(Bloomberg Opinion)—If market participants are wringing their hands over the potential fallout from the collapse of Silicon Valley Bank, just wait until they look at the banking industry’s exposure to the rapidly weakening commercial real estate sector.

It seems as if every few days brings news of some big property going into default. Within the past few weeks, an office landlord controlled by Pacific Investment Management Co. defaulted on about $1.7 billion of mortgage notes on seven buildings in places such as San Francisco, Boston and New York. Before that, a Brookfield Corp. business defaulted on loans tied to two Los Angeles office towers. A $1.2 billion mortgage on a San Francisco complex co-owned by former President Donald Trump and Vornado Realty Trust has showed up on a watchlist of loans that may be in jeopardy.

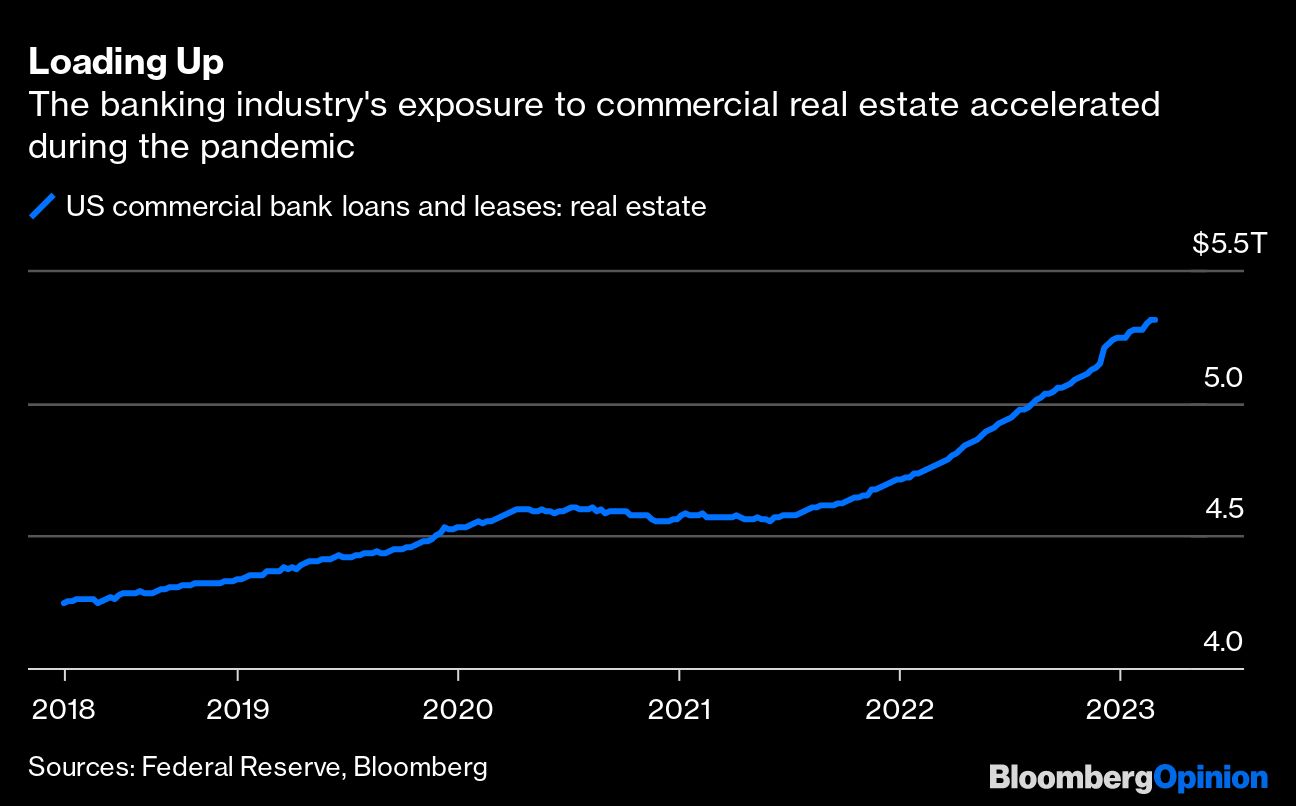

If the saga at Silicon Valley Bank hastens the arrival of the next recession, expect to see many more properties go into default sooner rather than later. This is bad news for lenders because they have ramped up their financing of real estate. Since mid-2021, total real estate loans and leases on their books have soared by more than $725 billion, or 16%, to a record $5.31 trillion, according to the Federal Reserve.

