By Brian Chappatta

(Bloomberg Opinion) -- Leave it to catastrophe bonds to be among the most well-functioning debt markets out there.

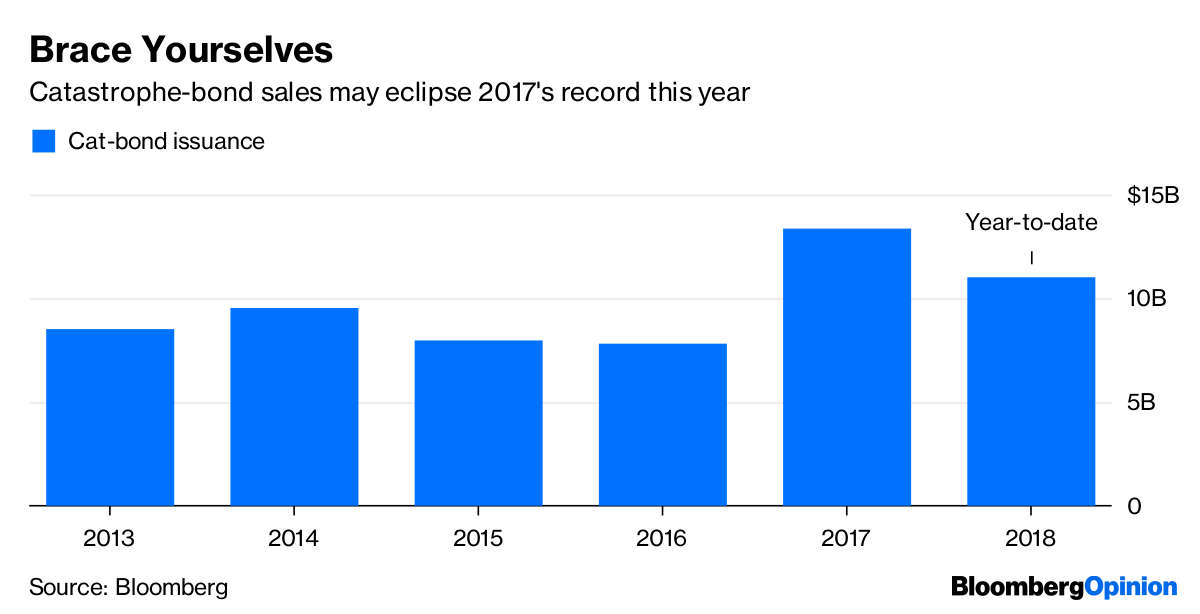

Issuance of “cat bonds” has climbed to more than $11 billion this year, about the same as this time in 2017, when sales hit a record, according to data compiled by Bloomberg. The debt helps protect insurers from potentially massive costs tied to damage from hurricanes, floods or other natural disasters. That’s important given that Hurricane Florence has strengthened into a Category 4 storm barreling toward the U.S. East Coast, with top winds reaching 130 miles (209 kilometers) an hour.

Now, you might think cat-bond buyers would be panicking. After all, Florence is shaping up to be of similar strength as Hurricane Hugo in 1989, which came ashore near Charleston, South Carolina, and caused about $14.1 billion in damage when adjusted for inflation, making it the 13th costliest U.S. storm. The entire purpose of cat bonds is to set aside proceeds to help pay future disaster claims, if needed. That’s money that investors won’t get back.\

