This upcoming weekend, Saturday, May 3, 2014, marks the one-year anniversary of the start of the great bond market sell-off of 2013. Starting May 3, bond prices declined steadily through late June 2013, with weakness persisting through much of the summer. The sharp pullback was one of the worst on record and contributed to the broad Barclays Aggregate Bond Index posting its weakest calendar year performance since 1994. In an eerie one year parallel, Apple, a rare corporate bond issuer, issued new bonds on April 30, 2013, just prior to the sell-off, and locked in a low interest rate. This week, Apple announced another bond issue to take advantage of low yields in an opportunistic issuance to benefit stockholders. Is the bond market near another market top?

Where Are We Now?

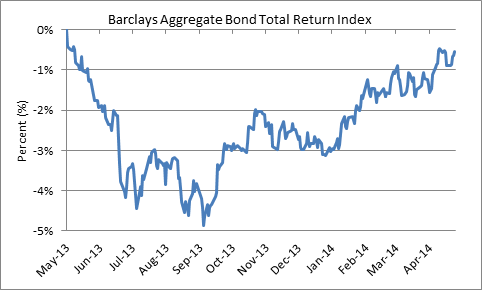

First, let’s take a look at where the bond market is now. The broad bond market has almost fully recouped the damage done from the 2013 sell-off, assuming reinvestment of interest income. As of April 28, 2014, the Barclays Aggregate Bond Index is down just 0.5% from the May 2, 2013 peak and close to recouping all of the loss from the sell-off [Figure 1]. Had a bond investor been unfortunate enough to have bought just prior to the sell-off, they would now be approaching breakeven if steadily reinvesting interest payments.

Figure 1: Bouncing Back from the Sell-off.

Source: Barclays, LPL Financial Research 4/28/14.

Two main drivers are responsible for the bond recovery:

- A strong start to 2014. As we have discussed in prior commentaries, the bond market has enjoyed broad-based strength in 2014 with higher prices translating to lower yields. Weaker-than-expected economic reports, due in large part to adverse weather impacts, China and emerging market uncertainty, and geopolitical tensions in Ukraine have aided bonds.

- Good old interest income. Average high-quality bond prices have not returned to their late April/early May 2013 highs but the passage of time and reinvestment of interest income has helped offset price declines associated with the rise in interest rates last year. Over longer periods of time, interest income will be the primary driver of bond returns. Interest income has boosted total returns and helped heal the wounds of 2013.

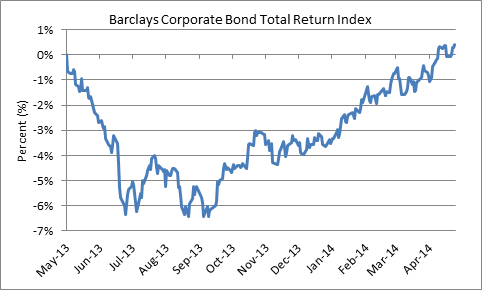

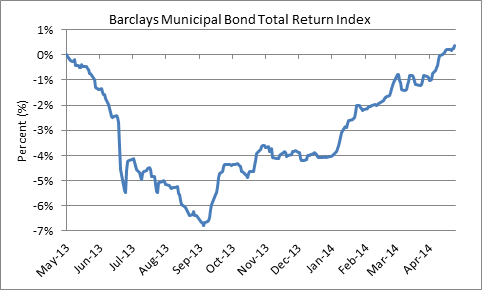

Several sectors are positive over the past 12 months. Both investment-grade corporate bonds and high-quality municipal bonds have more than recouped 2013 declines [Figure 1]. The more attractive valuations of corporate bonds and municipal bonds have helped both sectors snap back more strongly from the bond market pullback.

Source: Barclays, LPL Financial Research 4/28/14.

Source: Barclays, LPL Financial Research 4/28/14.

High-yield bonds, which have historically exhibited very little interest rate sensitivity, are notably ahead of late April/early May 2013 levels. High-yield bonds endured a more limited pullback that was exacerbated by an illiquid trading environment and the sector has led bond market performance over the past 12-months with a 6.7% total return.

On the negative side, some areas of the bond market have not fully recouped losses from the 2013 sell-off. US Treasuries are still 1.7% off their highs and both high-yield municipal bonds and long-term bonds are down roughly 2% from 2013 peaks (according to Barclays Index data). Treasuries possessed some of the most expensive valuations prior to last year’s sell-off, and remain expensive in our view, while long-term bonds typically bear the brunt of sharp changes in interest rates with 2013 no exception. Long-term bonds are among the leaders of 2014 bond market performance so far this year as their interest rate sensitivity has been a positive amid falling bond yields. High-yield municipal bonds have similarly benefited from the fall in long-term yields but also benefited from improving credit quality in the municipal bond market.

Repeat Unlikely

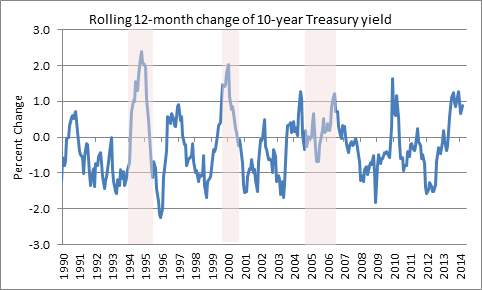

History shows that over the past 25 years spikes in interest rates, as measured by the 10-year Treasury yield, are very rare. Figure 2 illustrates the change in the 10-year Treasury yield over rolling 12-month time periods. A back-to-back increase in the 10-year Treasury yield of 1% or more has never happened. So a repeat of the 2013 sell-off here in 2014 is very unlikely. Yield increases are often the result of Federal Reserve (Fed) interest rate hikes. In 1996 and in 2013, the threat of Fed rate hikes, or a less market-friendly Fed, caused yields to move higher. Expensive valuations played a role in 2013 as they did in 2009.

Figure 4: A Back-to-Back Spike in Bond Yields Has Never Happened

Source: Bloomberg, Federal Reserve, LPL Financial 4/28/14. Please denote shaded areas represent periods of Fed rate hikes.

The 2014 rebound in bond markets is welcome for many investors but has created new challenges. The rebound and corresponding higher valuations and lower yields increases the difficulty of finding attractive investments. Continued strength in the high-yield bond market and notable rebounds across several bond market sectors, such as investment-grade corporate bonds, municipal bonds, and preferred securities, translates into less value for bond investors. The average yield of high-yield bonds is hovering at an all-time record low of 5% and the average yield of investment-grade corporate bonds is just 0.4% above May 2013 lows. Intermediate to long-term high-quality municipal bond yields are 0.5% to 0.7% above year-ago lows and approximately 50% below 2013 peaks.

Uncertainty over the economy, and the degree to which weather played a role in sluggish 1Q14 economic growth, may keep yields low but the lack of value urges caution. While we do not expect a repeat of 2013, a similar gradual rise in yields resembling the 2004–06 episode may unfold as the bond market gradually unwinds expensive valuations and prepares for Fed rate hikes.

Anthony Valeri is an Investment Strategist for LPL Financial.