Most executives rightly focus on their offensive strategy—saving and investing—but a defensive strategy is essential, too. As high earners, executives are often in a position to self-insure for some potential needs, but in almost all situations there remain gaps to fill with wisely chosen insurance strategies.

Essentially “delegating” defensive strategy to an HR department—in the form of workplace-provided policies—is unlikely to be wise. Ideally, a risk-aware strategy will include some base components available through the workplace, such as group disability and life insurance policies, augmented by tailored products purchased personally.

Across both workplace and personal products, there are subtleties to consider as you plan your defensive strategy. This article explores strategies and tips for executives across disability and life insurance and also touches briefly on other needs.

Disability Insurance

Long-term disability insurance can sometimes be overlooked when putting together a comprehensive insurance plan. The Social Security Administration estimates that more than one in four 20-year-olds will become disabled and unable to work at some point before they reach the age of 67. The details of long-term disability coverage are especially critical for highly compensated individuals to consider carefully, as most disability insurance structures don’t cover the full amount of income they stand to lose.

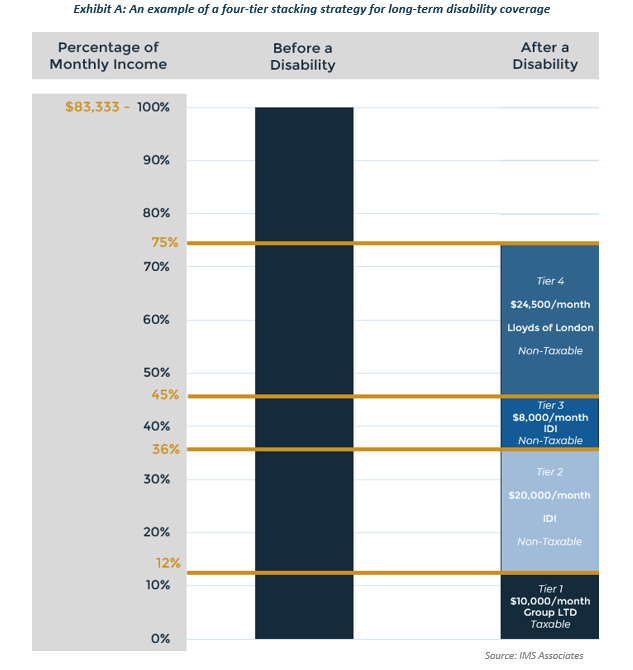

Consider, for example, an executive earning $1,000,000 per year, or $83,333 per month. Maxing out a typical group policy will cover only $10,000 (or perhaps up to $15,000, in other common policy structures)—just a drop in the bucket. That $10,000 coverage serves as the base, “Tier 1” amount in Exhibit A, below.

Because insurance carriers may be willing to cover, in aggregate, up to about 75% of income, this executive may be wise to augment the workplace policy in a “stacking” strategy. The goal of stacking is to obtain the best possible disability coverage with multiple policies. Where you apply to, when you apply and how much you apply for really matter. Disability insurers have maximum benefit amounts they will issue depending on the underlying circumstances. Strategically applying will not only save on premium costs but also maximize coverage.

Working with an independent broker, this executive found coverage for another $52,500/month through traditional, individually owned means. Specifically, the executive found $28,000/month through traditional means: $20,000 through one company and $8,000 through another. Then, additional coverage of $24,500/month was secured through Lloyd’s of London as “excess disability coverage.”

By using four different carriers, this executive was able to fully maximize coverage to protect 75% of their income! Now, if something were to happen, this executive’s income situation is likely nearly the same, net of taxes. (Important note: Be sure to personally pay premiums where applicable so the benefit will be tax-free in the event of a claim!).

Here are some additional tips for getting more coverage at less cost:

- Enhanced group coverage. Talk to HR about increasing the group coverage threshold (Tier 1)

- Multilife discounts. Personally apply with multiple colleagues to obtain group discounts (Tiers 2 and 3)

- Group excess coverage. Talk to HR about offering group excess coverage which may provide for additional discounts (Tier 4)

Finally, consider these important notes about excess coverage: Typically, Lloyd’s of London will guarantee premiums for seven years and provide disability payments for five years, as Lloyd’s does not want to be on the hook forever. You can also obtain a lump sum benefit on top of this. The idea is that as an executive, you should save a lot of money every year so you can reassess your ability to self-insure along the way. If a claim occurs, a lump sum can be invested, in addition to your other assets, to allow you and your family to live the lifestyle you have been accustomed to living. You can reapply every seven years or sooner.

