By Scott Dorf

(Bloomberg Prophets) --The bond bears had a good run. The benchmark Bloomberg Barclays U.S. Treasury index declined as much 3.67 percent between early September and late September. Lately, though, they seem to have lost some of their resolve as yields on intermediate-term Treasuries fell back from their highest levels since 2010. If anything, they should be more bearish.

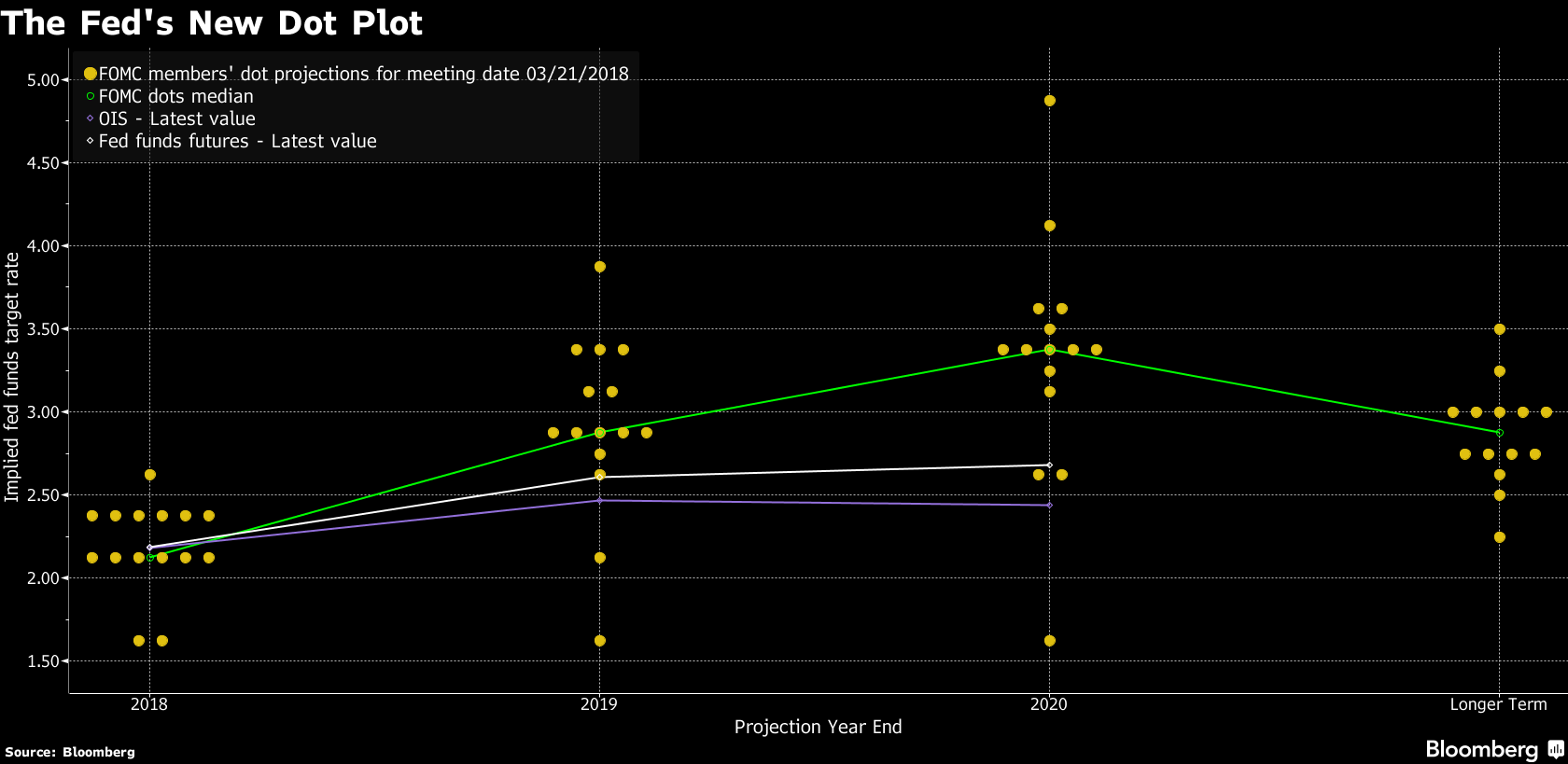

The Federal Reserve meeting last week, where the central bank raised interest rates for the fifth time in the last 15 months and signaled two more are on the way by the end of the year, should have breathed new life into the bears. Instead, bonds rallied, in part, as Chairman Jerome Powell downplayed the risks of faster inflation and stocks tumbled. But, a close look at the Fed’s rate forecast reveals that the difference between its call for a total of three increases this year and four amounted to one estimate on the central bank’s “dot plot.”

Looking past 2018, the Fed’s outlook is even more bearish for the bond market. The central bank boosted by one the number of rate hikes it expects in each of 2019 and 2020. At the same time, its unemployment rate projections were lowered to an eye-popping 3.6 percent and its inflation estimate rose above its 2 percent target level, to 2.1 percent. Although the shift on inflation was small, it’s important because the Fed finally acknowledged that inflation is likely to overshoot its target, and that former Chair Janet Yellen’s “run hot” approach to policy will continue under Powell.

Yes, first-quarter gross domestic product projections have fallen after weak readings on retail sales and other key data, but the Fed is confident that any slowdown will be temporary, stating simply that “the economic outlook has strengthened recently.” With that, the Fed is acknowledging the strength of the prior three quarters, as well as the likely benefits from the recently enacted tax reform and massive deficit spending. As for inflation, it’s likely to start rising well above the Fed’s 2 percent target as soon as next month when the cell-phone price cuts of early last year drop out of the annualized CPI data. Look for a CPI rate that is up almost 2.4 percent from a year earlier.

