(Bloomberg) --Retirement security in the U.S. took a significant hit in a global ranking, falling three notches to No. 17 among 43 developed countries.

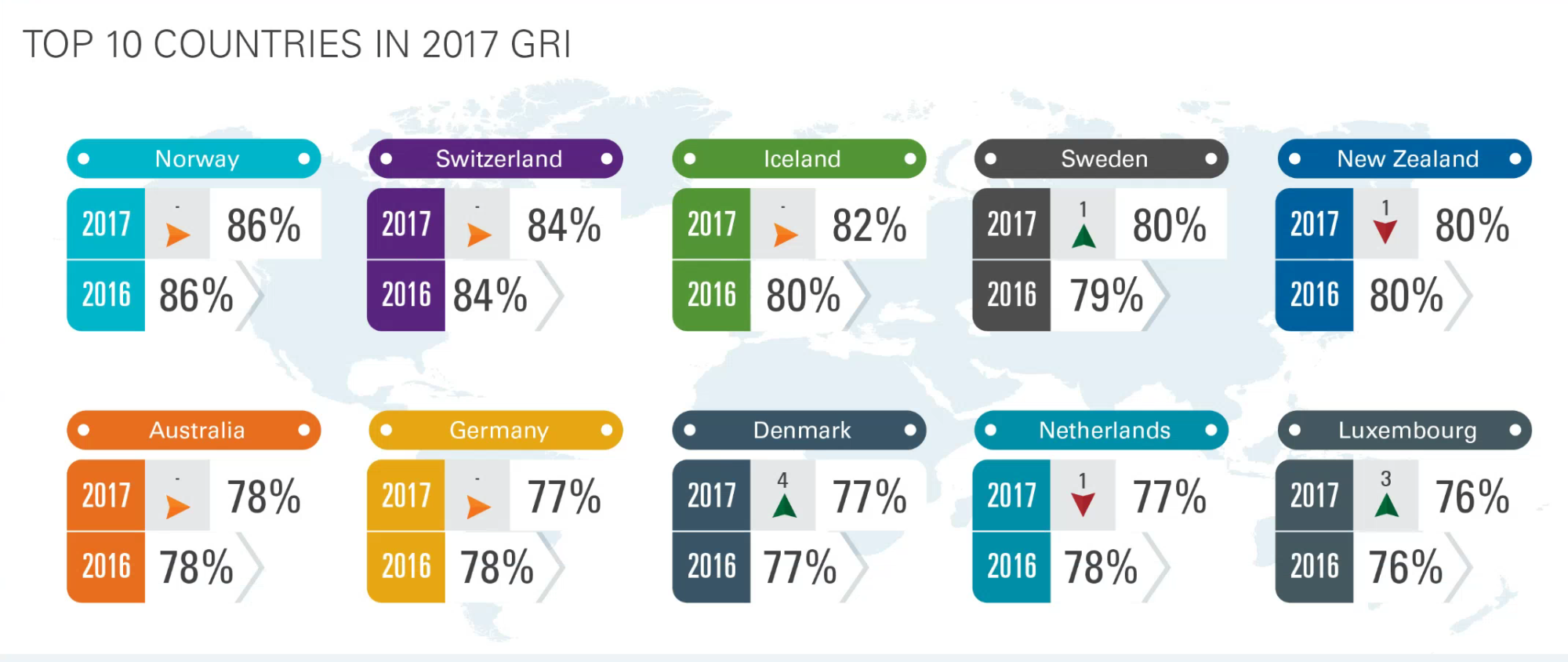

The fifth annual Global Retirement Index ranking from Natixis Global Asset Management has Norway, Switzerland, and Iceland holding on to the top three slots from 2016. The ranking creates an overall retirement security score for each country from 18 performance indicators that address finances, healthcare, material well-being, and quality of life. Countries are also ranked by those four sub-indexes.

