Sponsored by iCapital Network

In wine production, prevailing conditions during the growing season influence vintage quality. Similarly, prevailing market conditions can impact private equity results.

A private equity fund’s “vintage” year, typically the year in which it makes its first investment, effectively starts the clock on the 10-year term of a typical fund. While volatility is not as dramatic in private markets as it is in the public markets, private markets are also subject to cycles. Funds of a certain vintage may benefit from investing into a low-valuation environment and a corresponding ability to ride an economic recovery. Other vintages may have the ill fortune of deploying most of their capital right before a market crash. Investors can help mitigate the impact of vintage performance volatility by allocating across multiple vintages and selecting high-quality investment managers.

Vintage Performance Is Hard to Predict

As most would acknowledge, attempting to forecast market conditions over a prolonged period is a futile exercise. Moreover, private equity fund lives are split into an investment period that typically lasts five years and a subsequent harvesting period, when the exit environment becomes more relevant. The fact that private equity fund investments are not made in one lump sum, but rather the committed capital is deployed over several years, gives managers a fair amount of flexibility to time their entry and exit points. This makes it impossible to predict the predominant investment environment for a given fund.

For a sharpshooting, vintage-timing approach to be successful, one would have to know in advance not just which multi-year period will present the most favorable investment environment for a given strategy, but that the selected manager will, in fact, deploy the majority of their capital during that concentrated period. In other words, trying to cherry pick vintage years for private equity would require exceptional market foresight and macro timing.

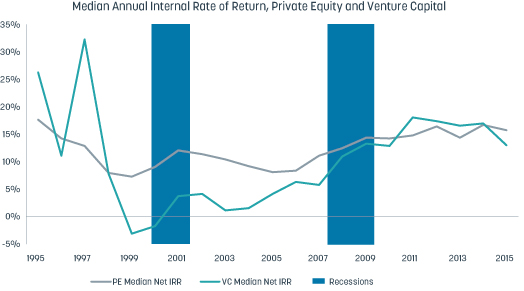

To provide an example, one might assume that buyout and venture capital funds would tend to perform similarly across cycles. In fact, as shown in Figure 1, buyout and venture capital returns have exhibited meaningful counter-cyclicality, despite both being equity oriented. Timing the markets in the context of performing fundamental analysis on individual, liquid stocks is difficult enough. Given the nature of private equity fund investing, a vintage selection approach that attempts to predict both market conditions and the performance of specific strategies far into the future has a slim chance of consistent success. This underscores the basic need to construct private equity allocations that are diversified by manager, strategy, and vintage.

Figure 1: Vintage Year Returns Typically Have Low Correlations with Market Cycles

Median Annual Internal Rate of Return, Private Equity and Venture Capital

For illustrative and informative purposes only. Source: Preqin All PE and VC benchmarks, as of December 31, 2018.

High-Quality Managers Can Perform Well in Any Market

Effective private equity investors typically find that the best strategy is to focus on finding experienced managers who can take advantage of favorable investment conditions when they occur (effectively, buying low, selling higher, and taking advantage of secular growth along the way). It is also important that these managers have the networks, discipline, and industry expertise to avoid overpaying in frothy markets, develop and execute clear value creation plans at portfolio companies, and identify the most accretive selling opportunities in any given market environment.

The Importance of Peer Comparison

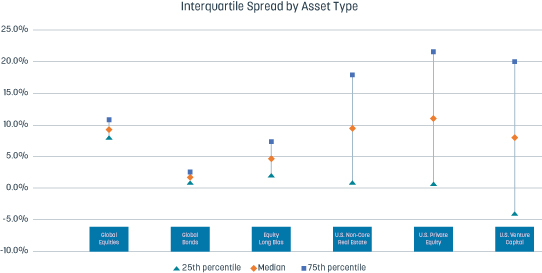

A superior winery tends to produce a better product on average across vintages. Similarly, experienced, talented private equity managers demonstrate the ability to consistently add value in both bull and bear markets. Separating these superior managers from the pack requires comparing their returns with those of other funds of comparable size and strategy in the same vintage year. It also requires parsing out how much of the return was generated by multiple expansion (effectively, private equity beta driven by market conditions), versus by revenue and EBITDA growth in their underlying portfolio companies (a strong proxy for private equity alpha, particularly in down markets). As shown in Figure 2, the spread between private equity beta and the asset class’ top-performing funds can exceed 1,000 basis points.

Figure 2: Private Equity’s High Interquartile

Sources: Lipper, NCREIF, Cambridge Associates, HFRI, J.P. Morgan Asset Management. For illustrative purposes only. Global equities (large cap) and global bonds dispersion are based on the world large stock and world bond categories, respectively. Manager dispersion is based on 2013 –2018 annual returns for global equities, global bonds, U.S. core real estate and hedge funds. U.S. non-core real estate, U.S. private equity and U.S. venture capital are represented by the 5-year horizon internal rate of return (IRR). Data is as of December 31, 2018.

Consider a Vintage Diversification Program

In sum, manager selection in private equity is far more important than vintage selection and has the added virtue of being a feasible exercise. Further, successful private equity investors tend to commit capital not just to top-quartile managers but across vintage years. A steady allocation pace across vintages adds critical diversification both within private equity allocations and in the context of the broader portfolio. Allocating across vintages also allows an investor to build out a systematic private equity program that eventually becomes self-funding by producing a distribution stream that can be reinvested (or distributed as income).

Investors seeking to build a diversified private equity allocation may wish to consider a vintage investing program constructed with vintage-specific, multi-manager funds. These funds typically provide access to carefully vetted private equity funds within a single vintage year. By including multiple vintage year funds in a private equity allocation, investors can gain diversified sector and vintage exposure, often at lower investment minimums.

Kunal Shah, Head of Private Equity Solutions, iCapital Network

Tatiana Esipovich, AVP, Research & Due Diligence, iCapital Network

END NOTES

1. Source: Preqin, as of December 31, 2018.

IMPORTANT INFORMATION

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as legal, tax or investment advice, a recommendation, or as an offer to sell, a solicitation of an offer to purchase or a recommendation of any interest in any fund or security offered by iCapital. Past performance is not indicative of future results. Alternative investments are complex, speculative investment vehicles and are not suitable for all investors. An investment in an alternative investment entails a high degree of risk and no assurance can be given that any alternative investment fund’s investment objectives will be achieved or that investors will receive a return of their capital. The information contained herein is subject to change and is also incomplete. This industry information and its importance is an opinion only and should not be relied upon as the only important information available. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. Securities may be offered through iCapital Securities, LLC, a registered broker dealer, member of FINRA and SIPC and subsidiary of Institutional Capital Network, Inc. All rights reserved.