You've probably heard the worry in your clients' voices: Will the federal government's multiple stimulus policies send inflation soaring? How can I protect my portfolio and my beneficiaries from “CPI in the sky?”

Identifying a good inflation-hedging asset can be surprisingly tricky. One reason is that you have to predict whether inflation will be bad — but that exposes you to “prediction risk,” which is defined as the chance of moving into the wrong asset based on a mistaken prediction.

Another reason is that the shorthand ways of talking about inflation hedging ability, especially the correlation coefficient, are generally the wrong way to think about the problem.

Here's a review of the investment attributes of three classic inflation hedges: real estate, commodities and U.S. Treasury inflation-protected securities (TIPS). The three assets differ in important ways, but all of them serve a valuable function in protecting against a plague of price increases.

How Should an Inflation Hedge Work?

What clients want from an inflation hedge is simple: They want an asset whose returns will protect their wealth from the loss of purchasing power that comes when prices rise. To be specific, when inflation is high, clients want their asset returns at least to keep pace with the consumer price index. The response does not have to be immediate, but asset returns should dependably catch up to the price increase.

Notice that I've said nothing about a “high correlation between returns and inflation.” That's because correlation is the wrong measure of inflation hedging ability, for three reasons. First, a high correlation means that when inflation goes down, asset returns go down, too: not exactly what your clients are hoping for, and certainly not required of a good inflation hedge.

Second, the correlation coefficient measures only the contemporaneous response, that is, whether asset returns respond in the same month (or quarter, or year) as the surge in inflation. But an inflation hedge doesn't have to be contemporaneous. TIPS, for example, adjust to the inflation rate only every six months, meaning that their returns are almost guaranteed not to be contemporaneous with the price index.

Third, and most important, the correlation coefficient says nothing about whether the asset returns actually protect purchasing power. Think of a hypothetical security whose return is exactly equal to one-hundredth of the inflation rate. If inflation surges to 30 percent, for example, then your asset return goes up to 0.3 percent. The correlation between inflation and asset returns would be perfect, but your clients' purchasing power would be unprotected.

The Inflation Protection Dependability Index

Here's a better way to think about inflation protection: When inflation is high, how dependable is each asset in protecting purchasing power? You can measure that using what we call the Inflation Protection Dependability Index, or IPDI.

This is how it works. First, define the time period that provides for “acceptable” inflation protection. Remember, returns don't have to respond contemporaneously to surges in inflation, but they should respond pretty soon thereafter. As we noted, TIPS are adjusted to inflation on a six-month basis, which seems reasonable.

Second, consider what happens to asset returns only during those periods when inflation is high. That is, your clients aren't looking to hedge the risk of low inflation — so don't judge an inflation hedge by what it does when inflation is low (or negative). For example, one way to define “high-inflation episodes” is those six-month periods during which inflation is greater than its median value of about 3.26 percent annualized.

Third, look at the historical record to find out whether the total returns on each asset at least covered the inflation rate during those high-inflation periods. It's important to look at total returns — not just dividends — because few (if any) of your clients can afford to depend only on income returns to allay their worries about inflation.

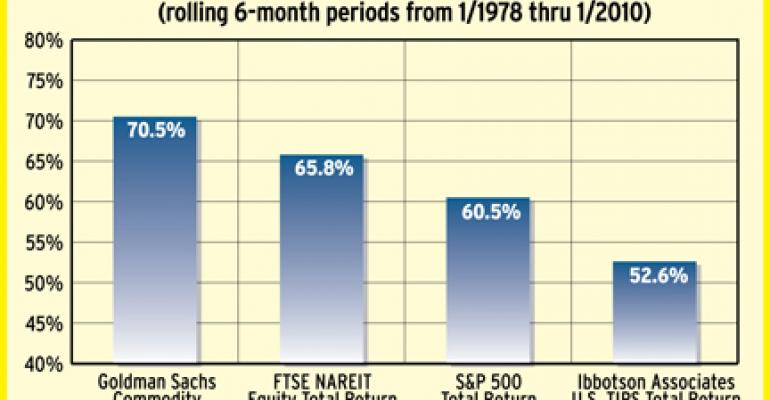

The first shows the Inflation Protection Dependability Index for the three classic inflation hedges — real estate (accessed through publicly traded REITs), commodities, and TIPS — along with the U.S. stock market. As you can see, commodities and REITs have historically provided the most dependable inflation hedging, with total returns meeting or exceeding the inflation rate in 70.5 percent and 65.8 percent, respectively, of high-inflation six-month periods.

TIPS turn out to be a surprisingly poor inflation hedge, with total returns protecting purchasing power in only 52.6 percent of high-inflation periods. TIPS are almost as bad as flipping a coin when looking for inflation protection. Even stocks turn out to be a better inflation hedge than TIPS.

What About Prediction Risk?

As we noted, one problem with hedging against inflation is that nobody can predict very confidently exactly when price increases are going to hit. There are good reasons why you should take this into account.

During periods of high inflation, commodities historically have often provided the strongest returns. That's not surprising, because the CPI largely measures the changes in commodity prices, especially gasoline and other energy costs. (Incidentally, gold — another commodity that's often touted as an inflation hedge — actually has ridiculously poor inflation hedging dependability, covering price increases in only about 40 percent of high-inflation periods.)

But during low-inflation periods between January 1978 and January 2010, the average return to commodities is just an annualized 0.67 percent. That's far worse than TIPS, the S&P 500, and equity REITs, less even than the “low-inflation” inflation rate. That means that commodities expose your investors to very high prediction risk: If you guess that inflation will be high, but the Federal Reserve succeeds in holding it down, then you've put your clients into the worst possible asset.

Now consider the performance of other assets. The total return on TIPS over the 32-year range just barely exceeds the inflation rate during high-inflation months; the excess return (from investing in medium- to long-term bonds) appears only during low-inflation months.

In contrast, publicly traded REITs — even after experiencing the worst crisis in their history during 2007-2009 — provided stronger returns during high-inflation months than any asset other than commodities. What's especially important, though, is that REITs didn't expose investors to prediction risk. REIT returns were also high — second only to stocks, and just barely — during low-inflation months, too.

That means that publicly traded REITs are the only assets that historically have protected investors from inflation in both crucial ways: They provide dependable inflation protection when it is needed most, and they don't expose investors to prediction risk. Those are two forms of protection that your investors will truly respond to.

Brad Case is vice president, Research and Industry Information National Association of Real Estate Investment Trusts