Yale is among the finest learning institutions in the world. It’s known for many great things, but in the investment world, it’s probably best known for its top performing endowment, which many try to replicate with what’s called an “endowment model.” What can individual investors learn from the Yale endowment? Maybe how to not invest if you have to pay taxes.

Endowment Models

Over the past five to ten years, I’ve seen a large increase in firms selling ultra-high-net-worth (UHNW) investors (individuals and families who have liquid investable assets excluding real estate of $50 million or more), endowment style investment portfolios and limited partnership fund of funds.

Why might this initially appear to make sense? Many UHNW investors have no debt, consume a small portion of their assets for annual expenses and are really investing for future beneficiaries or to be able to give more in the future to charity. Some have even set up trusts in jurisdictions like Delaware that allow family trusts to run for more than 100 years (so called dynasty trusts). Because of this, UHNW investors commonly view their time horizon for family trusts in generations, not years or decades.

What does a trust that’s investing over a very long-term timeframe for the benefit of generations to come sound like? Maybe an endowment?

If UHNW trusts have characteristics that resemble endowments, and Yale arguably has one of the best endowments from an investment standpoint, shouldn’t more UHNW portfolios look like Yale?

Many investment managers and advisors certainly suggest this. Over the years, I’ve seen firms craft pitches for UHNW wealth families that sound something like this:

“You have more money than you can possibly spend in a lifetime and are now really investing for the benefit of generations to come. Because you have such a long-term timeframe and have the access that your success brings, shouldn’t you be investing the same way some of the most successful investors in the world invest? Shouldn’t you be investing like Yale in an endowment like model? The risk-adjusted returns and strategies that we can implement on your behalf using an endowment style limited partnership or approach are compelling.”

The Catch

What’s the problem with using an endowment approach? At least three: fees, performance and taxes.

Every endowment approach I’ve ever seen has one thing in common: a sizable allocation to hedge funds.

A great deal has been written in academic studies and the media about the high fees associated with hedge funds. More is starting to surface about hedge fund performance comparing unfavorably to low cost, simple, diversified portfolios of index funds that have the same historical risk adjusted returns and volatility (feel free to reach out to us for our analysis of this – my hedge fund friends might de-friend me if I post it publicly).

Not as much has made the press, however, about what really makes UHNW investing different from endowments, namely, taxes.

Yes, taxes. Regardless of your political leanings, no one likes writing a big check to the Internal Revenue Service, but the IRS is a fact we can’t avoid.

Recent tax law changes have made the subject of taxes even more important as it relates to investments. Tax law changes that became effective Jan 1, 2013 include a top short-term gain rate of 39.6 percent, a long-term gain rate of 20.0 percent, an additional 3.8 percent tax on net investment income (the Medicare tax) and an effective additional 1.2 percent rate increase due to the phase-out of deductions for top-bracket taxpayers (the Pease phase-out). These tax changes combine to create a 44.6 percent tax on short-term gains and ordinary income and a 25.0 percent tax on long-term gains and dividend income. And this rate only takes into account federal taxes. Many states such as California, which has one of the largest collections of UHNW individuals in the United States, impose a substantial additional tax burden.

Words of Caution

When I’m helping UHNW investors free up funds around tax time to pay bills due for large realized gains on hedge funds, I often raise words of caution about these investments.

Endowment model investment presentations, which typically include sizable allocations to hedge funds, are complex, well done and often presented by well educated and well heeled professionals. The pitches can be impressive and hard to resist. What they often don’t point out, however, is that allocations to hedge funds often generate large short-term gains, which now carry with them a 44.6 percent federal tax or reduction of return for taxable investors.

So, what has made me write of this subject now? Well, the dreaded April 15th tax date has recently passed, so conversations about this subject with our UHNW investors are top of mind.

In addition, credit must be given to a tax aware investment firm in California, Aperio Group. I shamelessly took the title of this post from one of their recent papers. The full research report can be found here.

Index Funds

Inspiration also comes from the long-time Chief Investment Officer of the Yale endowment, David Swensen. Swensen is considered one of the most successful investors in the world and, based on his use of non-traditional investments such as hedge funds, a major contributor to the endowment investment model. Following thoughts from Swensen’s first book in 2000, Pioneering Portfolio Management, many UHNW advisors started promoting the endowment model. The UHNW investment world eagerly embraced this new “sophisticated” approach and yet, going on 15 years later, still seems to be forgetting the fact that Swensen’s book was designed for tax-exempt investors.

Even though Yale has generated top returns for its beneficiaries through the use of hedge funds, what does Swensen, like many other successful investors such as Warren Buffett, suggest for taxable investors?

Index funds.

Why?

