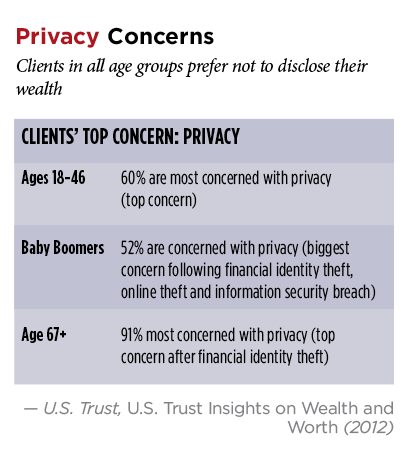

Wealth transfer to younger generations is one of the biggest concerns for families today. Many families feel that the younger generations aren’t ready to handle the wealth they’ll receive;1 in fact, only one-third of wealthy parents have fully disclosed their wealth to their children.2 The perceived unpreparedness, along with a concern for privacy and wealth preservation or asset protection, are some of the key non-tax reasons that many families establish trusts. (See “Privacy Concerns,” this page.) Moreover, many trusts are extremely large due to the $5.43 million gift and generation-skipping transfer tax exemptions in 2015 ($10.86 million per married couple).3 Thus, for many settlors, the sole reason for making a transfer to a trust may be to reduce estate taxes—not to provide immediate benefits to trust beneficiaries.4

Historically, trustees have always provided trust beneficiaries with information regarding trust assets, performance, distributions and taxes. And, most states require that a trustee provide information regarding a trust to beneficiaries. The duty to inform beneficiaries stems from common law and the Uniform Trust Code (UTC).5 A recent trend, however, has developed with many states, particularly the key dynasty trust states, moving to enact beneficiary quiet trust statutes.6

Elements of a Beneficiary Quiet Trust

Beneficiary quiet trust statutes generally provide the settlor the flexibility to waive beneficiary notice of trust assets and keep trust information silent from one or more beneficiaries.7 A settlor who wishes to keep trust information quiet should include or reference specific statutory language in the trust instrument. The language should demonstrate the settlor’s intent to withhold information from one or more beneficiaries, thus protecting the trustee from what might otherwise be considered disloyalty or bad faith.8 In many instances, a settlor may also explain in a letter of wishes why it was in the best interest of the beneficiaries to keep the trust quiet (silent) as to them.

Generally, if the trust is kept quiet as to only one beneficiary, there are many ways to coordinate with other beneficiaries not to disclose trust information to the silent/quiet beneficiary. In addition, it’s important to note that a waiver by the settlor of the trustee’s duty to keep the beneficiaries informed of the trust’s existence and administration usually doesn’t affect the trustee’s other duties.9 A trust protector will often oversee the quiet (silent) beneficiary’s interest.10

A trust document typically includes the following provisions:

1. The identities of the settlor, trust protector and/or advisors;

2. The ability to expand, restrict, eliminate or modify;

3. The rights of beneficiaries to receive trust information.

A quiet beneficiary trust document should also include a provision similar to: “I hereby direct that the Trustee is not required to provide the notice set forth in SDCL Section 55-2-13 to qualified beneficiaries.”11

Discretionary Trusts

Most long-term trusts are established as discretionary trusts to maximize the asset protection for both the settlor and the beneficiaries.12 Additionally, some states have key statutes stating that a discretionary interest in a trust isn’t a property right or an entitlement.13 These statutes are powerful in general from an asset protection standpoint, but even more powerful when combined with beneficiary quiet statutes and directed trusts.14 Generally, the distribution committee of most directed trusts are comprised of family members and advisors, as well as a trustee in the selected situs jurisdiction. This distribution committee composition generally puts families at ease with fully discretionary trusts.15

The combination of a beneficiary quiet provision and a discretionary trust allows a settlor and/or trust protector to select which beneficiaries will receive trust information and when they’ll receive it. It may, of course, be awkward, and potential issues may arise if one child is given access to trust information before others. Consequently, the use of a beneficiary quiet provision isn’t for all families. Few wealthy parents believe that their children will be mature enough to deal with wealth before age 25; 50 percent of wealthy parents believe that their children won’t be mature enough to handle their wealth before age 30; and more than one quarter think their children won’t be mature enough to handle their wealth until the children are age 40.16

