Articles about affluent families usually start by referring to “the challenges of wealth.” We’re then reminded of the toxic nature of wealth and the inevitability of “shirtsleeves to shirtsleeves in three generations.” Yet, it may not be wealth itself that’s so challenging to handle. Many families around the world have found effective ways to adjust to, teach about and prepare for wealth across generations. A better perspective is that becoming wealthy is a much more complex adjustment for individuals and families than most people (including advisors) believe. Families, unprepared for this process, can make wrong guesses or follow unhelpful advice, which leads them down a path away from wealth. The issue isn’t truly about coping with too much money. The real challenge is knowing how to adapt to the unique attitudes, behaviors, competencies and perspectives needed to live with wealth successfully.

The Lens of Culture

Becoming wealthy is a major transition in economic culture for most individuals and families. A common misconception is that the ranks of the wealthy in the United States or around the world are filled with a combination of new money and old money, with old money being represented in significant numbers. Multiple surveys over decades actually indicate that around 75 percent to 80 percent of those with wealth were born and raised in lesser economic levels.1 A recent U.S. Trust survey found, for example, that 28 percent of those with self-made wealth over $3 million in net worth grew up either poor or lower middle class, while another 36 percent were raised in a middle class household. Only 14 percent came from upper middle class or wealthy households where the culture of affluence shaped their identity, skills and attitudes.2The ranks of the wealthy consist mainly of people streaming in via high earning professions, business success, windfalls and marriage. Only a few are born there.

My colleague Dennis Jaffe and I realized nearly a decade ago that wealth is, in a sense, a land of immigrants, raised in one culture but now living in another.3 The journey from a modest economic upbringing to having millions in investable net worth is as great as crossing any ocean. We also realized that, for those economic immigrants who become parents, there’s a central dilemma familiar to any ethnic immigrant: How do I raise my children in a culture in which I didn’t grow up? The children and grandchildren of wealth’s newcomers are, in the cultural model of wealth, natives, not immigrants. How can wealth’s immigrants, newly arrived and trying to adjust personally to their new circumstances, know what to do, in the right sequence, overlaid on the normal stresses of parenting children?

Many families fall prey to the following pitfalls:

• Overconfidence that they know what to do with wealth, despite the stereotypes, biases and lack of information society carries about it, including entrenched beliefs about wealth in the minds of wealth creators. Entrepreneurs who are appropriately headstrong in business often carry over their self-confidence to family life, in which a more emotionally intelligent approach works better.

• Guesses about how to live with wealth based on personal beliefs, fears or fascinations with the rich.

• Delayed, inadequate or incorrect methods of parenting with wealth, due to lack of knowledge about what must be done during childhood development when money personality and money skills are being formed.

• Spotty or unhelpful advice from advisors, peers, family and the media, most of whom are largely middle class and unaware of what’s necessary to raise children who are prepared for wealth.

Looking at wealth through a lens of cultural migration and adaptation leads to a new understanding of the stresses involved and the strategies needed for coping. Let’s examine the different stages involved in the lives of individuals and families with wealth.

Immigrants and Natives

The wealth population welcomes a variety of newcomers, some of whom arrive alone and some in groups:

Wealth creators. Those pioneering immigrants who earn and invest high incomes or create businesses that eventually become successful enough to make their owners wealthy. These are members of Generation 1 (G1), whose perseverance, resilience, risk capacity and intense devotion to work inspire others and lead to a sense of well-deserved wealth. Wealth creators may be individuals or members of family businesses—the primary drivers of significant wealth creation,4 with liquidity events often being the point at which the family is transformed from a business enterprise to a wealth enterprise. However, just as charismatic, hard driving, individualistic entrepreneurs don’t always make the best managers of large diversified conglomerates, wealth creators may not be prepared to lead the family across generations in making the necessary adaptations for wealth.

Windfall recipients. This category includes those individuals who come to wealth through circumstances other than their own efforts, such as lottery winnings, litigation settlements or marriage. Spouses raised in middle class life who marry into wealth are perhaps the most common and misunderstood group of immigrants in wealthy families across generations.

In contrast to the multitudes of immigrant newcomers to wealth from various directions, some members of the wealth population are natural-born citizens.

