Most advisors claim to provide not just investment services but also in-depth, comprehensive financial planning.

And yet, the vast majority focus on investment management and provide too little planning; in particular, for the wealthy, they offer little or no estate planning guidance. The reason is simple: Gathering assets for investment management can be very profitable for the advisor, even if the advisor doesn’t deliver much performance for the client.

Proactive, in-depth estate planning presents a far greater potential value for families of wealth than investing. Countless families pay their advisors a great deal for their investing “prowess,” and in return receive uncertain results at best. In contrast, qualified advisors can implement estate planning strategies that are certain to disinherit the Internal Revenue Service and save families a massive percentage of their intergenerational wealth.

To adapt an old adage, it’s a choice between having two birds in the hand or one (possibly) in the bush.

Oddly enough, the creators and stewards of significant wealth continue to accept the status quo in which investing is at the heart of wealth advisory services. That’s partly because of investors’ natural desire to beat the market and partly, we believe, because the stewards of wealth don’t understand the relative impact of eliminating tax obligations versus gaining a few elusive points of investment return. Additional returns manifest in the form of larger account balances while tax savings are tangible only in the form of a reduction in taxes. Psychologically, the latter, while significantly larger, is difficult to enjoy. In contrast, an increase in portfolio value—however small in comparison—elicits a euphoric feeling of accomplishment.

We believe that families who are very wealthy—and wish to remain so—need to heed the math and rethink the status quo. While it’s true that people get wealthy by taking risk, they stay wealthy through thoughtful steps like tax mitigation, not by taking needless investment risk.

Wealth Advisory Services: Building Blocks or Roadblocks?

Financial advisors are typically judged by their investment results. Delivering better returns than their peers lands investment managers on the front pages of investment publications and makes them in-demand guests on cable business channels, and this, in turn, attracts return-hungry, new clients.

To understand the extent to which investors are drawn to the promise of returns, look no further than Bernie Madoff’s infamous Ponzi scheme. Predominantly wealthy, highly intelligent investors fell for Madoff’s scheme, partly due to its air of exclusivity and its strangely consistent, high (but not too high) returns. Investors’ emotions don’t discriminate by intellect and a master charlatan is not required to fall prey to the attraction of investment returns.

So it’s no wonder that most investment advisors’ initial pitch is to suggest that they can provide better performance than their counterparts and deliver returns greater than the market. But take a step back, and you’ll find that most investment managers cannot beat the market on a consistent basis. In fact, they often trail the very indexes they seek to beat. And the fees and taxes that come with the approach of active investing make it almost impossible for clients— that’s you—to come out ahead.

Active managers’ inability to provide more value than a low-cost, passive index fund is no great secret: This shortfall has been documented in study after study. And yet, advisors continue to dangle the carrot of delivering “alpha” to their prospects—Wall Street speak for “beating the market.”

Their bait—typically some version of “We can [time the markets and] pick a better asset mix than other firms” or “Not only can our firm pick managers that will outperform the markets, but we can also get you into managers that others cannot”—have been the same for decades. Why does this investing-centric framework persist? You need only follow the money. Active asset managers earned an estimated $600 billion in fees in 2014, according to State Street’s Center for Applied Research. That’s about the gross domestic product of Switzerland. It’s little wonder that 60 percent of financial firms’ capital expenditures go toward attempting to generate short-term performance.

Being a financial advisor can be an extremely lucrative business. Little capital expenditure is required. Barriers to entry are almost non-existent. The business is extremely scalable, and the revenue extracted from long-term clients is recurring and often increasing.

This money spigot has helped to make the financial services industry profitable like no other. In 2016, financial services made up approximately 7.3 percent of the U.S. GDP, but accounts for a significant portion of GDP profits. Translation: A lot of people are moving their money in the form of fees to a much smaller number of people in the form of paychecks—wealth transfer of the worst kind.

Tax Planning: The Ultimate Fulcrum

In a truly client-centered financial industry, the focus would not be on the chimera of investing alpha. Passive index funds would be prevalent. And the resources once devoted to beating the market would be used for the real difference maker: Planning. For the wealthy, estate planning is a fulcrum of unmatched power.

There is no better way to influence the total family balance sheet than by maximizing the amount of wealth that transfers from generation to generation. By minimizing taxes on the transfer of wealth, families can create or protect a legacy. Think of it as disinheriting Uncle Sam and giving the money to your family instead. The transfer tax is an astounding 40 percent, and then 40 percent again to skip a generation. With almost $30 trillion transferring between generations in the coming decades, the importance of effective planning is paramount for families of wealth.

