to create a new portfolio structure or complement an existing one. We offer investment strategies across the yield curve and credit spectrum, as well as in specialized disciplines that focus on individual market sectors. We build portfolios one bond at a time, with a critical review of each security by experienced fixed income managers. As of September 30, 2013, ING U.S. Investment Management managed $121 billion in fixed income strategies in the United States.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

Past performance is no guarantee of future results.

©2014 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 8446