The Barclays U.S. Aggregate Index is a broadly based, widely followed index of fixed income markets, based on a market-cap-weighting of investment grade bonds traded in the United States.

The Barclays U.S. Aggregate Index is a broadly based, widely followed index of fixed income markets, based on a market-cap-weighting of investment grade bonds traded in the United States.

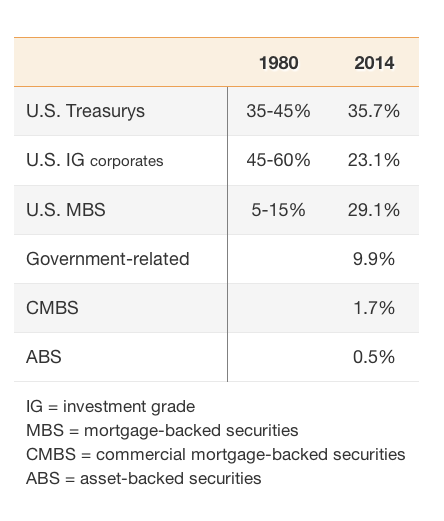

Since its inception in 1976, the index has evolved along with the development of various fixed income sectors, taking into account their embedded duration and issuer concentration profiles. For example, as asset-backed securities (ABS) became more popular, these were included in the index in 1991, followed by commercial mortgage-backed securities (CMBS) in 1997. The table below illustrates how the composition of the index has changed during the past 30 years.

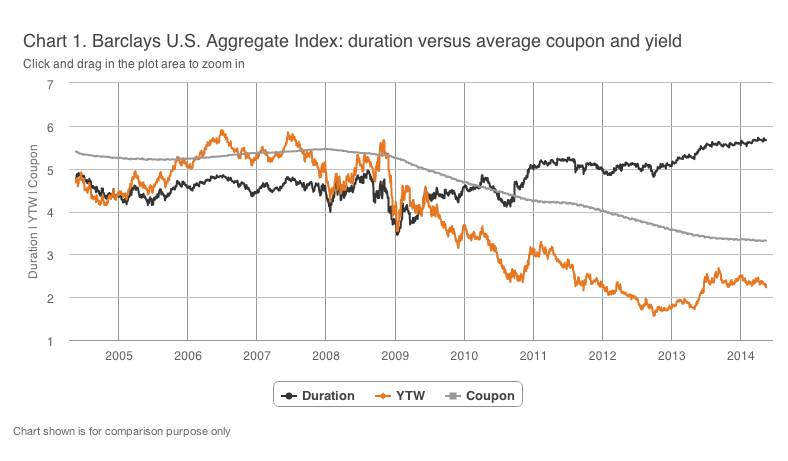

As shown, issuance trends — the emergence of new sectors and their underlying duration and concentration profiles — have shaped the index since its inception. However, let’s focus on the more-recent evolution of the index, in particular its duration profile since 2009 (see Chart 1).

The data illustrate considerable duration extension within the index, while its yield and coupon have experienced some compression. For investors benchmarked to the index, this means taking more interest rate risk (in the form of duration) in exchange for smaller future rewards (yield). At this writing, the index’s current yield of 2.23 and its duration of 5.66 imply that an interest rate increase of 39 basis points would wipe out the yield component of total return. (One basis point equals one one-hundredth of a percentage point.)