Natives. These are members of Generation 2, Generation 3 and beyond, who’ve been exposed to affluence during their upbringing; this is the culture of their birth. Their personalities, attitudes and identities are strongly influenced by growing up with wealth. An important factor impacting self-esteem, self-sufficiency and identity is that many natives don’t actually control much wealth themselves, due to being beneficiaries of trusts or other entities, such as family limited partnerships. Furthermore, some natives wind up not possessing much wealth at all as adults. They may have been raised in affluent circumstances, but by adulthood, there’s little money left, due to profligate spending, unfortunate setbacks in the family fortune or distribution of a modest fortune to too many family branches.

Individuals raised in middle class circumstances who receive a significant inheritance during adulthood are immigrants, not natives. They may inherit some wealth, but their identity, habits, attitudes and orientation to money are those of a middle class person. In the cultural model of wealth, it’s where you come from, not just where you wind up.

Immigrant/native hybrids. This category includes those inhabitants of the land of wealth who start off as natives but then grow or regrow the wealth through their own efforts. Unlike immigrants from middle class life, they’re familiar with the culture and mores of the wealthy, but they also benefit from the enhanced self-esteem, work ethic and sense of deservedness that wealth creators have.

Acculturation

Becoming wealthy can be stressful in ways unanticipated by those focused only on making the journey. For many people, it’s a disruptive adjustment that challenges their ability to cope. In the short run, a liquidity event or winning the lottery can produce elements of “sudden wealth syndrome,” first identified in the dot-com era, but now a well-characterized adjustment process.5 New relationships must be formed, old relationships may be tested, new options must be evaluated and chosen intelligently and an entire industry of advisors must be navigated with new responsibilities. In estate planning, the choices can be overwhelming in scope and consequence: How do I protect myself and future generations? What type of discretionary provisions are best in trusts: absolute discretion? the ascertainable standard? incentive provisions? Whom should I appoint as trustee? Should I pass on assets equally when that doesn’t seem fair or equitable?

Cross-cultural psychology provides valuable guidance in understanding how individuals make the adjustment to a new culture when leaving behind their heritage culture—what’s termed “acculturation.” We see this phenomenon with ethnic families establishing a new life in a new country. The same patterns are evident in the strategies chosen by those becoming wealthy.

Avoidance. A significant portion of the newly wealthy choose not to make much adjustment to their newfound situation. Perhaps, these individuals believe they’re middle class now and forever and that it would be dangerous to themselves and their families to make any accommodation to their new circumstances. Even with enough resources to be able to relax and enjoy life, they cling to old habits of frugality and modesty. They use financial or legal advice sparingly, and they view even moderately complex estate planning with suspicion. In extreme cases, these clients will ask for your input about their estate but not disclose the level of their assets. They’re likely to hide knowledge of their wealth even from their family until the secret is revealed after their death.

Assimilation. These clients take the opposite tack from avoiders. They’re so happy to be liberated from the constraints of middle class life that they go overboard in enjoying their newfound freedom and status. They wish to assimilate as quickly as possible into their stereotyped image of the rich. Materialism is their new life and attitude. These clients flaunt their status rather than hide it; they may even deny or downplay their middle class roots. Assimilators may be difficult clients in their own right. They may be overspenders who disdain budgeting as a relic of their past economic life. They may keep advisors operating in silos with little coordination, perhaps due to a lack of understanding about the benefits of integrated planning or a desire to keep any one advisor from knowing how much spending is going on. Within the family, assimilators spend little time teaching healthy self-discipline and responsibility to their offspring. Long-term planning may go by the wayside in the daily rush to acquire and spend.

Integration. The best option for adjusting to a new culture is generally to integrate one’s heritage and one’s new circumstances, blending the two thoughtfully.6 Those new to wealth also do best when they take their time adjusting to their new life, allowing themselves to become, in a sense, economically bicultural. Evaluating the many new choices of wealth one step at a time is harder, compared to the all-or-none approaches of avoidance or assimilation. But in the long run, the adjustment is likely to be more balanced and successful. These clients are the easiest to work with. They wish to hold onto the core values and beliefs that helped make them successful. Yet, they’re not afraid to listen to good advice about their current and future circumstances. They’re willing to consider family communication, education of the next generation and other best practices.

