On Oct. 28, 2021, President Joe Biden announced a framework for changes to the U.S. tax system to raise revenue for a $1.75 trillion version of the Build Back Better Plan. Here are some of the highlights that impact estate and trust planning:

Increased income taxes impacting fiduciary income taxes: The following surtaxes will be effective for tax years beginning on or after Dec. 31, 2021.

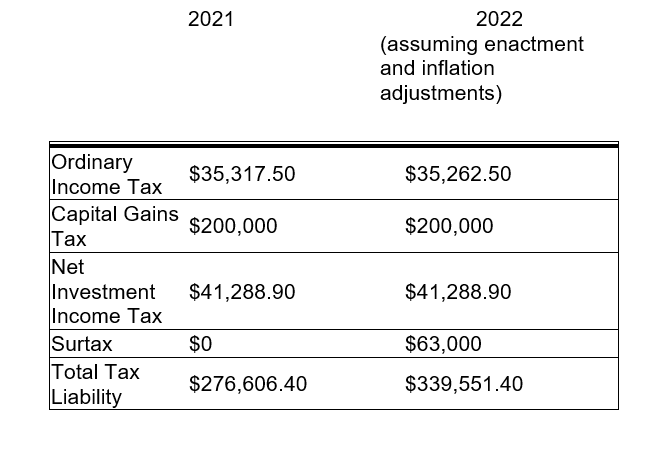

- Surtax of 5% on the modified adjusted gross income of a trust or estate above $200,000

- Additional 3% surtax on the modified adjusted gross income of a trust or estate above $500,000

Example: Assume your client has a trust with $1 million in capital gains and $100,000 of ordinary income.

Qualified small business stock (QSBS): The gain exclusion for QSBS will be reduced to 50% of gain from 100% where the taxpayer is a trust for sales and exchanges occurring after Sept. 13, 2021, unless further to a binding contract in effect on that date and not materially modified after that date. In addition, the excluded gain would be an AMT preference item.

What Didn’t Make It In

Many of the revenue raisers from the previous legislative text that originated from the House Ways and Means Committee were dropped from the latest version:

- No change in estate, gift, and generation-skipping transfer tax exemption amounts

- No change to applicability of valuation discounts.

- No change to estate inclusion of grantor trusts; and

- No change to the treatment of sales or exchanges with grantor trusts.

Observations on the Framework

Despite the political dramatics of a presidential press conference and speculation on the timing of votes, there isn’t yet a deal. As a result, advisors need to be mindful that this legislation could change again or may not pass at all. If this version of the legislation is passed, estate planners will be grateful that many transfer tax planning techniques will be unaffected. However, it will reinforce the “paradigm shift” away from the emphasis on estate taxes to planning techniques driven by income tax considerations in an effort to mitigate the impact of the proposed surtax, particularly on non-grantor, complex trusts.