Life Insurance

Start with the need, not the product. Many people get caught up with the cash value component of permanent insurance and end up buying something they don’t need. Think about all of the other insurance policies you own. Do any of them come with a cash value component? Not unless it’s a health savings account, which arguably is not an insurance policy. So why should this be any different? Pay the minimum amount of money for the right amount of insurance to transfer the risk.

Most insurance needs can be covered by term coverage (10, 15, 20 or 30 years). Across these time thresholds, common insurance needs include:

- Covering outstanding debt (match the debt terms)

- Paying for education costs

- Replacing income

- Paying estate taxes/providing liquidity at death (permanent need)

Don’t be afraid to purchase multiple term policies with staggering terms. For example, if college is 10 years away, a 10-year policy will do the trick. If a mortgage will be paid off in 15 years, don’t buy a 20-year policy, etc. This will typically save costs in the aggregate. Note: once a death benefit reaches $1 million for term coverage, there will be no additional discount available.

If there is a need or desire for permanent coverage, beware of the underlying assumptions with “off-the-shelf products.” Illustrations can be manipulated to show staggering amounts of cash value and rates of return. That said, the insurance company has the right to increase internal insurance costs and can reduce the rate of return down to a stated minimum (noted in the fine print). If either of these two events occur, the performance becomes sub-optimal. Even if these events do not occur, performance tends to lag expectations, in my experience. Guaranteed coverage is often a good idea.

Executives are usually accredited investors, which means they qualify for private placement life insurance (PPLI). This product is not “off-the-shelf.” Once qualified, the internal insurance costs are much less than retail products and the investment options are more robust (hedge funds, private equity, private credit, etc). Investing in PPLI is often a way more efficient way to obtain coverage in tandem with cash accumulation versus buying a retail product.

When it comes to underwriting, understand how the Medical Insurance Bureau works (MIB). Once a formal life insurance application is processed, personal health details become visible to the MIB, permanently! Apply “informally” first so if there are any adverse health concerns, there is ample time to make adjustments before the MIB and insurance carriers know about it—don’t get blacklisted. Stacking is applicable here as well if there is a larger need for coverage. Also keep in mind that insurance carriers look at the lives they insure as a portfolio. For example, if they want to increase exposure to males from the age of 45-50 who smoke, they may become more competitive for a period of time.

Other Types of Insurance

To protect “exposed” assets (i.e., those not in trusts), personal liability coverage is tremendously important. Obtaining an umbrella policy is a smart move and typically inexpensive. Match the umbrella coverage with the amount of assets exposed, at a minimum. Keep in mind that if you get sued, the insurance company may send their own lawyers to represent you because they don’t want to pay up. Talk to HR about this as well—group umbrella coverage can lead to some savings.

Most executives tend to self-insure for long-term care issues, but to the extent you want to sleep better at night, there are hybrid long-term care insurance products. Rather than pay premiums in the traditional “use it or lose it” sense, there is a better way. For example, in an example received from one insurance company in 2019, a 40-year-old male can give an insurance company $100,000 and opt to receive either $562,000 of total long-term-care coverage inflating annually, a $320,000 death benefit, or have the right to get their money back in full after five years. There is potentially a lost opportunity cost here, but this tends to be a more efficient use of assets.

Other common areas for executive insurance tend to include, but are not limited to, the following:

- Directors and officers liability/Outside directors liability

- Employment practices liability

- Fiduciary liability

- Crime

- Kidnap and ransom

- Liability arising from the activities of employed lawyers

Across the basic categories of disability and life, as well as these additional potential needs, executives need to assess risk by thinking through their financial situation and make sure they are sufficiently covered, even if that means going beyond what’s offered through the workplace.

Kevin Couper, CFP, is a senior vice president with Wealthspire Advisors.