By Brian Gartner and Matthew Phillips

Wealthy U.S. families are increasingly utilizing Private Placement Life Insurance to enhance their after-tax investment returns.

With the passage of the Tax Cuts and Jobs Act of 2017 the investment portfolios of many wealthy individuals and their families will be subject to a higher level of income tax, resulting in lower net after-tax returns in their investment portfolios. While the highest bracket for federal income tax was reduced from 39.6 percent to 37 percent, high-net-worth families are generally experiencing a higher effective tax rate on their investment portfolio. Additionally, and often overlooked, most investment management fees are no longer deductible under the new law, further impacting the after-tax returns delivered to investors.

What Is PPLI and How Does It Work?

PPLI is institutionally priced variable life insurance, available only to qualified purchasers and accredited investors, that offers the ability to allocate to both registered (mutual) and non-registered (alternative investment) funds in a tax-efficient manner.

The values inside a PPLI account grow tax-deferred and a large percentage (approximately 85 percent) of the account value can be accessed income tax-free during the insured person’s lifetime via withdrawals of cost basis and income tax-free policy loans. At the death of the insured, the remaining values not accessed during the insured’s lifetime are paid to the beneficiary(ies) as an income tax-free life insurance benefit. PPLI policies are generally structured with the smallest amount of life insurance possible, in accordance with the Internal Revenue Service’s tax rules, in order to minimize the annual fees of the structure. The annualized fees associated with PPLI are, in general, significantly lower than the income taxes that would be payable on a taxable investment portfolio.

Like any variable life policy, policy owners can allocate PPLI account values to any investment made available by the issuing insurance company. The menu of investment options has expanded dramatically in recent years, and for clients making sizable investments in PPLI, it may be possible to create a customized investment offering tailored to meet their objectives.

