By Barry Ritholtz

(Bloomberg Opinion) --There are a lot of misconceptions about so-called corporate qualified plans, the best known of which are 401(k)s. Much of the misunderstanding stems from several articles about a Fidelity Investments report on how many of its clients had $1 million or more in their tax-deferred savings accounts, a group sometimes referred to as the 401(k) millionaires.

In the raucous online debate that ensued, some commentators suggested that saving $1 million was almost impossible. As someone who runs an asset-management firm with millions of dollars in qualified corporate 401(k) plans, I want to address this assertion. We will a) set the record straight on various dollar amounts that can be contributed to retirement plans; and b) outline a simple path for getting to $1 million.

First, the data: The typical 401(k) account holder can easily reach $1 million, mathematically; the hard part, like so much in investing, is having the discipline to set a plan and stick to it. To be sure, it is much easier said than done, but the rules make the $1 million goal very attainable.

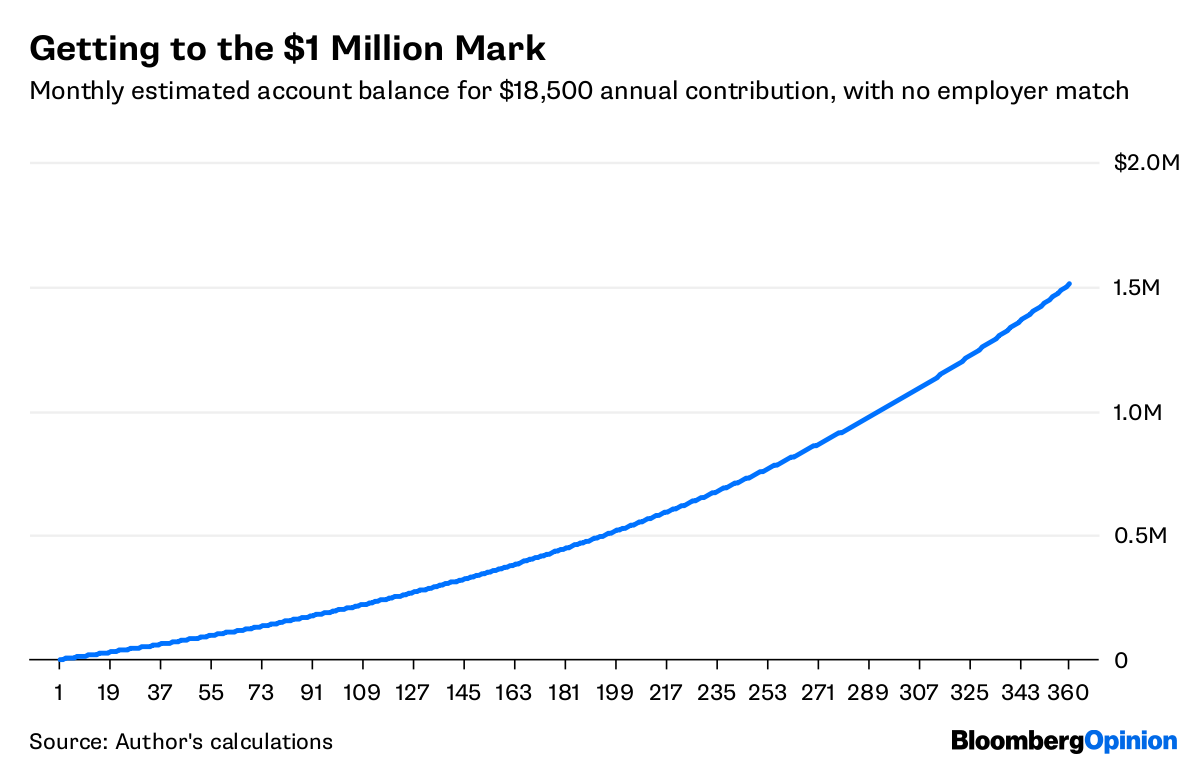

How do you get to $1 million? Well if you were just starting out today, it is really easy: assume a zero-starting balance, make the maximum annual pretax contribution of $18,500, generate investment returns of a mere 6 percent annually from a low-risk portfolio of 60 percent stocks and 40 percent bonds. Even without a matching contribution from your employer, in 30 years that will be worth $1,509,687.

Of course, all of this assumes you earn a decent salary, have the basics (food, rent, health care, etc.) covered, and max out your 401(k) every year. It also doesn’t take account of expenses charged by the 401(k) plan administrator.

The $18,500 contribution limit is for any employee under 50; for those over 50, an employee can contribute an additional $6,000 a year (or $500 per month). Over the course of a decade, I estimate that adds almost $100,000 to the total.

The contribution limits are inflation-indexed, and they go up over time — $18,500 is the 2018 limit, and it will likely increase (it was $7,000 in 1986; $15,000 in $2006, and $18,000 in 2016-17).

If you are fortunate enough to work for an employer that contributes a match of employees’ salaries to their 401(k), you begin to see even bigger gains. Using the same assumptions as above, the money piles up. The Internal Revenue Service rules allow employers to match an employee’s salary with as much as $55,000 in contributions, plus a $6,000 annual catch-up for employees over 50. The best-case results of our conservative scenario is three decades from now, an employee maxing out their 401(k) has a portfolio worth $4,489,838. Note this uses a low-risk and simple strategy to achieve that goal.

So in practice how easy is it to have already reached $1 million in your 401(k)? True, it requires diligence and income and discipline, but many people have indeed achieved this goal. By my estimate, there may well be a million people with more than $1 million in their 401(k) accounts already.

Here’s how I drew this conclusion. Let’s go back to the report that led to this 401(k) millionaire brouhaha in the first place: Fidelity. Here’s what the firm, one of the biggest mutual-fund companies in the world, reported:

The number of people with $1 million or more in their 401(k) increased to 157,000 at the end of Q1, a 45 percent increase from Q1 2017. Another 148,000 had saved that much in an IRA. Of those, 2,400 people had saved $1 million in both types of accounts.

That means this one firm holds tax-advantaged retirement accounts for 300,000 people with $1 million in savings.

Those are just the accounts at one firm (though it is true, it’s a pretty big firm with $6.9 trillion in assets under management). If we add in all of the other large custodians such as Charles Schwab and TD Bank; big fund managers such as Vanguard, BlackRock and State Street; and big brokerage firms such as UBS, Merrill Lynch and Morgan Stanley, the number of 401(k) millionaires adds up very quickly.

If there aren’t a million 401(k) millionaires already, there will be soon. For all we know, that milestone may have already been reached.

Winding up with $1 million in your 401(k) isn’t too hard — as long as you are willing to do the difficult things that need to be done to get there. Commitment, discipline and most of all, managing your own behavior is all that you need.

To contact the author of this story: Barry Ritholtz at [email protected]

For more columns from Bloomberg View, visit bloomberg.com/view