Last year’s 11.2% increase was equal to the previous four years combined and the most since — gulp — 2006. Not only that, but commercial real estate loans make up close to 24% of all bank loans, the most since the financial crisis, according to BNY Mellon strategist John Velis. One reason banks have so much exposure is that it has become tougher to offload the risk to investors. The commercial mortgage-backed securities market went from $240 billion in annual issuance in 2007 to just $60 billion in 2020, a 75% decline, Velis notes. Here’s what Velis wrote in a research note before Silicon Valley Bank blew up:

“In textbook monetary policy, rate hikes are intended to tighten financial and credit conditions, leading to lower economic activity. However, certain parts of the economy, in particular where significant leverage is present, can come under duress, often leading to financial-sector strains. We are keeping an eye on commercial real estate (CRE) loans as one area of the financial system where we see vulnerabilities present.”

Commercial real estate is a risk that Bleakley Financial Group LLC Chief Investment Officer Peter Boockvar has been warning his clients about for months. In one research note late last year, Boockvar walked his readers through the numbers. In his example, an investor that paid $50 million for an apartment property in 2020 and took out a three-year loan for 70% of the property’s value. Assuming the property was bought at a 5% capitalization rate, it would deliver some $2.5 million in gross annual rent. That’s more than enough to cover the $960,000 or so in annual interest on a sub-3% loan and cover other expenses such as insurance, taxes, maintenance and property management.

But nobody thought interest rates would rise as fast as they have, and this investor now faces having to refinance this year at rates well above 7%. That would push annual interest costs to some $2.63 million, according to Boockvar. Even if the investor was able to raise rents by 10% in 2021 and a similar amount last year, rental income would only go up to about $3 million. That leaves around $400,000 for all those other expenses, and property taxes alone in some states alone wipe out that $400,000, he notes.

Sure, those are back-of-the-envelope calculations, but they ring true and illustrate the troubles that lie ahead for both real estate investors and lenders. Loan stress can feed on itself quickly in commercial property as rates rise because loan refinancing becomes more costly and harder to find as banks look to reduce their exposure, which leads to more property sales at lower prices and more risk of losses for lenders.

Declining property values are not coming — they are already here. A widely followed index of commercial real estate prices published by the National Council of Real Estate Fiduciaries plunged 3.5% last quarter, the biggest decline since 2009 and only the second quarterly drop since then. The decline was led by office and apartment properties.

So, where does the risk lie for banks? Mostly at small banks and some large lenders that specialize in real estate. In the Federal Reserve’s 2022 stress tests, Wells Fargo & Co. experienced the biggest dollar value of commercial real estate losses, but M&T Bank Corp. and Huntington Bancshares Inc. experienced the biggest losses as a share of total loan losses and as a share of their capital bases.

M&T lifted its provisions for bad loans significantly last year but mainly for consumer and corporate debt rather than real estate. The bank has cut back its exposure to projects under construction over recent years and said that stress in the hotel sector had diminished. But assisted living and offices are now the areas where problems could start to grow.