The UTC precludes a trust instrument from waiving the duty to inform a qualified beneficiary that has attained age 25.17 Some states have eliminated the notice requirement to minor children by providing that a beneficiary below age 21 isn’t entitled to trust information unless otherwise required by the trust document.18

Reasons for Silence

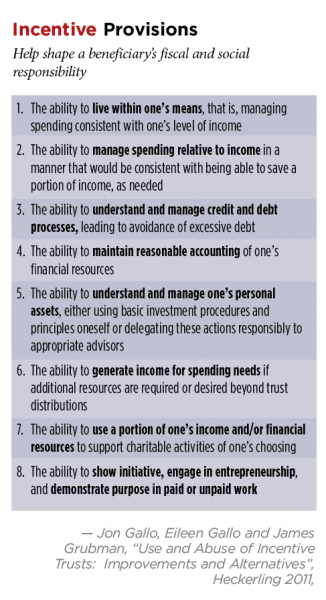

There are many reasons why a parent or grandparent may want to keep trust information silent as to children, grandchildren or great grandchildren. Some settlors are concerned about promoting fiscal and social responsibility within the family, which may be negatively impacted if a beneficiary has knowledge of a large trust. Alternatively, some parent settlors are concerned that financial secrets can lead to guilt, anger and even shame for a beneficiary. Consequently, these parents disclose the trust but include various incentive provisions associated with any trust distributions (see “Incentive Provisions,” this page).

These incentive provisions can guide members of a distribution committee to mentor a child beneficiary to develop his social and fiscal responsibility from a young age, potentially shaping the beneficiary’s future behavior and development.19 There are many ways of structuring incentive trusts to accomplish these goals,20 and these trusts, along with beneficiary quiet trusts, are gaining in popularity to prevent young beneficiaries from becoming “beach bums” and nonproductive members of society.

Another key reason for keeping a trust quiet (silent) from beneficiaries may be wealth preservation and asset protection. Some clients feel that the less a child or grandchild beneficiary knows about a trust or inheritance, the less chance there is for frivolous lawsuits against that child, undesirable friends, identity theft or even kidnapping. A careless child who leaves a trust statement out in plain view for friends, roommates and other outsiders to see is exposing himself to potential problems. Additionally, settlors may want beneficiaries with emotional or psychological issues, drug problems, bad marriages or creditor risks to be unaware of their trusts and unable to access trust funds.21

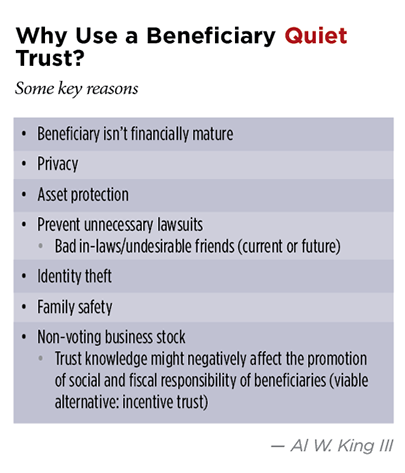

Moreover, a quiet trust is useful when non-voting family business interests are transferred to a trust for estate-planning purposes, but the settlor patriarch prefers not to discuss the direction or operation of the business with younger family member beneficiaries. This strategy makes sense if the beneficiaries aren’t active in the business and their shares are non-voting.22 (See “Why Use a Beneficiary Quiet Trust?” p. 15.)

Regarding the tax reporting of a beneficiary quiet trust, generally, if the trust is discretionary and the beneficiary isn’t receiving any distributions, the tax reporting won’t interfere with the quiet trust status, and the trustee typically wouldn’t have to send tax information to the beneficiary. The only time a trustee would need to send tax information to a beneficiary is if the trust is beneficiary defective or if the beneficiary is taking a distribution and the trustee needs to provide a K-1. However, beneficiary defective trusts23 generally aren’t quiet trusts. Additionally, if the quiet trust were a grantor trust, there would generally be no tax information going to a beneficiary.

