In our previous article, we looked at benefits payable to other family members and the maximum family benefit (MFB) for a worker’s retirement benefits. We’ll now move on to cover the MFB for survivor benefits. While there are similarities, the resulting benefits to family members can be dramatically different.

Primary Worker’s Social Security Benefit

Assume your client recently died at age 62 with a primary insurance amount (PIA) at his full retirement age ((FRA); assume age 66) of $2,000. He died before he started collecting benefits. As with Part 1 of this article, assume the spouse (age 56) doesn’t have sufficient credits to qualify for personal Social Security (SS) benefits and is too young for a spousal benefit. They have four children: two sons ages 19 and 16, and twin girls age 14.

The spouse has been told that there’s a maximum family benefit (MFB) applicable to family beneficiaries who are receiving benefits based on the deceased husband’s SS record. She would like to know how the MFB is determined and how it will impact their family benefits. She would also like to know the requirements and benefits applicable to each family member.

Let’s take a look at the benefits available to the surviving family members. Even though the spouse (age 56) isn’t yet eligible for a personal benefit, she may be eligible for a widow’s benefit when she reaches age 60. This would be the case if spouse didn’t remarry prior to age 60. At that point, she would be eligible for a reduced widow’s benefit based on the client’s SS record at his death.

To qualify for a widow’s benefit, the spouse must have been married to the client for nine months before his death. At age 60, the benefit would be 71.5 percent of her husband’s $2,000 PIA, with the percentage going up monthly until she reaches FRA. Because we assume the client’s death is in the current year (her age 56), the widow’s benefit won’t be applicable for another four years. Therefore, it won’t impact the current MFB.

If the spouse remarries prior to age 60, she won’t be eligible for any benefits based on the client’s SS record. If the remarriage is after age 60, she will continue to be eligible for benefits. If she waits until her FRA, she will qualify for 100 percent of the client’s PIA or her own retirement benefit if greater. We discussed the nuances of survivor benefits in “Social Security Survivor Benefits Simplified.”

Requirements

Children under the age of 18 (19 if in high school), or any age if disabled before age 22, will be eligible for survivor benefits so long as the client qualifies as “fully insured” (which generally means 10 years of previous SS earnings).

Children’s Benefit

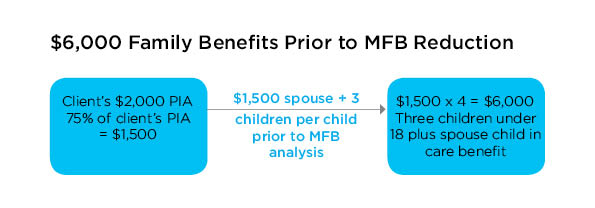

The children’s survivor benefit is $1,500 each (75 percent of your client’s $2,000 PIA) prior to any MFB reduction. This is higher than the 50 percent benefit available if the primary earner was still alive. The total unreduced benefit for the three children under age 18 will be $4,500 ($1,500 each). This benefit terminates as each child reaches age 18.

Child in Care Benefit

The spouse is too young to collect a spousal retirement benefit. But as with the retired worker, there’s a child in care benefit available to a surviving spouse at any age. The unreduced amount available if the spouse is caring for a child under age 16 is $1,500 (75 percent of the deceased spouse’s PIA). Only one benefit for a child under age 16 is allowed at a time. This benefit terminates when the child reaches age 16.

Dependent Parent’s Benefit

Note that the client’s parents may also be eligible for survivor benefits (not retirement benefits) if the client was providing at least 50 percent of their support. The minimum benefit is $1,650 (82.5 percent of your client’s $2,000 PIA). If he’s providing at least 50 percent support to both parents, the benefit amount is reduced to 75 percent of the PIA. In this case, we’ll assume your client wasn’t providing 50 percent financial support to either parent.