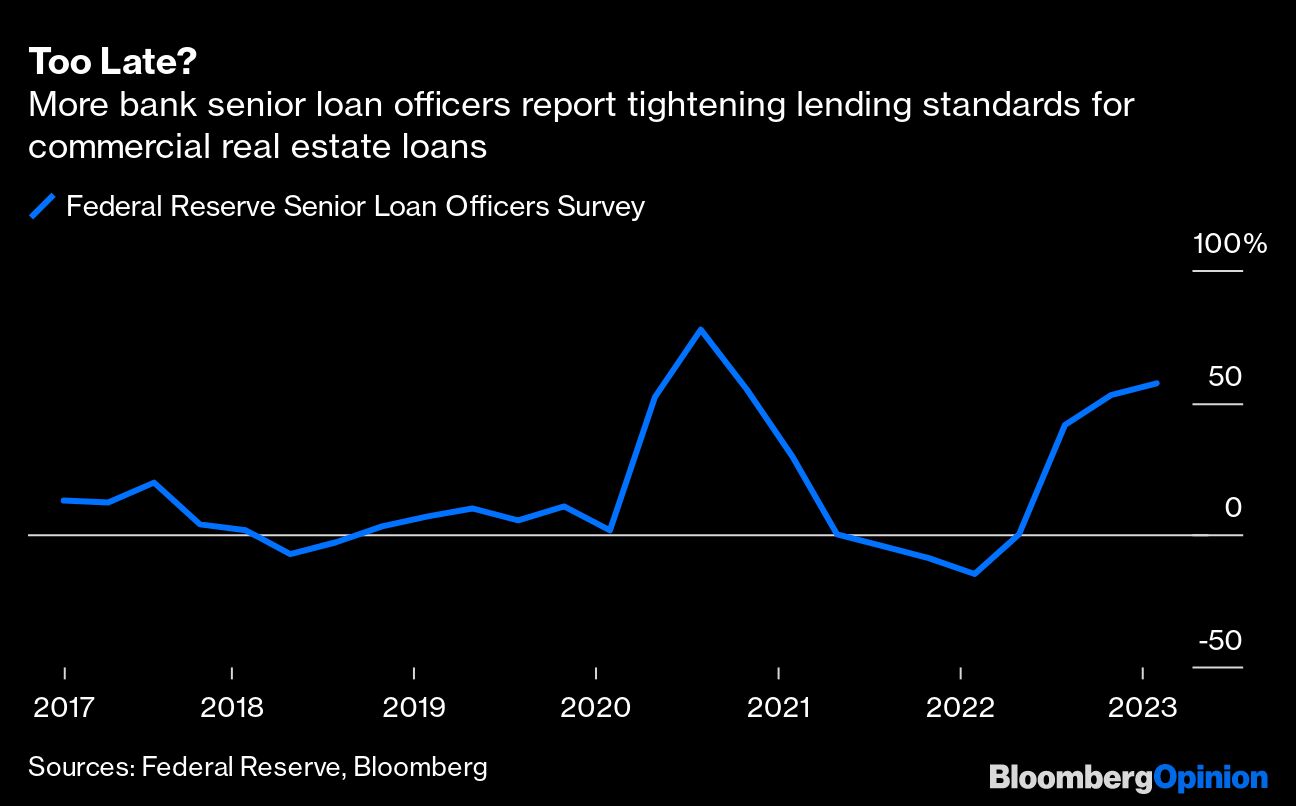

The good news is that lenders have begun tightening standards when it comes to providing credit for commercial real estate. The most recent quarterly loan officer survey from the Fed showed 57.6% of respondents reported tightening standards. The bad news is that this may have come too late, as standards loosened significantly after the onset of the pandemic.

It’s fair to ask whether what’s happening now in commercial real estate could be setting the banking industry up for a repeat of the savings and loan crisis of the late 1980s and early 1990s, when a mass souring of property loans and investments led to a recession. It’s too soon to answer, but what we’ve learned from that and other episodes since is that you can’t have a healthy economy without a healthy banking system. The crisis at Silicon Valley Bank suggests that perhaps the banking system isn’t as healthy as we thought.

--With assistance from Paul J. Davies.

To contact the author of this story: Robert Burgess at [email protected].

© 2023 Bloomberg L.P.