Decanting a Quiet Trust

Caution must be taken regarding the decanting of a quiet trust.24 There’s a question as to whether a quiet trust should even be decanted. An advisor should first verify that the new trust situs also has a quiet trust statute.25 If so, advisors also need to verify whether the decanting statute requires the decanting trustee to provide notice of the decant to the beneficiaries. Many state decanting statutes don’t require notice or make notice optional.26

Selecting Trust Situs

Not all states have beneficiary quiet statutes.27 Alaska, Delaware, New Hampshire, Ohio, South Dakota, Tennessee and Wyoming have some of the better beneficiary quiet trust statutes. Those statutes generally provide for: 1) a grantor to waive the trustee’s duty to inform in the trust document, and/or 2) a trust advisor or trust protector to expand or modify the rights of beneficiaries to information relating to the trust. Many UTC states expressly permit quiet trusts by allowing grantors to waive the trustee’s duty to inform the beneficiaries of the trust’s existence before the beneficiaries’ 25th birthday.28 Some statutes exempt a trustee from notice requirements only during the life of the settlor or the settlor’s incapacity.29 Some states allow the trust protector to continue to waive notice even after the death or disability of the settlor.30 Others allow for the waiver of notice but don’t allow the trust protector or advisor to modify notice.31 Flexibility regarding beneficiary notice and the ability to keep the trust silent to one or more beneficiaries are important considerations for situs shopping families.

Bottom Line

Note that for a settlor to take advantage of a beneficiary quiet statute, the trust the settlor establishes would need to be properly sitused and administered in a state with a beneficiary quiet statute. Generally, however, a family wouldn’t need to live in, visit (or even look down when they fly over) these states. Families establishing a beneficiary quiet trust, particularly if it’s a long-term dynasty trust, should also consider asset protection and state tax laws when selecting a beneficiary quiet statute and trust situs.

Endnotes

1. U.S. Trust, U.S. Trust Insights on Wealth and Worth, at pp. 12, 13 (2012).

2. Ibid., at p. 14 (2012).

3. Arden Dale, “Quiet Trusts Popular Amid Gifting Boom,” The Wall Street Journal (Nov. 20, 2012); Kelly Greene and Arden Dale, “Can You Trust Your Kid with $5.25 Million?” The Wall Street Journal (Jan. 18, 2013).

4. William R. Burford, “What the Kids Don’t Know–Deconstructing the Silent’ Trust,” ALI CLE Estate Planning Course Material Journal (June 2014).

5. Uniform Trust Code (UTC) Sections 103(3), 103(13), 813. See also UTC Sections 105(b)(8) and 105(b)(9); Restatement of Trusts Section 173 (1935), A. Scott, Law of Trusts Section 173.

6. Greene and Dale, supra note 3; Alaska Stat. Section 13.36.080; Ariz. Rev. Stat. Section 14-10813; Del. Code Ann. tit. 12 Section 3534; S.D. Codified Laws Section 55-2-13; Tenn. Code Ann. Section 35-15-813; N.H. Rev. Stat. Ann. Section 564-B:1-105; D.C. Code Section 19-1301.05; Maine Rev. Stat. Ann. tit. 18-B Section 105; Mo. Rev. Stat. Section 456.1-105; N.C. Gen. Stat. Section 36C-1-105; Ohio Rev. Code Ann. Section 5801.04; 20 Pa. Cons. Stat. Ann. Section 7780.3; Va. Code Ann. Section 64.2-703; Wyo. Stat. Ann. Section 4-10-813.

7. See statutes listed in ibid.

8. Charles E. Rounds, Jr. and Charles E. Rounds, III, Loring and Rounds: A Trustee’s Handbook Section 6.1 (2015).

9. UTC Section 105; See also note 18, infra.

10. Most of the states with good beneficiary quiet statutes also have complimentary trust protector statutes, for example, Alaska, Delaware, New Hampshire, South Dakota and Tennessee.

