(Bloomberg) -- For the titans of private credit, it’s a once-in-a-generation opportunity.

Wall Street’s vaunted leveraged finance desks are reeling. Billions of dollars in losses on mistimed loans have forced them to dramatically scale back lending, leaving the private equity firms that rely on them to help fund acquisitions in a bind.

Enter the likes of Apollo Global Management Inc., Blackstone Inc., HPS Investment Partners and Ares Management Corp. Direct lenders, already among the largest players in leveraged buyout financing, see an extraordinary opening to grab market share — and hang onto it for the long haul.

Their strategy, in part, involves staking a claim to increasingly larger loans, deals once exclusively the domain of banks due to their sheer size. The four are among the shops offering $5.5 billion to fund Carlyle Group Inc.’s purchase of a 50% stake in Cotiviti Inc., according to people familiar with the matter, in what would be the biggest ever transaction of its kind. Private credit firms are also working on a $5 billion financing for another LBO, said the people, asking not to be named because they’re not authorized to speak publicly.

The bold foray speaks to the power shift already underway in the lucrative business of providing debt to the buyout industry. Should the strategy succeed, Wall Street risks losing out on even more fee-rich financings that until recently generated a third of their investment-banking revenue. What’s worse, the more reliant private equity becomes on direct lenders, the harder it will be for banks to win back mandates, market watchers say.

“Multibillion-dollar M&A deals can now credibly consider private credit as an option,” Mike Patterson, a governing partner at HPS, said speaking about the market broadly. “Even as capital markets re-open, we’d expect private credit to keep 10% to 25% of those deals that would have traditionally gone to public markets.”

Representatives for Apollo, Blackstone, HPS and Ares declined to comment on their involvement in the Cotiviti loan.

Of course, there’s no guarantee that in seizing market share from Wall Street, private credit firms won’t make the same mistakes banks did a year ago mispricing risk. Just look at the surge in rates over the past month alone.

Still, direct lenders say that with leveraged finance desks still largely on the sidelines, they’ve been able to be more selective on deals. They’re commanding higher yields and better safeguards, firms noted, helping protect them should investor sentiment sour.

This year “is going to be a really important year for direct lending — we recognize that the higher rate environment and weaker economy will really test the quality of the underwriting,” said Craig Packer, co-founder of Blue Owl Capital Inc. “We are baking into our assumption a potential recession by the middle of the year.”

‘Here to Stay’

Last year’s sharp deterioration in credit conditions as the Federal Reserve boosted interest rates to tame inflation forced banks to self-fund billions of dollar of financing commitments they’d planned to offload to money managers. Large portions of the debt ultimately had to be written off amid a slump in high-yield bond and leveraged loan prices.

Private credit firms weren’t immune to the pain either, with many shying away from the largest, riskiest deals in the second half.

Still, they were able to withstand the rout better than their Wall Street rivals, and buoyed by resurgent institutional allocations, are once again looking to push the envelope when it comes to jumbo financings.

“People are seeing more institutional capital come to market,” said Dwight Scott, head of credit at Blackstone. “The potential for two large deals happening indicates that private credit is here to stay.”

Losing out on Cotiviti would be particularly painful for Wall Street given the company has been a reliable source of fees in the past.

When Veritas Capital bought the Utah-based firm in 2018, banks including JPMorgan Chase & Co., Deutsche Bank AG and Macquarie Group Ltd. helped arrange a $3.7 billion leveraged loan and $1.1 billion high-yield bond offering. The debt has performed well over the years, and investors say similar financing would be an easy sell for banks, noting that it’s a sponsor-to-sponsor deal that needs little wait time to close.

Yet Carlyle and Veritas have so far preferred to pursue the private funding route, Bloomberg previously reported.

Representatives for JPMorgan, Deutsche Bank and Macquarie declined to comment.

Read more:

- Apollo, HPS Pile Into Record $5.5 Billion Private Credit Deal

- Carlyle Said in Talks to Buy Cotiviti for Close to $15 Billion

- Wall Street’s Lucrative Leveraged-Debt Machine Is Breaking Down

- Sixth Street Leads $2.6 Billion Loan for Thoma Bravo Coupa Deal

Of course, Wall Street isn’t going to lay down without a fight.

Some banks have been actively pitching buyout firms on syndicated financing options after some initial success last month chipping away at the mountain of bonds and loans stuck on their balance sheets.

