fingerprint")

(Bloomberg) --A retirement savings wave that has been rolling stealthily across corporate America is gaining momentum. Some 68 percent of large U.S. companies now automatically enroll employees in 401(k) plans, up from 58 percent two years ago, according to a new survey. Three-quarters of those employers bump up worker savings rates automatically every year, and many continue until savings rates hit 10 percent and beyond—or until, presumably, the employee screams.

That may seem a little heavy-handed, but a retirement plan that's largely on autopilot can make inertia work for, rather than against, savers. After all, saving 10 percent of one’s salary doesn’t even meet the minimum suggested by experts such as Morningstar’s head of retirement research, David Blanchett. He puts the minimum at 12 percent, and says a good rule of thumb is more like 15 percent. Some of that should come from your employer’s matching contributions.

A biennial survey by benefits administrator Alight Solutions reached 333 big U.S. employers representing 10 million workers and $775 billion in retirement assets. Among some of the positive signs in the survey: A third of companies are setting the default savings rate for workers automatically enrolled in their plans at 6 percent or more of salary. The survey still found the common, inadequate savings rate of 3 percent at 37 percent of employers.

Here are highlights from the report:

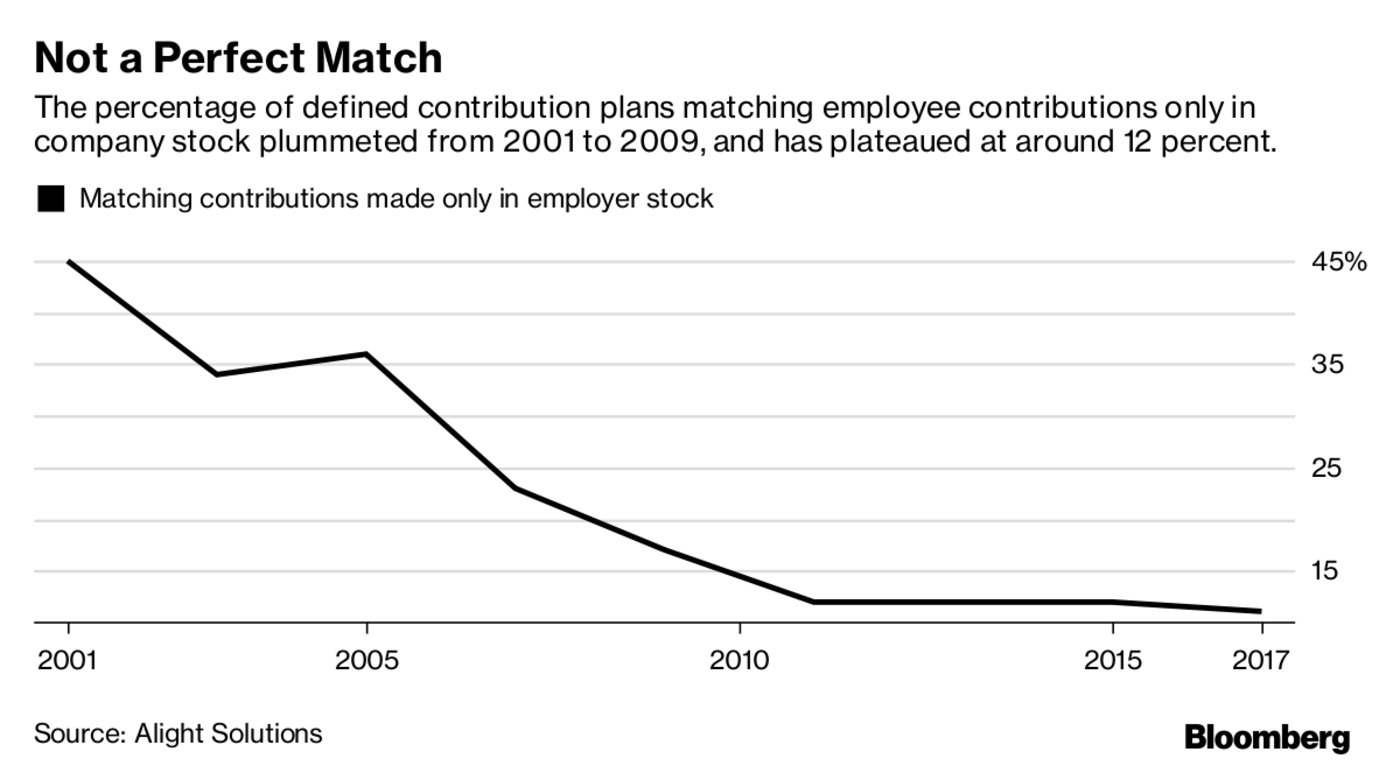

- Thirty-four percent of the companies offer employer stock as an option in plans. As an asset class, it made up 11 percent of the total, the same percentage held in stable value funds. "The concentration in company stock is going down, but it's still a pretty large asset class," said Rob Austin, director of research at Alight. Thirty-one percent of plans that offer employer stock restrict how much of a new employee’s contributions can go into the stock or limit it to a chunk of the overall balance. That limits how much of a potential hit a worker can take from holding such a concentrated position in a stock.

- Assets in large-cap stocks in the plans surveyed rose to 23 percent of the total, from 21 percent in 2015, while money in stable value funds fell from 14 percent to 11 percent. Employer stock slid from 13 percent to 11 percent, and asset allocations to intermediate-term bonds rose to to 7 percent, from 5 percent. Allocations to the 14 other asset categories had the same percentage figures as in 2015.

- Three quarters of companies offer a Roth 401(k) option, up from 58 percent two years ago and 11 percent a decade ago.

- Over the past decade, the percentage of plans offering managed accounts from an outside vendor as an option has risen from 11 percent to 58 percent. These accounts offer a more personalized asset allocation for an extra fee. Just 14 percent of employees, on average, opted for a managed account in 2017, down from 16 percent in 2015 and 20 percent in 2013.

- The biggest change in the asset classes available to plan participants was a jump to 17 percent, from 12 percent in 2015, in the percentage of plans offering global equity investments. The asset classes that the plans were most likely to add were target date/target risk funds (27 percent), midcap equity (23 percent), and stable value (18 percent).

To contact the author of this story: Suzanne Woolley in New York at [email protected] To contact the editor responsible for this story: Peter Jeffrey at [email protected]