11. S.D. Codified Laws Section 55-2-13; Loring and Rounds, supra note 8 at Section 9.9.25 (2015).

12. The three common trust distribution options are: (1) mandatory (that is, all income distributed and/or 1/3 of principal at age 25, 1/3 at age 30 and the balance at age 35); (2) discretionary support (that is, health, education, maintenance and support (HEMS)), or (3) total discretion with either single pot or separate shares for each child. A total discretionary interest trust maximizes the beneficiary quiet provisions as well as the asset protection and the flexibility regarding incentive trust provisions. Many trusts start as single pot to minimize administration and then convert to separate shares once distributions commence to prevent family disagreements.

13. Daniel G. Worthington and Mark Merric, “Finding the Best Situs for Domestic Asset Protection Trusts,” Trusts & Estates (December 2014) at p. 45; Alaska Stat. Section 13.36.080; Ariz. Rev. Stat. Section 14-10813; Del. Code Ann. tit. 12 Section 3534; S.D. Codified Laws Section 55-2-13; Tenn. Code Ann. Section 35-15-813; Wyo. Stat. Ann. Section 4-10-813.

14. A directed trust structure is one in which an administrative trustee is being directed with regard to investment and/or distribution decisions. For example, a settlor appoints an investment committee or trust advisor who directs the administrative trustee to make all investment decisions. This setup may also be done relating to distributions and a distribution committee or advisors. See Al W. King III and Pierce H. McDowell III, “Delegated vs. Directed Trusts,” Trusts & Estates (July 2006), at p. 26. Most of the quiet trust dynasty states are also directed trust states (Alaska, Delaware, New Hampshire, South Dakota and Tennessee).

15. See ibid. Note that family distribution committee members may determine distributions for HEMS, but tax-sensitive distributions require independent distribution committee members (Internal Revenue Code Section 672(c)).

16. U.S. Trust, U.S. Trust Insights on Wealth and Worth (2012).

17. UTC Section 105(b)(8).

18. S.D. Codified Laws Section 55-2-13.

19. A distribution committee may be used, via incentive provisions, to foster fiscal and social responsibility so as to maximize the beneficiaries’ development, as well as their distributions from the trust.

20. Strict incentive trust provisions, for example, $1 trust income for $2 earned income. See Nancy G. Henderson, “Managing the Benefits and Burdens of Inherited Wealth with Incentive Trusts,” Denver Estate Planning Council,

Jan. 20, 2011. Another approach to incentive provisions is one proposed by Jon and Eileen Gallo. This approach, defined as “Results Oriented Trust Environment,” uses “behavioral benchmarks that focus on and correlate with the beneficiary learning and demonstrating financial literacy and money management skills.” See Jon Gallo and Eileen Gallo, “Use and Abuse of Incentive Trusts,” Heckerling Institute on Estate Planning, 2011.

21. A third-party trust is one created by a third party for the benefit of someone other than himself. A spendthrift or domestic asset protection trust (DAPT) is a trust created by a settlor in which he’s a permissible beneficiary of his own trust (that is, self-settled). Some beneficiary quiet states (Alaska, Delaware, Missouri, New Hampshire, Ohio, South Dakota, Tennessee, Utah, Virginia and Wyoming) provide asset protection features for DAPTs, such as self-settled statutory protection from creditors, limited liability corporation charging order protection as the sole and exclusive remedy, discretionary interest protection and spendthrift provision protection. See also Worthington and Merric, supra note 13.

22. Donald D. Kozusko, “In Defense of Quiet Trusts,” Trusts & Estates (March 2004) at p. 20.

23. A beneficiary defective trust is one in which the beneficiary is treated as the owner for federal income tax purposes; see Richard A. Oshins, The Beneficiary Defective Inheritor’s Trust (2008).

24. Decanting is the process of appointing trust property in an existing trust to another trust; it’s a discretionary distribution of all trust assets from one trust to another trust by the trustee. Rashad Wareh and Eric Dorsch, “Decanting: A Statutory Cornucopia,” Trusts & Estates (March 2012) at p. 22.

25. Alaska, Delaware, New Hampshire, South Dakota and Tennessee.

26. See note 22.

27. Greene and Dale, supra note 3.

28. UTC Section 105(b)(8).

29. See, for example, Cal. Prob. Code Section 16069.

30. See S.D. Codified Laws Section 55-2-13; Tenn. Code Ann. Section 35-15-813.

31. See, for example, the statutes listed in note 6.