The rules around wealth transfer are straightforward. Currently, a married couple with net worth below $22 million can take advantage of transfer exemptions, lifetime gifts and other non-taxable gifts to remain unscathed by the transfer tax. But every additional dollar of net worth beyond $22 million is taxed at a decimating 40 percent when passed to just the next generation. Then those assets are taxed again when they move to the next generation. And so on.

Effective estate planning can be thought of as delivering a 40 percent immediate return in the form of taxes avoided. Investors simply cannot earn enough, without taking the kind of risk that could jeopardize their wealth, to add more value than that.

By way of a simple example, let’s look at a hypothetical $100-million estate. Let’s say that the investment returns for this estate, whether due to superior management or luck, are 8 percent, rather than the 7 percent market return. That extra 1 percent of return adds up to $1 million before taxes in any given year. Even if the estate doubles the market’s 7 percent return, it’s only earned $7 million in alpha.

In contrast, if the family plans their estate effectively and avoids transfer tax, the savings will leave the family more than $30 million ahead. Try earning $30 million through excess performance.

The best estate planning advisors use tools like recapitalization of businesses, freezes, discounts, and transfers into generation-skipping trusts to help protect family wealth. Effective planning can lead to an exponential advantage in family wealth over time.

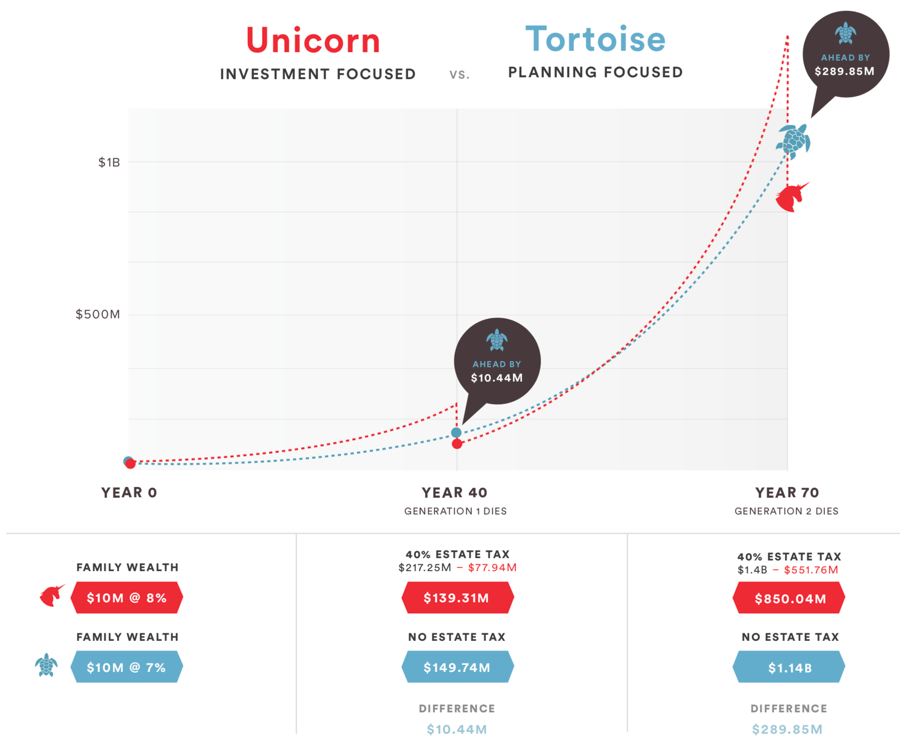

Suppose a firm named “Unicorn Investment Advisory” is an exceptional investment management firm, consistently beating the liquid markets by 100 basis points, while “Tortoise Wealth Advisors” is a planning-focused firm that only uses passive investments. The Tortoise team doesn’t waste their resources attempting to beat the markets but instead focuses its efforts on minimizing transfer taxes.

A wealthy 50-year-old couple with a 20-year-old child considers both firms. Neither spouse has used their lifetime or generation-skipping exemptions. Each has sufficient assets to use their exemptions and also to pay the taxes that will result from the grantor status of the trusts. For simplicity, all returns assume that taxes are paid by the grantor or outside of the portfolio.

Does investing still matter? Should your advisor invest your money well? Of course. But chasing alpha, which consumes time and energy better used for tax planning, isn’t the answer.

Even if successful, modest outperformance is likely achieved at the expense of estate planning, something which when accomplished, rarely increases portfolio risk. By deploying a diversified portfolio of low-cost, passive funds, advisors will likely outperform peers who are attempting to better the markets. Their clients will also pay less in fees. And they will free up important resources to make a certain impact through effective planning. Simply put, your advisor should be focused where their impact will add the greatest value, not weaving a tale of what could be if everything goes as pitched.

Quality estate planning will trump investment planning every day of the week.

Steve Lockshin is a founder and principal of AdvicePeriod, and former chairman of Convergent Wealth Advisors.