Of the 25 countries with the highest overall scores, the U.S. and Austria saw the biggest annual declines this year. The U.S. score is 72 out of 100, which puts it right below Belgium and the Czech Republic and just above the United Kingdom and France. The U.S. had the sixth-lowest score for income equality, which is part of the score for material well-being. That measure, designed to show how well a country's population can provide for its material needs, combines an income per capita index, income inequality index, and unemployment index.

Here are the countries that score the highest for how well their citizens are set up to enjoy a comfortable retirement. The arrows next to the 2017 ranking in the graphic show whether the country stayed the same (orange), moved up (green), or moved down (red) in the rankings, and by how many slots.

When scores are tallied by region, the U.S. and Canada rank higher than western Europe, with scores of 73 percent and 70 percent, respectively. The U.S. was No. 10 on the finances sub-index, largely thanks to improvements in bank non-performing loans, as well as its level of federal debt relative to other countries. But the regional win is largely due to the financial struggles in Italy, Portugal, and Spain. Canada ranks at No. 11 in the country rankings, down one notch from 2016, with a score of 76 percent.

One measure that hurt the U.S. in this year's index was its rank as No. 30 on life expectancy, even though it spends more per capita on health care than any other country in the index. The mismatch suggests U.S. health expenditures "may not be yielding the same return on investment" achieved by top-ranked countries for longevity, such as Japan, the survey diplomatically noted.

The U.S. was also dinged because income inequality rose from last year. America got the sixth-lowest score in the material well-being category for all 43 countries, even though it was No. 5 in per capita income. The report's analysis: "The results suggest that millions of lower-income Americans are missing out on that economic growth and may struggle to save for a secure retirement as a result."It shouldn't be too surprising, then, that the quality-of-life measure for retirees fell for the U.S., mainly due to a dip in a happiness indicator. On the bright side, cleaner air improved the American ranking on environmental factors, which are included in the quality-of-life sub-index score.

Challenges to retirement security in a world of aging populations and increasing longevity was a major theme of the report. The ranking looks at "old age dependency," the ratio of the population of younger workers, who will be paying into a retirement system like Social Security, to the retiree population drawing down that money. The bigger the pipeline of younger workers relative to older workers, the better the score.

"If we only had one of these factors—poor dependency ratios but people weren't living longer, or great dependency ratios so it would be OK that people were living longer—it wouldn't represent the type of risk it does to the entire retirement system," said Dave Lafferty, chief market strategist for Natixis. "It's the combination of those two things that presents a real problem."

For most countries, there are not enough younger workers to support an aging population in the next few decades. The chart below shows where countries rank on this metric now, and projections of where they will rank in 2030 and 2050.

A deficit of younger workers paying into retirement systems for older workers is a dilemma faced across the developed world. Even top-ranked countries for retirement security face this issue. Germany, Sweden and Denmark, all top 10 countries on the overall ranking, are in the bottom 10 for this measure.

This global retirement picture is playing out against a backdrop of slow economic growth worldwide and low momentum in productivity gains. "We see a bit more synchronization in growth rates around the world for the first time in seven or eight years," said Lafferty. "It looks like it is picking up in the near term, but it's limited in the long term unless we can unlock productivity gains, which are hard to come by." In the U.S., an unpopular solution to improve the finances of Social Security would be to raise the age at which Americans are eligible for benefits, Lafferty noted. "Social Security was designed in a period where the likely age of mortality was right around the early 60s, so right around when Social Security kicked in," he said. "As people live longer, it would make sense to extend that out."

While that may be a great mathematical solution, it's not a big vote-getter for politicians, he added. Also, even if many Americans want to work longer, they aren't always able to, because of ageism, disability, or changes in their industries.

All in all, finding solutions to retirement problems "takes public policy leadership, and there isn't an enormous amount of that out there right now," Lafferty said.

Have personal finance questions or lessons to share? Join Money Talks, the new Facebook community from Bloomberg News.

To contact the author of this story: Suzanne Woolley in New York at [email protected] To contact the editor responsible for this story: Peter Jeffrey at [email protected]