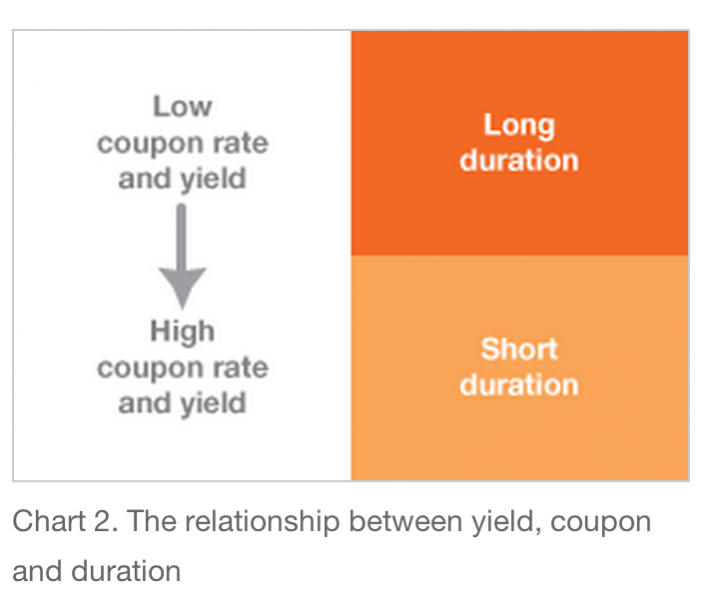

A closer look at the relationship between duration, coupon, and yield can help explain why bonds with high coupon rates and, in turn, high yields will tend to have lower durations than bonds that pay low coupon rates or offer low yields. It makes sense because when a bond pays a higher coupon or has a high yield, the holder of the security receives repayment at a faster rate. Chart 2 summarizes this relationship.

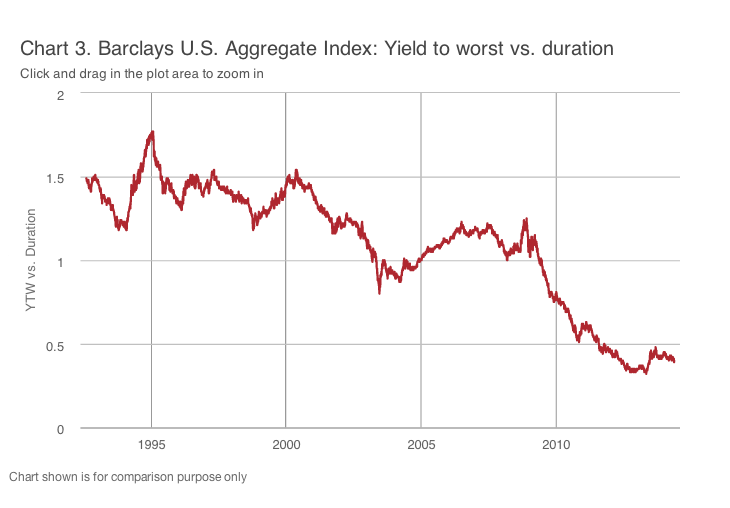

Because yield and duration are the key drivers of total return for a bond investment, it is interesting to look at the yield-versus-duration relationship historically, as plotted on Chart 3.

Based on this metric, the risk-reward associated with index-based investments is asymmetric. Another way to think about this is that over the same time frame, the annualized total return for the index was 6.83%, while the average coupon rate was 6.37%, which implies that over long periods, the coupon component represents the majority of total return (in this case, 93% of total return). Apply this concept to the index’s current coupon of 3.32%, and you see the index’s reward potential in today’s environment.

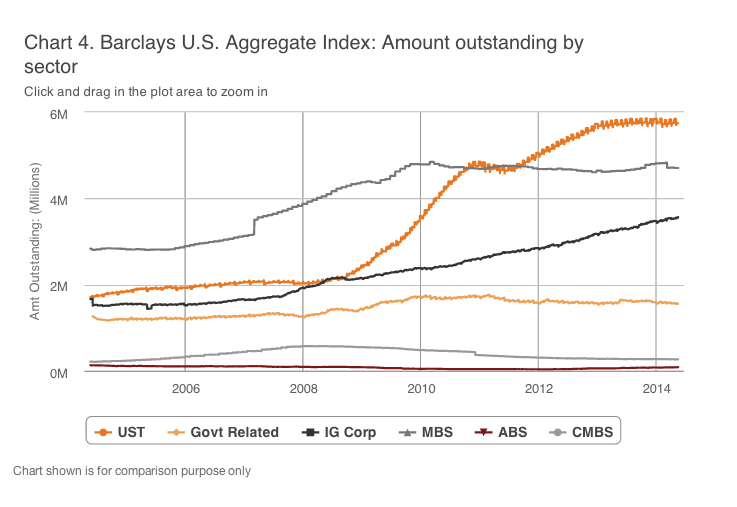

Chart 4 examines each sector within the index to isolate the source(s) of the index’s duration extension.