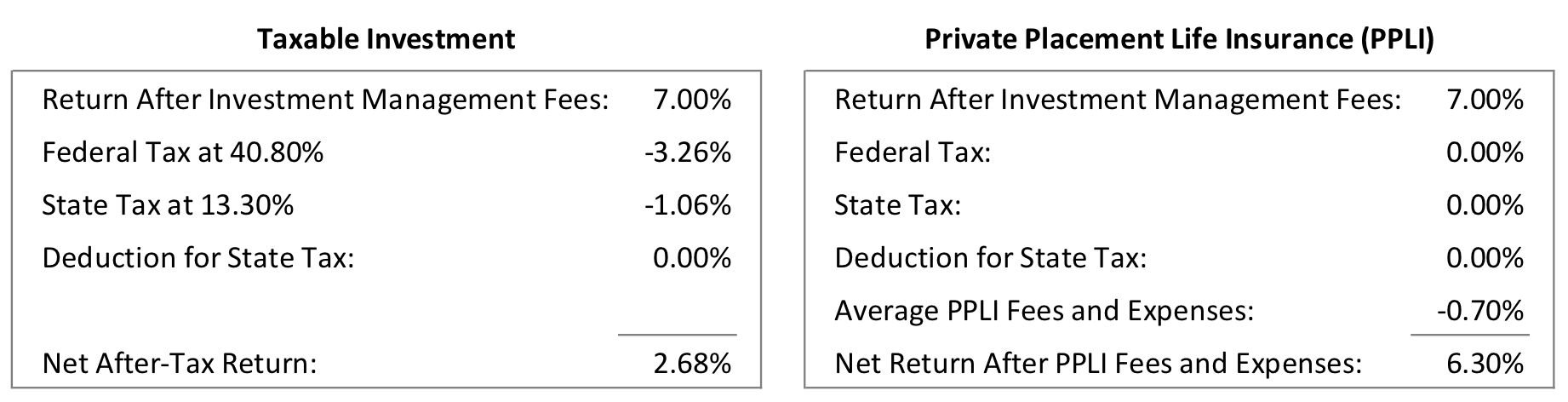

The general value proposition is that the expense of the PPLI account is significantly less than income taxes, creating higher after-tax returns. As seen in the table below, for a California resident investing in a taxable investment account, assuming a 7 percent return net of a 1 percent non-deductible investment management fee, and assuming that 100 percent of the gains are subject to income taxes at ordinary rates, income taxes equal 432 basis points. As a result, a 7 percent return in a taxable investment account nets to an after-tax return of 2.68 percent. In comparison, the annualized expense of a PPLI account is in the range of 70 bps over the lifetime of the insured. Here, a 7 percent return net of investment management fees inside PPLI nets to an after-tax return of 6.30 percent.

To the extent that the annualized expense of the PPLI account is lower than the impact of taxes in a taxable investment account, the incremental compounding inside the PPLI account will create substantial after-tax wealth over time. Many affluent families are concluding that allocating to tax-inefficient asset classes, such as credit funds, direct lending funds, and hedge funds, through a PPLI structure that can be beneficial regardless of whether they plan to access the values during the insured’s lifetime or leave them inside the PPLI account to compound for the benefit of future generations.

How Can PPLI Be Structured to Maximize Family Wealth?

PPLI can be used in conjunction with grantor trusts for the benefit of heirs to further enhance a family’s economic results. Income taxes generated by investment gains inside a grantor trust are paid by the grantor. This status is beneficial for the trust that can compound the investment returns income tax-free, but not for the grantor who bears the burden of paying income tax generated by the growth of trust assets. If the trust investments are made through PPLI, the grantor’s income tax liability will be eliminated, and the trust assets will continue to accumulate tax-free. Trust investments through PPLI compound at a slightly reduced return to pay for the PPLI fees and charges, however, the grantor’s tax liability on PPLI investments will be eliminated. Alternatively, PPLI can be structured inside of non-grantor trusts in order to mitigate the trust’s income tax burden generated by investment gains.

Trustees are attracted to PPLI in the context of multigenerational trust planning for three main reasons: (1) assets within a trust allocated through PPLI grow on an income tax-deferred basis; (2) the trustee can make income tax-free distributions to trust beneficiaries from PPLI without having to consider the income tax consequences of liquidating assets; and (3) the trust will eventually receive an income tax-free insurance benefit, which will serve to effectively step-up the basis of the assets within the trust that are allocated through PPLI.

By insuring younger generations, instead of senior generations, the duration of income tax-free compounding can be extended, which further improves the long-term economics of the trust investments.

While PPLI is particularly impactful in the context of trust planning, many individuals choose to optimize investments they’re making on their own balance sheet by utilizing personally-owned PPLI as well.

Additional Considerations

A key component of PPLI is the owner’s ability to allocate to a customized investment option, or allocate (or reallocate) to any number of investment options made available by the insurance company without ever incurring income tax generated by investment gains. Investment managers are entering the private placement market with new investment options at a greater rate than ever before. As a result, it’s easier than ever to build out a well-diversified portfolio within PPLI accounts. That said, PPLI is not for everyone. To optimize the investment, PPLI requires an investor with a mid-to-long-term time horizon.

Whenever high-net-worth families are allocating to third-party managers, and are subject to income taxes on their investment portfolio, PPLI can be a powerful tool to consider. The recent tax law changes, coupled with the increasing number of available investment options, make for a particularly interesting time to explore PPLI as a tax-efficient investment solution.

PPLI is an unregistered securities product and is not subject to the same regulatory requirements as registered variable products. As such, Private Placement Life Insurance or Annuities should only be presented to accredited investors or qualified purchasers as described by the Securities Act of 1933. Variable life insurance products are long-term investments and may not be suitable for all investors. An investment in variable life insurance is subject to fluctuating values of the underlying investment options and it entails risk, including the possible loss of principal.

Brian Gartner is a director and Matthew Phillips is a principal, both with Winged Keel Group.