Adaptation

Financially successful families must prepare the next generation for the lives they’ll lead with wealth. The family’s middle class roots must be adapted, keeping still-useful elements, dropping outmoded aspects and incorporating new relevant elements. There are two main areas the family must build effectively:

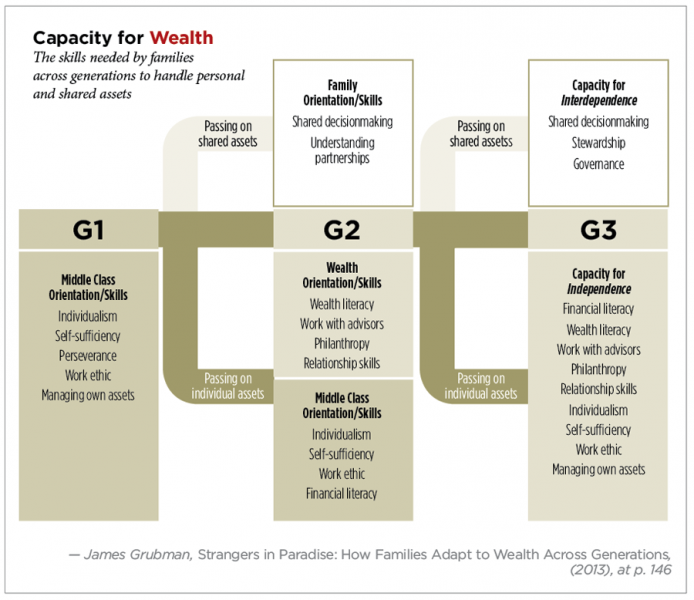

The capacity for independence. This set of competencies7 allows an adult to manage his life responsibly, including such values as work ethic, prudent spending and saving, careful harboring of assets, self-sufficiency and perseverance. They also include additional skills needed in the context of wealth, such as how to work with advisors, implement philanthropy, act responsibly as trust beneficiaries and navigate relationships as a person of wealth. Middle class attitudes and experiences provide only partial guidance in some of these areas. Even if an individual receives income or distributions from trusts or other financial entities, he can still demonstrate a full capacity for independence. Receiving trust income doesn’t automatically translate to emotional dependency, if the individual has been well-prepared to find purpose in life and responsibly handle whatever assets he may receive.

The capacity for interdependence. A hallmark of significant wealth is that assets are passed on in shared fashion, not just individually. There may be shared ownership of real estate, family businesses or partnerships, commingled trusts or other entities. Inheritors must, therefore, develop a second set of skills: an orientation to family, shared decisionmaking, collaboration and stewardship, balancing the needs of multiple present and future owners. These skills aren’t as needed for the individualism of middle class life and modest inheritances involving only personal assets. Families that understand and adapt for interdependence prepare succeeding generations to function together without disintegrating into partisan conflicts and disastrous rifts.

“Capacity for Wealth,” p. 42, shows the changes across generations that families may undergo to develop the dual capacities needed to handle wealth successfully.

The bottom half of the diagram shows the adaptations of those original skills from G1 to keep the best of middle class skills, while adding new competencies in heirs’ personal lives. The upper half of the diagram shows how, if shared assets are a part of the family’s life and resources, an orientation to family and shared decisionmaking is fostered.

The Role of Advisors and Attorneys

Trust and estate attorneys and wealth advisors spend most of their time focused on the mechanics of wealth management and transfer—those processes in “Capacity for Wealth” related to the passing of individual or shared assets across generations. Many estate plans promote creation of shared assets for tax or estate-planning purposes. However, the competencies of inheritors (and sometimes their spouses migrating in from middle class life) really influence the success of wealth transfers. When families don’t know or don’t care about preparing the next generation to be capably independent or interdependent, wealth gets mismanaged across generations, leading to attempts to work around the problem. Estate attorneys face clients wrestling with dilemmas related to how their children or grandchildren are handling wealth. Trusts are created to prevent unskilled heirs from receiving much money. Professional advisory teams are appointed to make decisions influencing multiple family members because the family itself has few skills to manage the complexity of shared decisionmaking. Those families that understand the need to adapt to wealth are much more successful in their wealth management, estate planning and family dynamics.