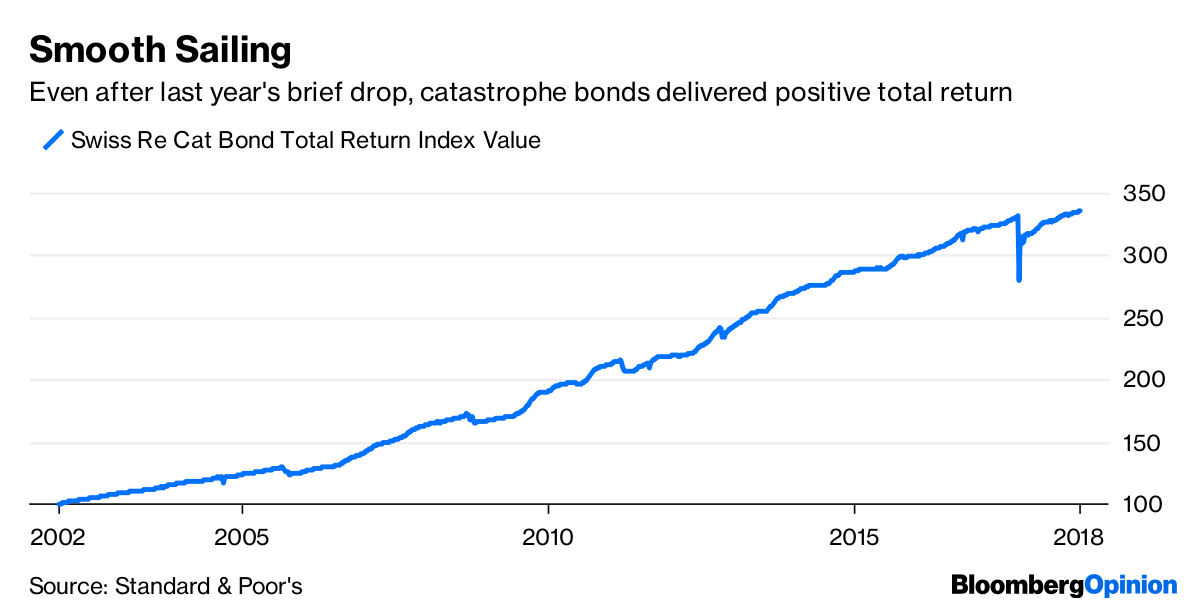

But that’s not what’s happening in this sliver of the financial markets. In fact, the bonds have gained 4.3 percent this year as measured by the Swiss Re Cat Bond Total Return Index. They’re up a remarkable 20 percent from 12 months ago, bouncing back from the index’s steepest loss on record in the wake of a devastating month for Atlantic hurricanes. In fact, as Bloomberg News’s Michael Regan pointed out, cat bonds haven’t posted a negative annual return since the index began in 2003.

So issuers are well protected and investors are well compensated. What’s the catch?

Certainly, a huge storm that activates so-called trigger events on a wide swath of securities would devastate investors. And their buffer is shrinking as the market matures — the average coupon on a cat bond issued this year is a mere 5 percent, Bloomberg data show. The average expected loss, according to a report from Brendan Grady at KeyBanc Capital Markets, is 2.71 percent. Combined, the spread is the narrowest ever.

But for cat-bond investors, it’s not as simple a calculation as “storm = losses” and “no disaster = profit.” Grady explains it like this:

“Hurricane Harvey hit Texas and was the second costliest storm in U.S. history — however — there were no losses for catastrophe bonds other than the initial mark-to-market impact of the storm. … Part of the reason that investors are willing to take on these risks is that the bonds insure for very specific events. A bond may only cover wind damage for a Carolina Hurricane, but not flooding.”

This specificity works to the advantage of all parties. For bond buyers, it reduces the likelihood that their money will be diverted away to cover claims. For insurers, it’s not as if cat bonds are the only method of insulating themselves from losses. Rather, the debt is just another way to hedge against a once-in-a-generation type of disaster.

Still, the market’s success has even surprised its experts. Consider Michael Millette, former head of structured finance at Goldman Sachs Group Inc., who helped the bank develop a market for cat bonds in the 1990s. He said in a Bloomberg Businessweek article in January that the market “exceeded my expectations as far as resiliency” in 2017. After a rash of hurricanes, “losses were consistent with the losses that investors felt should have occurred.”

The other upside for buyers is that these bonds have little to do with the overall economy and business cycle. That makes them a strong candidate for diversification among the typical “sophisticated investor” crowd — pensions, endowments, family offices and hedge funds.

As cat-bond sales this year have shown, supply has kept up with demand. And, according to a report from Kroll Bond Rating Agency, “many observers agree this will continue as it is expected there will be a greater need for more insurance due to climate change.”

According to Kroll, 2017 generated the most disaster damage in the history of the insurance-linked securities market. And yet it’s as strong as ever. Ironically, Kroll says the decline in credit ratings on these transactions — down to 27 percent of volume since 2013 from 75 percent previously — signals that investors are comfortable with the risks embedded in cat bonds. They simply don’t need to rely on the agencies’ input anymore after they have seen how this debt performs in bad times.

For the superstitious, this is the time to knock on wood. Insurers and investors alike would prefer no disasters at all, particularly one like Florence that could be in the same mold as Hugo, which killed 49 people in the U.S. and across the Caribbean. Total return seems inconsequential when people’s homes are destroyed.

But the cat-bond market is specifically designed for if and when disaster strikes. And at least for now, it seems built to last.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

To contact the author of this story: Brian Chappatta at [email protected]

For more columns from Bloomberg View, visit bloomberg.com/view