MFB Limits

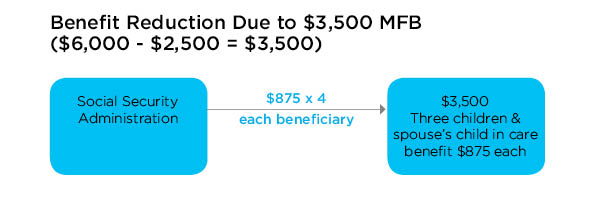

Now let’s look at the MFB on survivor benefits. As with the retirement benefits, the family’s total survivor benefits are limited by the MFB, although the calculations are somewhat different. The MFB is derived using a four-tiered “bend point” calculation. The MFB generally works out to be somewhere between 150 percent and 188 percent of the worker’s PIA. In this sample case, assume it’s calculated at 175 percent (175 percent x $2,000 = $3,500).

Benefit Summary

The surviving spouse is entitled to a 75 percent child in care benefit ($1,500 before MFB) for the child under age 16. The benefits for the three children under age 18 will also be 75 percent each (total $4,500). The total unreduced family benefit is thus $6,000, but the MFB is $3,500. The $2,500 excess will reduce the maximum total benefit from $6,000 to $3,500. The reduction will be split proportionally, so this will give the four beneficiaries a total of $875 each ($875 x 4 = $3,500).

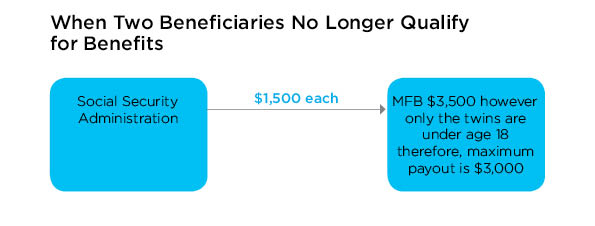

In two years, the 16-year-old son will be age 18 and the 14-year-old daughters will reach age 16. At that time, the son’s benefit and spouse’s Child in Care benefit will both terminate.

This leaves just the twin girls under age 18 as qualified beneficiaries. Their benefit will go up, but by how much? The maximum benefit for each beneficiary is $1,500 (75 percent of your client’s $2,000 PIA). Thus, the total benefit would be $3,000 ($1,500 x 2 = $3,000). In other words, the unreduced benefit would now be less that the MFB, so the MFB would no longer be applicable. As a result, the overall family benefit will decrease by $500 ($3,500 - $500 = $3,000). This will continue until twin girls reach age 18.

Difference Between Spousal Retirement and Survivor Benefits

It’s important to recognize the key differences between SS retirement and survivor benefits.

Retirement benefits. The maximum spousal retirement benefit is 50 percent of the worker’s PIA. It can begin as early as age 62. Deferred retirement credits (DRCs) of 8 percent per year, which are available if the worker delays collecting, aren’t included. The spousal benefit becomes available on a reduced basis at the spouse’s age 62. The children’s benefit and the child in care benefit are 50 percent each. For a spousal benefit to applicable, they must be married for at least one year.

Survivor benefits. The maximum spousal survivor benefit (widow’s benefit) is 100 percent (not 50 percent) of the worker’s retirement benefit, and it includes DRCs. It also becomes available two years earlier (on a reduced basis) at the spouse’s age 60. The children’s benefit and child in care benefit are 75 percent each. And don’t forget that parents’ benefits may also be applicable if providing 50 percent support to a parent. For the spousal benefit, they must be married at least nine months.

Disability. If disabled prior to FRA, the monthly disability benefit is the worker’s recalculated PIA. If disability continues until FRA, it will automatically convert from a disability benefit to a retirement benefit.

The earnings test. It will be applicable when any beneficiary has earnings in excess of $15,720 earnings limit and is collecting prior to FRA. Excess earnings will cause a $1 benefit reduction for every $2 of excess earnings, although the limit is more generous in the year FRA is reached. See “Qualifying for Social Security Retirement Benefits,” for more information on the earnings test.

In the year FRA is reached, the limit increases to $41,880 and $1 of benefits withheld every $3 of excess earnings.