Well, the following quote from his second book (this one for taxable investors), Unconventional Success may say it best:

“The management of taxable…assets without considering the consequences of trading activity represents a…little considered scandal. A serious fiduciary with responsibility for taxable assets recognizes that only extraordinary circumstances justify deviation from a simple strategy…”

Unconventional Success

Beyond Swensen, what Aperio has done better than almost anyone else I’ve seen is provide sophisticated evidence to counter some of the sophisticated endowment style presentations. Their research suggests that when you properly account for the tax drag, hedge funds should have little, if any, place inside taxable portfolios.

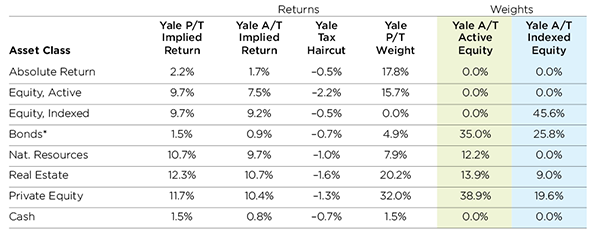

Aperio collected endowment asset allocations and asset class return, volatility and correlation data from multiple third party sources, including Yale’s annual report and an independent study of endowments by the Commonfund and the National Association of College and University Business Offices (NACUBO).1

Aperio took these data and, using detailed and well-accepted analytical processes, calculated pre-tax and after-tax returns for Yale’s asset classes. Then, using an allocation optimizer, they generated a tax-adjusted optimal asset allocation - evaluating, in other words, what Yale might do differently if it were taxable.

Below is a chart that illustrates findings from their work. The yellow column presumes that the equity allocation in the portfolio is available only through active strategies, while the blue column presumes that indexed equities are also available.

Notice that the allocations to Absolute Return (a term Aperio used as a proxy for hedge funds) and Active Equity shift to 0.0 percent when factoring in taxes.2

Low Correlation to Equities

Aperio concludes: “Given that an investor now has to pay taxes on what had been a tax-exempt portfolio, suddenly active equity and absolute return (hedge fund) allocations become far less attractive.”

Importantly, Aperio reached this conclusion even while assuming that hedge fund or Absolute Return strategies had a low correlation to equities and so offered diversification benefits. In fact, many hedge funds have relatively high correlation to equities (a well respected hedge fund index, the HFRI Fund Weighted Composite has a 0.88 correlation to equities), making the case against using them for diversification even less attractive. In Aperio’s words: “If a hedge fund strategy reflects the risk patterns of the HFRI index, with its higher correlation to equities, then the model never allocates anything to hedge funds.”

Lest you think that there’s anything unique about Yale, Aperio performed similar pre-tax and after-tax analyses across the previously mentioned Commonfund and NACUBO study of the allocations and performance of all U.S. endowments. The conclusions they reached from these data were the same: allocations to hedge fund and active equity strategies shift to zero in a taxable environment.3

Where does this all leave us as it relates to the title of this article?

If you’re a taxable investor, be wary of complex strategies that don’t factor in taxes.

Some hedge fund managers are outliers and have produced returns that on an after-tax basis might warrant inclusion in UHNW portfolios, but the work by Aperio and words of David Swensen continue to lead us to recommend that all investors, small and large, maintain a high percentage of keep-it-simple, low fee, fully transparent, tax efficient investments.

What types of investments should more UHNW investors use to try to achieve solid returns like Yale?

The evidence continues to point to index funds.

Endnotes

1. To learn more about how your own alma mater is invested, view a summary of the report: at the following:

NACUBO: 2014 Commonfund Study of Endowments

2. Aperio suggests that if you use tax-efficient index strategies, such as the ones that they provide, you can allocate more to certain types of hedge funds that have low correlation to equities. I’m a little suspect about how much value can be added in terms of tax efficiency over and above the extreme tax efficiency of index funds, but I encourage you to read the full Aperio report yourself, at www.fwp.partners/wp-content/uploads/2015/04/What-Would-Yale-Do1.pdf

3. The tax haircut estimates used represent just one of many valid sets of assumptions for a top-bracket taxpayer. Investors may face different tax outcomes due to a particular strategy or tax situation. The goal here isn’t to derive the unattainable: one single “true” set of tax assumptions, but rather to focus on the transparency of measuring and estimating actual tax impact rather than assuming it away as too complicated or irrelevant. Investors and their advisors appropriately focus on the fees and transaction costs that can diminish returns. However, at the same time they can inappropriately shrug off a tax impact that can potentially wipe out almost half of pre-tax returns, a reduction of wealth that can dwarf other factors. The performance reflected in the tables and charts in this report are hypothetical, shown for illustrative purposes only, and not based on actual investments.