Your clients probably think they know more about how their retirement plan works under the hood than they really do.

That’s a key finding of a quiz of more than 1,000 60- to 75-year-olds on retirement income, administered by the American College of Financial Services. The college, which trains financial planners, wanted to gauge how much Americans know about key retirement concepts - safe withdrawal rates, the relative risk of stocks and bonds, investment fees, longevity and the benefits of delayed Social Security filing.

The quiz was restricted to households with at least $100,000 in assets, although about 20 percent had considerably more ($500,000 - $1 million). So, this was a best-case scenario in that the quiz-takers were affluent households that have managed to save money for retirement. And in that sense, they are passing the test with flying colors.

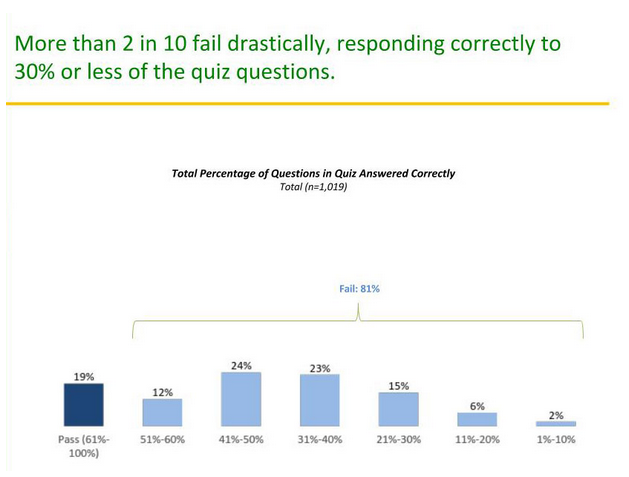

But most people flunked the quiz - 80 percent were unable to answer more than 60 percent of questions correctly. Yet more than half (55 percent) consider themselves well-prepared to meet their income needs in retirement, and almost all (91 percent) are at least moderately confident in their ability to achieve a secure retirement.

It’s not surprising that retirement savers don’t understand some of these concepts. After all, the financial planning community and top researchers can’t even agree on the definition of a safe withdrawal rate.

{kind=link}

And some of the questions asked here aren’t topics I’d really expect the average person to answer correctly. To wit:

-Only 39 percent understand that when interest rates rise significantly, the value of bond funds decrease significantly.

-Less than 10 percent understand that small company stock funds have a higher return over time than large company stock funds, dividend paying stock funds, or high yield bond funds.

-Only 36 percent know the circumstances when it is best to convert a traditional IRA into a Roth IRA. And, only 43 percent know that distributions from a Roth IRA are tax free after five years.

-Only 26 percent know that buying a $1,000 a month income with an immediate annuity will be more expensive for a younger person than an older one. And, only 13% know that the lifetime income payout rate for a 65-year-old male is roughly in the 6 percent to 7 percent range.

It would be reassuring if more people understood the benefits of a delayed Social Security filing (53 percent know that it’s best to wait until age 70 to claim if you think you’ll live to 90). On the other hand, this is a topic where many advisers get failing grades, too.

The study’s authors at the American College say the results point to a need for advisers to provide more education to clients. But, as I note in my column last week for Reuters, there just isn’t much evidence that average retirement savers have much appetite for learning more about the arcane details of retirement planning.

Also of interest: 63 percent of the survey respondents report that they have a financial adviser and see that person at least once a year, yet only 27 percent say they have a written financial plan. This suggests many don’t actually work with an actual financial planner, but think that they do.

Mark Miller is a journalist and author who writes about trends in retirement and aging. He is a columnist for Reuters and also contributes to Morningstar and the AARP magazine. Mark is the author of The Hard Times Guide to Retirement Security: Practical Strategies for Money, Work and Living. He edits RetirementRevised.com.