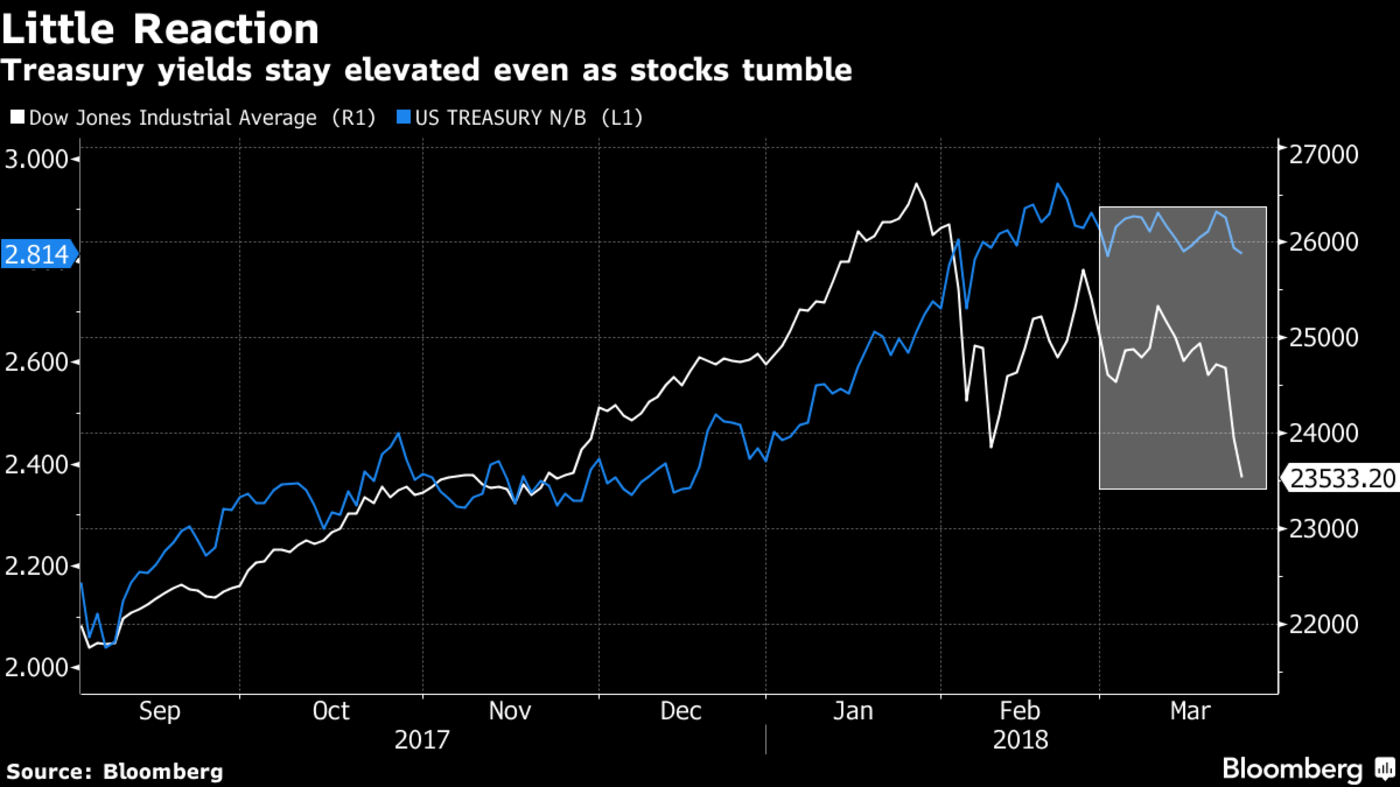

It’s true that Treasuries rallied last week, as yield-starved foreign investors poured into the market following the Fed’s rate decision and equity markets tumbled on the Trump administration’s tariffs targeting Chinese exports. But the most telling part of the action was the 10-year Treasury yields only managed to drop a measly three basis points on the week as the Dow Jones Industrial Average tumbled more than 1,400 points in its worst decline in more than two years. But this week, those lower bond yields will be tested by another round of the debt sales by the government. The Treasury is offering $109 billion of two-, five- and seven-year notes as well as the usual bill offerings.

The last refunding two weeks ago, which consisted of three, 10- and 30-year securities, surprised many by drawing strong demand. That was before the tariff tantrum in markets. When asked in an interview with Bloomberg Television on Friday whether China plans to scale back its purchases of Treasuries in response to tariffs imposed by the Trump administration, China’s ambassador to the U.S., Cui Tiankai, wouldn’t rule out the possibility. “We are looking at all options,” he said.

That’s a disturbing thought, given that the Treasury plans to more than double its borrowing this year to some $1 trillion to pay for the expanding budget deficit. Political uncertainty and threats to risk assets come and go, but the deficit explosion will always need to be funded. A look at the January meltdown in Treasuries shows what’s at stake. Yields on 10-year notes shot up almost 40 basis points that month, a huge move for a market where volatility has steadily diminished for almost a decade, and the Bloomberg Barclays U.S. Treasury index lost 1.36 percent in one of its biggest declines in recent years.

So, with the Fed on the march toward six quarter percentage-point rate hikes by the end of next year, the federal budget deficit headed to well over $1 trillion, and the government ramping up its borrowing, one has to wonder how long 10-year Treasury yields can hover around the 2.80 percent to 2.85 percent level.

Scott Dorf is a managing director at Amherst Pierpont Securities. He has been selling and trading U.S. Treasuries for more than 30 years.

To contact the author of this story: Scott Dorf at [email protected] To contact the editor responsible for this story: Robert Burgess at [email protected]

For more columns from Bloomberg View, visit Bloomberg View