When two of the world’s most respected bond gurus independently identify the same potential shocks coming to the fixed income market, it’s worth taking notice – if not action.

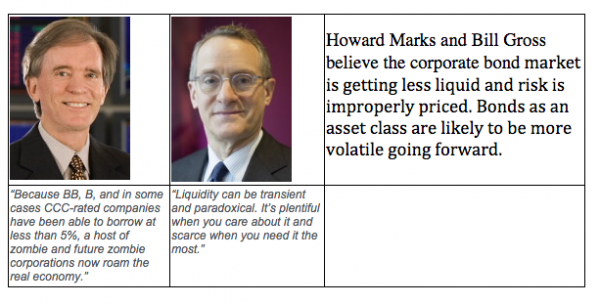

Bill Gross of Janus Funds and the Howard Marks of Oaktree Capital Management are hall-of-famers in the investment management world. Both have gone public in recent weeks predicting that the corporate bond markets are in for a rough ride due to conditions created by the Federal Reserve’s zero interest rate policy.

We agree with their short-term prediction. We also believe that the implications for long-term portfolio allocation are profound for family offices, RIAs, and institutional investors.

What Happened

Why have two industry titans turned their backs on the markets that made them rich and famous? For three good reasons that have to do with structural changes in the U.S. corporate bond market: reduced liquidity, low yields and mispriced risk across credit quality

First, the current corporate bond market is not as stable and liquid as it once was. The bond market today is just as rambunctious and unpredictable as the equity market. Dodd-Frank regulation after the 2007 financial crisis forced banks to step back from market-making operations and proprietary trading. Hedge funds, retail mutual funds and bond ETFs filled the void. The arbiters of the new bond market have liquidity mandates that force them to sell to meet daily or monthly redemptions from their investors. They can’t simply ride out the inevitable market fluctuations and tend to accentuate moves as price followers who sell low and buy high. Despite this shift, which otherwise might have stifled the growth of the bond market, corporate bond issuances over the past years have clocked a record pace fueled by low rates.

Second, corporate bonds even in a slowly rising rate environment are unlikely to deliver returns at historical levels of performance and will probably remain correlated with equities as they have been since 2007. The long-held adage of allocating bonds as a percentage of your portfolio according to your age (i.e., if you’re 75, you should be 75% in bonds) no longer makes sense in a market where bond yields are below 5%.

Third, pricing and risk across bond quality have been distorted by the massive universal demand for yield. The spread (or the relative measure of risk) between Treasuries and high-yield bonds has narrowed substantially compared to 20 years ago. There’s no reason to believe that high-yield bonds carry lower risk today than they did previously, but you don’t get paid a premium for that risk any longer. Yet hedge fund and individual investors continue to buy high yield mutual funds and ETFs for incremental yield and liquidity.

Rethinking The Basics: Private Debt – A Fixed-Income Alternative

If you accept our premise that corporate bonds are vulnerable to major liquidity constraints, and don’t generate sufficient income for the accompanying risk and volatility, you undermine the main premise behind most portfolios.

Portfolio theory seeks to reduce risk and maximize return through diversification across asset classes. By investing in equities, fixed-income and alternatives, investors in a well-constructed portfolio theoretically generate non-correlated returns, meaning that when stocks are tanking fixed income should be less affected or not affected at all.

The key question, then, is how investors should proceed.

We don’t think investors should abandon the fixed-income market. Instead, they need to think out of the traditional portfolio box by shifting some portion of public debt allocation into private debt. This change involves trading off the possibility of short-term liquidity for lower risk and higher returns.

One attractive opportunity is investing in the debt of private, lower middle market companies with strong assets, proven cash flows and well-defined growth plans.

Investments in this asset class can deliver double-digit yield from debt service, plus substantial upside from the equity positions we take in our companies. We believe this type of alternative fixed-income product offers a significant advantage in this market – current income, principal protection and capital appreciation.

In other words, returns comparable to private equity with limited principal risk, significant current income and low volatility.

The Bottom Line

Bill Gross and Howard Marks have rung the alarm bell. If your portfolio relies heavily on bonds for liquidity and steady income, you should understand that the zero rate environment of the past few years has rendered your allocation methodology obsolete.

Richard de Silva is Managing Partner of Lateral Investment Management in San Mateo, California.