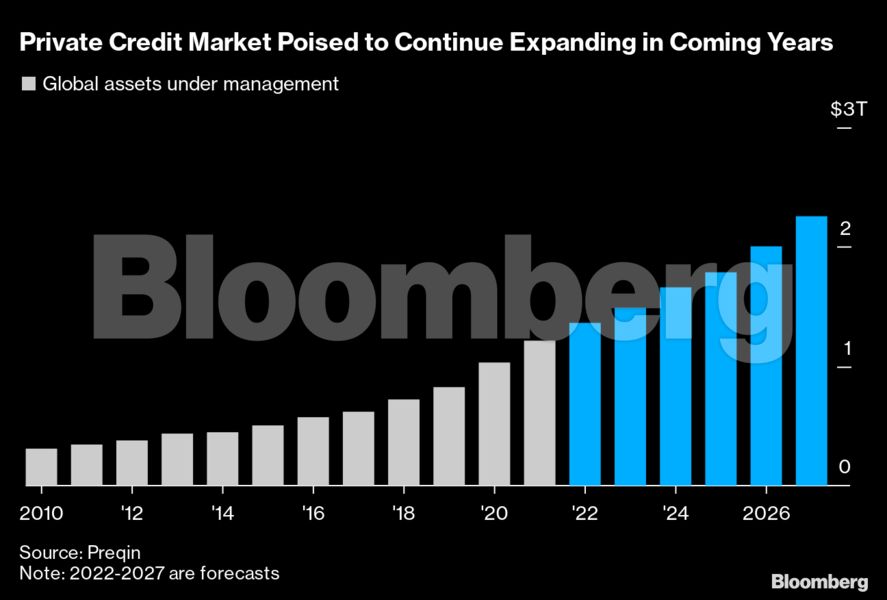

If you include the high-yield and leverage loan markets, all of leveraged finance is $3 trillion, while the entirety of private credit is $1.4 trillion, Mark Jenkins, head of global credit at Carlyle, points out.

“There’s no way we can fill the void today,” he said.

But wary of a repeat of last year, the banks have sought massive cushions to prevent getting stuck with losses should markets turn, industry insiders say. The flip side, of course, means leaving private equity with the exposure, a scenario that for many buyout firms is a non-starter.

“It’s a good time for private credit because banks aren’t providing compelling underwriting options at competitive terms,” said Kipp deVeer, Ares’ head of credit.

‘Brutal Reminder’

Even if Wall Street’s leveraged-debt machine is able to bounce back in relatively short order, direct lenders say that pent up demand for financing should ensure there’s plenty of business out there for those with the capacity to lend.

“M&A is picking up and there’s roughly $250 billion of refinancings coming over the next 12 months, so we expect to see plenty of demand across both private and public markets,” said Robert Givone, a partner at Apollo.

Private credit providers in Europe are also expecting to snag larger deals once the buyout market emerges from a sluggish start to the year.

“Every private equity deal will run a dual-track process, between private credit funds and banks, meaning that anything that gets done will be shown to people like us,” said Peter Lockhead, co-head of direct lending at Intermediate Capital Group Plc.

Many in the industry say private credit’s ability to provide financing even amid periods of heightened volatility will prompt more borrowers to migrate to direct lenders over the longer-term.

Last year “was a brutal reminder of the risk that banks take when they underwrite leveraged finance deals and wind up holding it on their balance sheets,” Blue Owl’s Packer said. “At some point the banks will come back, though we believe direct lending will continue taking market share.”

Here’s what else is happening in credit:

- In the US high-grade market, 16 companies, including Colgate-Palmolive Co. and Arrow Electronics Inc., are looking to sell bonds. Dealers are expecting around $40 billion of sales this week

- American Car Center told employees the business was closing its doors, a day after it pulled a $222 million bond sale from the market, according to people familiar with the matter

- Credit rating downgrades are exceeding upgrades so far this year

- Teva Pharmaceutical Industries Ltd., one of the largest generic-drugmakers in the world, kicked of a cross-currency bond sale on Monday to help buy back up to $2.25 billion bonds

- Junk bonds have dropped in value in February along with other fixed-income securities, though the high yield new issue market showed some life on Monday with Triumph Group Inc. and Teva unveiling deals

- Investors are shunning Atento SA’s bonds as an overdue payment on the notes does little to instill confidence the Brazilian call center operator can weather the worsening credit conditions on its home turf.

--With assistance from Silas Brown.

© 2023 Bloomberg L.P.