By Michelle Borré

The election of Donald Trump has brought about sweeping changes to some long-held market views. The low for long interest rate regime that was firmly in place before the election has notably been dislodged in the weeks since the election, as the yield on the 10-year U.S. Treasury bond increased over 50 basis points. What has driven this change and can it persist? If it does, how can investors position themselves in this new environment?

The view of my team is that the change in the bond market has been driven by a few key factors. This scenario was set in motion by some of President-Elect Trump’s stated policy goals, including:

- Fiscal stimulus in the form of tax cuts for corporations and individuals, as well as incentives to bring offshore cash back on shore.

- Fiscal stimulus in the form of increased infrastructure spending.

These measures would be constructive for growth in the United States, and that could enable a normalization of interest rate policy, which would bring an upward pressure on rates. In addition, this stimulus would come at a time when the United States is closer to full employment, a circumstance that could potentially lead to inflation and a further need for higher rates.

While on the campaign trail, President-Elect Trump was very critical of the policies of U.S. Federal Reserve Chair Janet Yellen to keep interest rates low. He is likely to appoint a more hawkish head of the Federal Reserve (the Fed) when Yellen’s term expires early in 2018. He also could fill the two vacancies on the Fed’s seven member board of governors with sympathetic appointees. These new appointees could bring an end to the dovish approach to interest rates that the Federal Reserve has taken for some time.

These developments, along with President-Elect Trump’s stated goals for trade policy, could create a new climate for trade:

- There could potentially be tariffs or taxes on imported goods. Both would increase the cost of goods being purchased from abroad and bring inflationary pressures. These changes could also spark growth in the capacity of U.S. companies to manufacture goods and provide services, as they respond to the surge in demand for their relatively lower-priced products and services.

- These trade policies could also spark retaliation abroad if other countries impose tariffs on U.S. exports―measures that could dampen global trade. In the long run, these new trade policies could hurt global growth and cause friction in the global economy.

One of Trump’s stated goals in renegotiating trade deals is to increase manufacturing capacity in the United States and displace capacity that is currently located abroad. If that effort succeeds, it will likely lead to a transitional period when the U.S. is undersupplied as the capacity comes on line here, and that circumstance would bring upward pressure on domestic pricing. Outside of the United States, the capacity that is currently filling U.S. demand is not likely to be shuttered quickly. That could lead to excess supply outside of the United States, which could put downward pressure on the prices of the goods and services produced in other countries.

This combination of upward pressure on pricing in the United States and downward pressure on pricing outside the United States could keep U.S. interest rates higher than international rates―and that would put upward pressure on the dollar. If the end of easy monetary policy in the United States is followed by, as an example, a decision by the European Central Bank to taper bond purchases, that could be the start of interest rates increasing in other parts of the world as well.

What Are the Implications for Investors?

We have been concerned for some time that eventually the 35-year bull market in interest rates would come to an end and that rates would begin to reverse direction. That scenario would cause fixed income assets with higher duration―that is, greater interest rate sensitivity―to underperform, and certain assets, like investment-grade debt that had served as strong portfolio diversifiers, to be less effective in doing so.

As evidence of that, consider what has happened since the U.S. election:

From November 8 through the date of this blog on December 7, 2016, the Barclays Aggregate Bond Index was down over 2.5%. That is a quick move in just a few weeks. This occurred alongside an equity market rally. The real problem for investors would come in a scenario in which both equities and U.S. Treasuries sold off simultaneously, as that would leave their portfolios without anything to cushion the markets’ fall.

To determine if we are at risk of such a scenario playing out, we looked at the correlation between stocks and bonds going back several decades.

We see from the historical data that for the last quarter of the past century, stock and bond returns were positively correlated. That means they moved together. When returns on stocks went down, returns on bonds did as well. Think of what happened in the late 1970s, when the pressures of very high inflation negatively impacted both stocks and bonds.

Since 2000, however, returns on stocks and bonds have been negatively correlated. When stocks went down, bonds went up and vice versa. This means that bonds have been a great diversifier for stocks for the past 15 years.

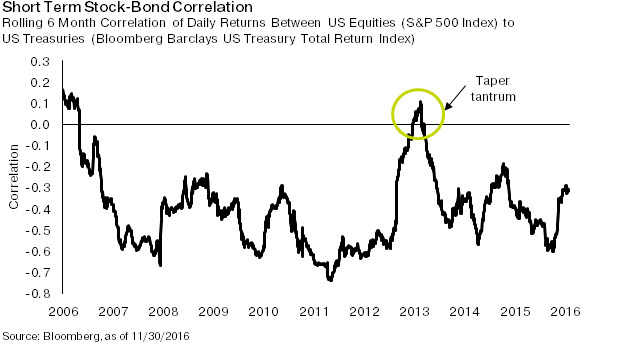

To further examine these correlations, we focused on the past decade.

Past performance is no guarantee of future results.

During the past 10 years, stocks and bonds have had mostly negative correlations. That would mean they provided good diversification with each other―with some notable exceptions. One occurred during the so-called Taper Tantrum, when the market panicked at the expectation that the U.S. Federal Reserve would begin to curtail its Quantitative Easing program. During that time, the correlation quickly changed from negative to positive, and stock and bond returns went down together. For a more in-depth look at this research, please refer to our white paper, Alternative Strategies Now and Going Forward.

The real risk for today’s portfolios would be a return to the prior regime of positive correlations between stock and bond returns. That scenario would make the traditionally great diversification benefits that traditional fixed income assets provide no longer effective. In that case, new means of diversifying would be needed. We are not there yet, but we view this possibility as a significant risk to portfolios. If interest rates keep rising, they could derail the equity market rally.

How to Position Portfolios for Rising Rates

We don’t think interest rates will rise in a straight line. There are bound to be ups and downs, but the unleashing of Trumponomics may well bring in a new era with higher rates and a stronger U.S. dollar. Low volatility funds that have less duration risk could play a valuable role in investors’ portfolios in this new regime.

Using the Barclays Aggregate Bond Index to diversify has been a terrific strategy, but at some point the benefits this approach provided could be in the rearview mirror. This broad-based U.S. bond index has had healthy returns with low volatility for many decades, as the yield on the 10-year U.S. Treasury bond went down from almost 16% to below 2%. That is not a repeatable scenario, and in a rising-rate environment, the returns on this index could quickly turn negative.

For investors, finding low-volatility alternative strategies that can play the important role of stabilizing portfolio returns could help them position their portfolios for the next five years.

Michelle Borré is a portfolio manager at Oppenheimer Funds.

This article originally appeared on the OppenheimerFunds website.