How You Can Help

Viewing wealth through the lens of cross-cultural adjustment provides a fresh approach to helping clients adapt to being wealthy. Here are some practical recommendations:

For clients who are immigrants to wealth (G1s or in-laws): Help these clients move toward a balance between their old ways and new circumstances. For clients clinging to their old identity, show that you understand their concerns. Educate them about best practices that offset wealth’s risks. Encourage small manageable steps toward approaching the comfort and security of affluence. For clients going overboard enjoying their money, initiate discussions about what their early roots were like when times were tougher. Draw out their values and remind them of the importance of skills, including the lessons they want to teach their children. Clients taking a moderate, thoughtful approach to their situation are probably aware wealth is complicated. Yet, they may be feeling confused or concerned about best practices. Offer these clients resources and articles about family dynamics, wealth management and estate planning for the dilemmas they want to handle as good parents.

Encourage the fundamental factors known to foster a balanced approach to wealth: maintenance and teaching of strong values; family communication; preparation for financial literacy; relationship skills; and preparation of the next generation for the roles and responsibilities of trusts, trustees and beneficiaries.

If wealth or estate planning creates shared assets, discuss how your clients might prepare their children to have skills for shared decisionmaking. It can be hard dissuading family patriarchs from holding the reins of authority too long. Initiating conversations about how other families work to prepare siblings to share decisionmaking can plant the seed that it can be done. Family meetings are very helpful in this regard for creating teachable moments and family communication.

For your clients who are natives to wealth: Take a proactive role in encouraging inheritors to develop skills for independently handling their lives. That doesn’t mean lecturing them—they’ve probably had enough of that. Encourage them to seek out training in basic financial self-management skills and help connect the next generation to resources. Some financial planners specialize in working with inheritors on budgeting, saving and keeping track of income and expenses.

Many beneficiaries know little about their trusts or how the trustee-beneficiary relationship works. You may be cautious about empowering a beneficiary who will then push back on your authority as trustee. But, you may also discover many beneficiaries struggle due to ignorance, misunderstanding or mistrust. Being educated about how trusts work, how you make discretionary decisions and what a beneficiary can do to maintain credibility may fix an unsatisfying relationship.8

Encourage family communication and family meetings. This step is particularly important if there are shared assets creating interdependence. Encourage inheritors to get training in collaboration, negotiation and communication skills, all of which are helpful in group interactions. Even if their parents didn’t prepare them well to work together, clients can still learn skills using peer networks and training in collaboration techniques.

Adapt

There’s no welcome wagon for newcomers to the land of wealth. Failure to understand and cope with the new environment means the family risks getting deported back to middle class life in short order. Fortunately, attorneys and advisors can serve as guides to clients seeking to navigate a sometimes bewildering and difficult landscape. Advisors can educate themselves about best practices for how individuals and families adjust to wealth to truly help their clients. The goal is what any immigrant family must do to thrive: adapt.

Endnotes

1. See James Grubman, Strangers in Paradise: How Families Adapt to Wealth Across Generations (FamilyWealth Consulting: Amazon/CreateSpace 2013), for a full discussion of the demographics of wealth.

2. U.S. Trust (2013), “Insights on Wealth and Worth,” www.ustrust.com/publish/content/application/pdf/GWMOL/UST-Key-Findings-Report-Insights-on-Wealth-and-Worth-2013.pdf.

3. Dennis T. Jaffe and James A. Grubman, “Acquirers’ and Inheritors’ Dilemma: Discovering Life Purpose and Building a Personal Identity in the Presence of Wealth,” Journal of Wealth Management (Fall 2007) at pp. 1-26.

4. For an overview of statistics on family enterprises, see “Global Data Points” in the “Research and Resources” section of the Family Firm Institute website, www.ffi.org.

5. Susan Bradley, Sudden Money: Managing a Financial Windfall, Wiley and Sons (2000); see also Stephen Goldbart and Joan Difuria, The Money, Meaning & Choices Institute, www.mmcinstitute.com.

6. David L. Sam, “Acculturation: Conceptual background and core components,” D.L. Sam and J.W. Berry (eds), The Cambridge Handbook of Acculturation Psychology (Cambridge University Press 2006) at pp. 11-26.

7. I use “capacity” here in the legal sense as a set of component skills and knowledge, analogous to sets of legal competencies that constitute testamentary capacity or fiduciary capacity.

8. Good resources on creating positive trustee-beneficiary relationships can be found through the website and writings of attorney Hartley Goldstone and family business consultant Kathy Wiseman at www.navigatingthetrustscape.com.