Barclays U.S. Aggregate Index: Amount outstanding by sector Chart 4. Barclays U.S. Aggregate Index: Amount outstanding by sector Compared to 2009, the amount outstanding has increased in Treasurys and investment grade corporates, while the amounts of MBS and government-related debt have shrunk. At the same time: (1) the average maturity has remained stable in Treasurys; (2) ABS and CMBS have shown contraction; and (3) government-related, investment grade corporates, and MBS have shown extension. We also note that the average coupon rate has compressed across sectors as new-issuance refinancing has occurred at lower yield levels. In terms of contribution to duration, Treasurys, investment grade corporates, and MBS have extended the most.

A Word About MBS Durations, and a Closing Note:

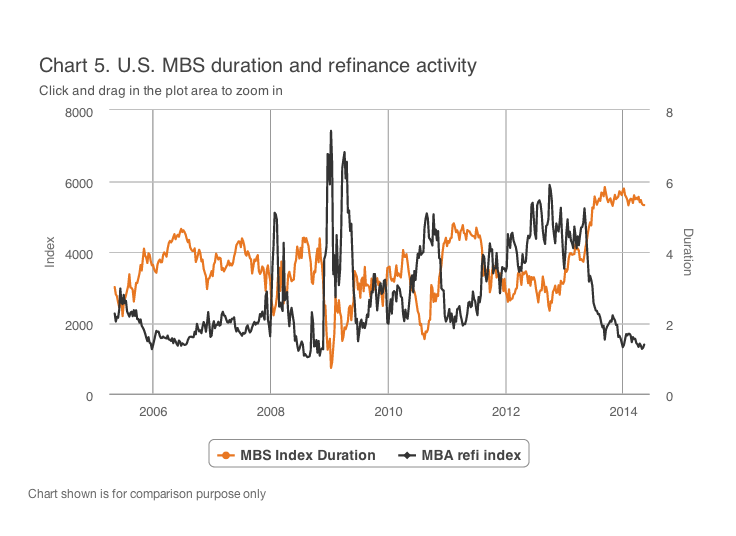

Lastly, we want to focus on the duration dynamics of MBS. Refinance waves (represented in Chart 5 by the Mortgage Bankers Association Refinance Index) have led to the creation of “new” MBS securities that carried lower coupons and longer durations. These securities were then included in the index, extending its overall duration (Chart 6).

In light of the evidence mentioned thus far, we conclude that the risk-reward scenario created by the current interest rate environment is unattractive for investments that mirror the Barclays U.S. Aggregate Index. Across the portfolios we oversee at Delaware Investments, we therefore advocate the diversification of income strategies versus interest rate risk (spread over duration), which we believe can offer a degree of protection from downside risk and potentially achieve a reasonable return on (and of!) capital.

The views expressed represent the Manager's assessment of the market environment as of June 2014, and should not be considered a recommendation to buy, hold, or sell any security, and should not be relied on as research or investment advice. Views are subject to change without notice and may not reflect the Manager's views.

Carefully consider the Funds' investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Funds' prospectuses and their summary prospectuses, which may be obtained by visiting the fund literature page or calling 800 523-1918. Investors should read the prospectus and the summary prospectus carefully before investing.

IMPORTANT RISK CONSIDERATIONS

Investing involves risk, including the possible loss of principal.

Past performance does not guarantee future results.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Diversification may not protect against market risk.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt. The Funds may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Funds may be prepaid prior to maturity, potentially forcing the Funds to reinvest that money at a lower interest rate.

High yielding, noninvestment grade bonds (junk bonds) involve higher risk than investment grade bonds.

The Mortgage Bankers Association Refinance Index provides a weekly measure of all applications submitted to refinance an existing mortgage, including conventional and government refinances.

Ion Dan is a Senior Structured Product Analyst and Trader for Delaware Investments

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}