So-called 'socially responsible investing' and 'morally responsible investing' funds have enjoyed a rapid growth trajectory over the last five years. Assets in SRI or MRI funds grew from $202 billion in 2007 to $569 billion in 2010, according to the Social Investment Forum.

The performance of these funds, however, is still up for debate.

Socially responsible investing typically screens stocks according to non-financial principals, such as corporate governance, environmental records or employee practices. Morally responsible investing often looks more towards investments that adhere to moral codes or faith-based creeds, perhaps staying away from companies that sell tobacco, profit off of abortions or build military equipment. Just recently the Presbyterian church narrowly rejected a ban on church investments in companies that "support the Jewish occupation" of Palestinian territories, including Hewlett Packard, which manufactures biometric equipment used at checkpoints, and Caterpillar, which makes the trucks that are used to demolish Palestinian homes, according to a 2011 church report.

Regardless of the motives, the conventional wisdom has been that SRI clients were typically long on political and ethical commitment, but short on investing smarts. By using nonfinancial criteria to pick stocks, these investors were doomed to underperform—as would any broker foolish enough to take these clients on.

Morningstar currently tracks 191 SRI funds. On average, SRI funds across asset classes were down 2.47 percent for the year ending June 30, a time period when the S&P 500 returned 5.45 percent, according to Morningstar data. SRI funds were up 11.54 percent for the three years ending June 30 as the wider index rose 16.4 percent. Over five years the funds track the index a bit closer - returning .33 percent compared to .22 percent for the S&P 500.

The short-term underperformance isn't neccessarily a result of investing with the heart instead of the head - actively-managed funds overall didn’t perform much better. According to Morningstar, all U.S. actively-managed, non-SRI mutual funds returned 1.08 percent, 11.39 percent and 0.82 percent for the same one-year, three-year and five-year periods, respectively.

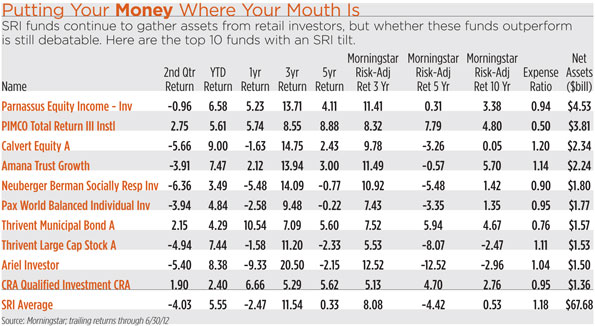

That said, risk-adjusted returns for SRI funds were lower than their trailing returns (see chart below).

Todd Rosenbluth, mutual fund analyst with S&P Capital IQ, says it’s impossible to compare SRI funds to each other because each one uses a different set of criteria. It makes more sense to compare them to their peer group. The Domini Social Equity Fund (DSEFX), for example, outperformed its large-cap blend peer group for the one-year, three-year, and five-year periods ending July 5. In addition, the fund owns a lot of stocks Rosenbluth likes from a fundamental, qualitative standpoint.

Rick Platte, co-portfolio manager to the Ave Maria Rising Dividend fund, argues that periods of underperformance of SRI and MRI funds are not due to any investment restrictions.

“Even when we’ve had periods of underperformance, there were reasons for that underperformance. It wasn’t like, ‘Oh, if we could’ve invested in that,’” Platte said. “I don’t think it’s been a significant factor where you look back and say, ‘We would’ve outperformed over the last three years if we could have invested in XYZ.’”

The Ave Maria Rising Dividend fund, which has about $275 million in assets, invests in about 40 companies that Platte believes have the capacity to increase their dividend payouts over time. Those names also have to conform to the screens established by the Catholic advisory board. If a company is involved in abortion or fetal stem cell research, makes contributions to Planned Parenthood, or is involved in pornography, out they go.

“People say, ‘does that really limit the number of companies you can invest in?’” Platte said. “It’s been more like 5 percent of the Russell 3000 that we can’t use. It’s not been huge, and it’s not been, to our sense, a great factor. But it is what it is, and there are certain companies that we can’t invest in.”

The Ave Maria Rising Dividend fund has outperformed the S&P 500 for the three- and five-year periods ending June 30, as well as since inception in May 2005. It has lagged behind the index over the past year.

Mel Lindauer, co-author of The Bogleheads' Guide to Investing and The Bogleheads' Guide to Retirement Planning, says just because a fund has a moral or social bent doesn’t mean it will underperform. Active funds in general tend to underperform their benchmarks over the long-term, he said.

“I think it's a ‘feel good’ story, and some investors choose to ‘put their money where their mouth is,’” Lindauer said. “They’re willing to accept possible lower returns in exchange for following their convictions, even though lower returns aren’t necessarily guaranteed. The fund may well outperform, too, depending on the fund management’s selections, but it’s still active investing.”

Rosenbluth says the performance of SRI really depends on the individual fund and whether it screens out companies or sectors that are in, or out, of favor.

The Ave Maria Rising Dividend fund, for example, screens out a lot of companies in the pharmaceutical industry because many produce abortifacients. Whether guided by providence or not, banning exposure to that underperforming sector turns out to have been a good break. “In some ways, it’s helped us inadvertently,” Platte said.