Most advisors ignore socially responsible funds. The conventional wisdom has been that SRI clients were typically long on political and ethical commitment, but short on investing smarts. By using nonfinancial criteria to pick stocks, these investors were doomed to underperform—as would any broker foolish enough to take these clients on.

But some social funds are worth a look—even if you never consider social screens. In fact, a handful of top social funds have sterling long-term records. In recent years more investors have begun to notice.

For the uninitiated, socially responsible investment funds are funds that screen potential investment targets for things like environmental impact, corporate governance or employment policies.

The funds report an increasing flow of assets from investors who have no interest in socially responsible investing (SRI). In fact, the Social Investment Forum found that net assets in SRI funds doubled to $641 billion from 2010 to 2012.

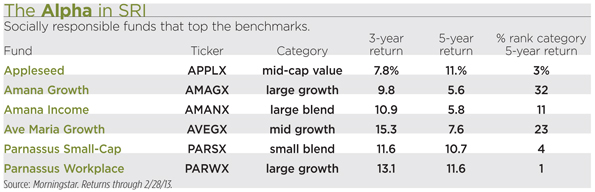

Consider Appleseed (APPLX), a social fund with $256 million in assets. Portfolio manager Adam Strauss says that only about half the assets come from SRI advisors. The rest of the shareholders have been drawn by an unusual strategy that produced notable results during the financial crisis. In the turmoil of 2008, Appleseed surpassed 99 percent of its mid value peers and outdid the Russell Mid Value index by 20 percentage points, according to Morningstar. During the rally of 2009, the fund returned 60 percent and topped 97 percent of peers.

The top social funds follow a variety of different strategies. Some are growth investors, while others are diehard value players. But they all employ distinctive approaches that deliver outstanding results. Among the value stars is Appleseed, which only takes stocks that sell at big discounts to their fair values. Instead of trying to stay broadly diversified, the managers bet heavily on a few bargain stocks and avoid sectors that appear expensive or risky. The fund currently has a big stake in consumer staples and no assets at all in basic materials. During the financial crisis, Appleseed avoided trouble by staying away from financials and other leveraged businesses.

When they can’t find bargains, the Appleseed managers sit on the sidelines. Lately the fund has had 30 percent of assets in cash and gold. That served as a drag on results during the rally of 2012. A favorite holding is office supply chain Staples. The shares have languished because investors worry that competition from Amazon will hurt sales. Portfolio manager Adam Strauss concedes that the Internet poses a threat, but he says that Staples generates steady cash flows by delivering supplies to corporate customers. “They have a gem of a delivery business that is not being destroyed by Amazon,” he says.

Another fund that excelled in downturns is Ave Maria Growth (AVEGX), which follows Catholic principles. Portfolio manager James Bashaw favors rock-solid companies that can be resilient in hard times. In 2008, the fund outdid 96 percent of its mid growth peers. Ave Maria looks for businesses with leading market positions and the potential to deliver above-average earnings growth. Typical holdings have strong balance sheets and reasonable valuations. The average holding has a return on equity of 26.5 percent, compared to 14.7 percent for the S&P 500.

A holding is Mastercard, a company with a sky-high return on equity of 43 percent. Long a dominant force in the credit-card business, the company stands to grow steadily as more consumers in the emerging markets gain access to charge accounts. Another holding is biotechnology star Gilead Sciences. “The company will grow rapidly by providing remedies for HIV and Hepatitis C,” says Bashaw.

Among the strongest performers of recent years is the Amana fund family, which follows Islamic law. Because the law forbids collecting interest, the funds cannot hold financials. Portfolio manager Nick Kaiser must also shun companies that profit from pork, tobacco, and gambling. The restrictions did not appear to hurt returns—and may have helped results. During the past 10 years, Amana Income (AMANX) outdid 99 percent of its large-blend peers, while Amana Growth (AMAGX) outdid 98 percent of competitors in the large growth category.

Kaiser favors established blue chips. He aims to buy when the stocks have slipped out of favor. “Even if the current numbers are a little weak, our companies can come back because they are really solid businesses in good industries,” he says.

When Kaiser can’t find bargains, he holds cash. During 2008, Amana Growth had up to 30 percent in cash. The big cash holding along with an absence of troubled financials enabled the fund to outdo 98 percent of peers for the year. When financials rebounded in 2009, the two Amana funds delivered middling results.

Amana Income ranks as the one of the least volatile members of its category. The portfolio owns stable dividend payers, such as Colgate-Palmolive and Exxon Mobil. Amana Growth seeks stocks that can grow steadily at rates of around 10 percent or 12 percent. Familiar names in the portfolio include International Business Machines and Johnson & Johnson.

Another notable SRI fund family is Parnassus. All of the company’s five equity funds finished in the top 10 percent of their categories for the past five years. At the top of the list is Parnassus Workplace (PARWX). During the past five years, the fund returned 11.6 percent annually, outdoing the S&P by 6 percentage points and topping 99 percent of peers in the large growth category. Jerome Dodson, who founded Parnassus and manages the Workplace fund, begins by looking for companies that treat employees well. Many holdings have appeared on Fortune’s annual list of the “100 Best Companies to Work For.” Dodson argues that such companies tend to have motivated workforces and solid management teams. Academic studies have shown that stocks on the Fortune list have outdone the S&P 500.

Dodson looks through the list of potential do-gooders to find stocks that are undervalued. His portfolio has a price-earnings ratio of 17.5, below the average figure for his category. He often takes unloved giants that have been delivering steady growth. Holdings include Microsoft and Procter & Gamble. Dodson also runs Parnassus Small-Cap (PARSX), which has outdone 96 percent of small blend peers during the past five years. The fund favors undervalued shares that have strong niches. A winning holding recently has been PulteGroup, a homebuilder that has soared along with the revival of housing markets.