Every dog has its day, and in 2012, the battered financial sector—truly a pack of mangy hounds—had its year, with stocks in the S&P Financial Group leading all sectors, rising 27 percent for the year, almost twice the S&P’s return of 15 percent.

Bank of America (Ticker: BAC) and Citigroup (Ticker: C) were among the strongest performers, as BofA rose more than 50 percent and Citi almost 40 percent. These once-scorned names staged a relief rally as potential settlements in the ongoing mortgage fraud litigation that has embroiled the industry became more likely. Losses from home loans and consumer lending portfolios also slowed. Once on life support, the group now seems closer to shedding its pariah status amongst investors. And the wealth management units of these companies, which still underperformed on a historical basis, are closer to gaining traction than at any time since the 2008 financial crisis.

For advisors considering investing in the group, and for those working at large firms receiving compensation in restricted stock or options, looking at wealth management stocks and wealth management units at large banks seems timely. And while many industry execs are wary about the outlook for 2013, there is still a long-term strategic commitment to the space.

Wealth management has always been an attractive opportunity for both large and regional banks. Margins in these units have generally been healthy over time, and while currently depressed, the potential for increased profitability is clear.

“With no regulatory changes, wealth management units can get 20 percent operating margins in favorable environments, as Merrill Lynch did in 2005,” says Brad Hintz, an analyst at Alliance Bernstein who covers the group. “This operating margin profile compares favorably to other financial services firms and units, and this will continue to drive capital investment in this group by the large players.”

Even formerly institutional-focused trading and capital markets shops have a renewed appetite for retail wealth management. Part of the appeal is regulatory. “Wealth management is not affected by Basel III requirements on capital levels,” observes Michael Wong of Morningstar, leaving firms free to grow this business without expanding their balance sheets.

Wall Street heavies like Morgan Stanley and J.P. Morgan are no longer focused so exclusively on servicing the institutional client base and have begun to embrace a fee-driven model, instead of commissions. “Advisors got 46 percent of revenue from fees in 2012, and 45 percent from commissions, but expect to get 55 percent in 2015 from fees,” says Tyler Cloherty of Cerrulli and Associates, an industry research firm.

With wealth management assets proving to be far “stickier,” less subject to pricing erosion from technological competition, and more amenable to paying for service and advice, these firms are now realizing that wealth management is a crucial pillar in stabilizing their earnings. Hintz notes that Morgan Stanley (Ticker: MS) has 11 percent operating margins in its wealth management group, leaving plenty of room for improvement, particularly as it gets closer to their goal of generating 50 percent of earnings from wealth management. “JPM relies on institutional capital markets and Jamie Dimon, their CEO, has been clear he is trying to build their wealth management presence,” says Hintz.

The key is attracting retail investors to the markets, and they are still skittish after the 2008 meltdown, and still concerned about their employment status. “Retail brokerage revenues are correlated to non-farm payroll results, and we are still a long way from a strong employment outlook,” says Hintz. “Retail investing cycles are long. After the 1987 crash, the retail investor did not return to the market for four years. If you look at the results from companies like Charles Schwab, a pure play on retail investors, you are not seeing the retail investor jump back in with any enthusiasm.”

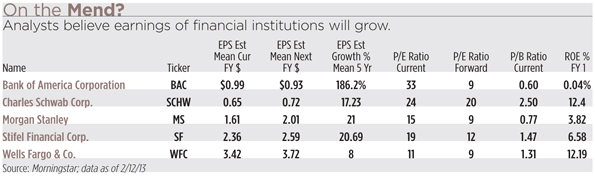

Unfortunately for investors seeking to play this rebound in large-cap names, the largest financial firms are too diversified to be driven by wealth management results. “The wealth management groups at BAC or WFC [Wells Fargo] are too small to drive profitability. Morgan Stanley is the best pure play on wealth management because of their long-term commitment to building this unit into a top performer,” says Hintz.

There are other names that investors can consider as a play on this sector. Charles Schwab (Ticker: SCHW), the leading discount retail brokerage, has built a highly recognized brand name, a top notch online presence, and a formidable asset base, spread amongst active traders, buy-and-hold mutual fund investors, and small and independent RIAs who outsource back-office functions to Schwab Advisor Services.

“The story with Schwab is simple and straightforward,” says Gaston Ceron, an analyst at Morningstar. “They have two main buckets of revenue: interest rate sensitive assets and trading revenues. Both have been in non-optimal environments; that has depressed results. Low interest rates have hurt net interest margins even as AUM has increased. 2012 was not a good year for trading results. Any rise in rates or improvements in trading will drive SCHW stock,” says Ceron, who believes it is still too early in 2013 to ascertain a trend for this year.

Still, Ceron believes there is plenty of room for improvement. He thinks return on equity could go from the current 11 to 12 percent range to a peak number in the upper teens or low 20-percent range. Earnings per share, which he expects to be $0.70 for 2013, also has plenty of room for improvement. EPS could reach $1.70 in more favorable interest rate and trading environments, and with the stock currently hovering around $17, this makes Schwab a bargain if you believe these results improve in 2013 or 2014.

Stifel Financial (Ticker: SF) is another play on wealth management, having built on a series of acquisitions, including this just approved deal to acquire KBW. Stifel has been a remarkable performer over the last decade, showing both prescience and good fortune in moving to a bank holding model before the crisis, executing a string of savvy acquisitions in capital markets and wealth management, and avoiding the mortgage meltdown. But the stock is fairly valued; Wong at Morningstar has a $36 price target, and with the stock at $38 or so, there doesn’t seem to be great upside. And the firm does not deserve a premium multiple. “SF is a serial acquirer and has shown discipline, avoiding overpaying for Morgan Keegan. But the ROE and ROIC results are not fantastic,” says Wong, who assigns a 16.5x p/e multiple when deriving his price target, a reasonable view given the firm’s 6.5 percent ROE in 2012.

For advisors looking to find stocks to play a rise in interest rates and retail trading, there are few attractive pure plays left. SCHW is probably the best of the bunch, while SF would be an attractive purchase on any pullback below $30. Morgan Stanley is the best wirehouse play on these trends.

To get complete exposure to the financial sector, consider Select Sector SPDR-Financial (Ticker: XLF); the ETF is one way to play interest rates, as are the large banks with wealth management units, like BofA and Wells Fargo.