Following three years of material underperformance relative to U.S. equities, the MSCI EM benchmark has posted a total return of 16 percent YTD. Clearly the bottoming of both oil prices (and much of the commodity complex) and domestic growth conditions across the EM landscape have been important catalysts.

However, the level of USD gains - and just as importantly, the geographic distribution of such gains - suggests the principal driver of EM equity performance thus far in 2016 has been the global hunt for yield, rather than any meaningful improvement in underlying fundamentals. This is ultimately exogenous to domestic growth across the EM landscape.

What is really driving much of all this activity is global rates, or the absence of any measurable nominal yield across much of the Organization for Economic Cooperation and Development (OECD) landscape. The lurch for yield we’ve seen this year is based on the premise that weak global growth conditions will deter central banks - most notably the Federal Reserve - from raising rates or reducing unconventional stimulus.

What we are witnessing is not a massive cyclical recovery in EM economies and corporate earnings, but rather a global carry trade. Emerging market bonds have seen unbelievable levels of inflows as a result - a record $25.5 billion in 2016.

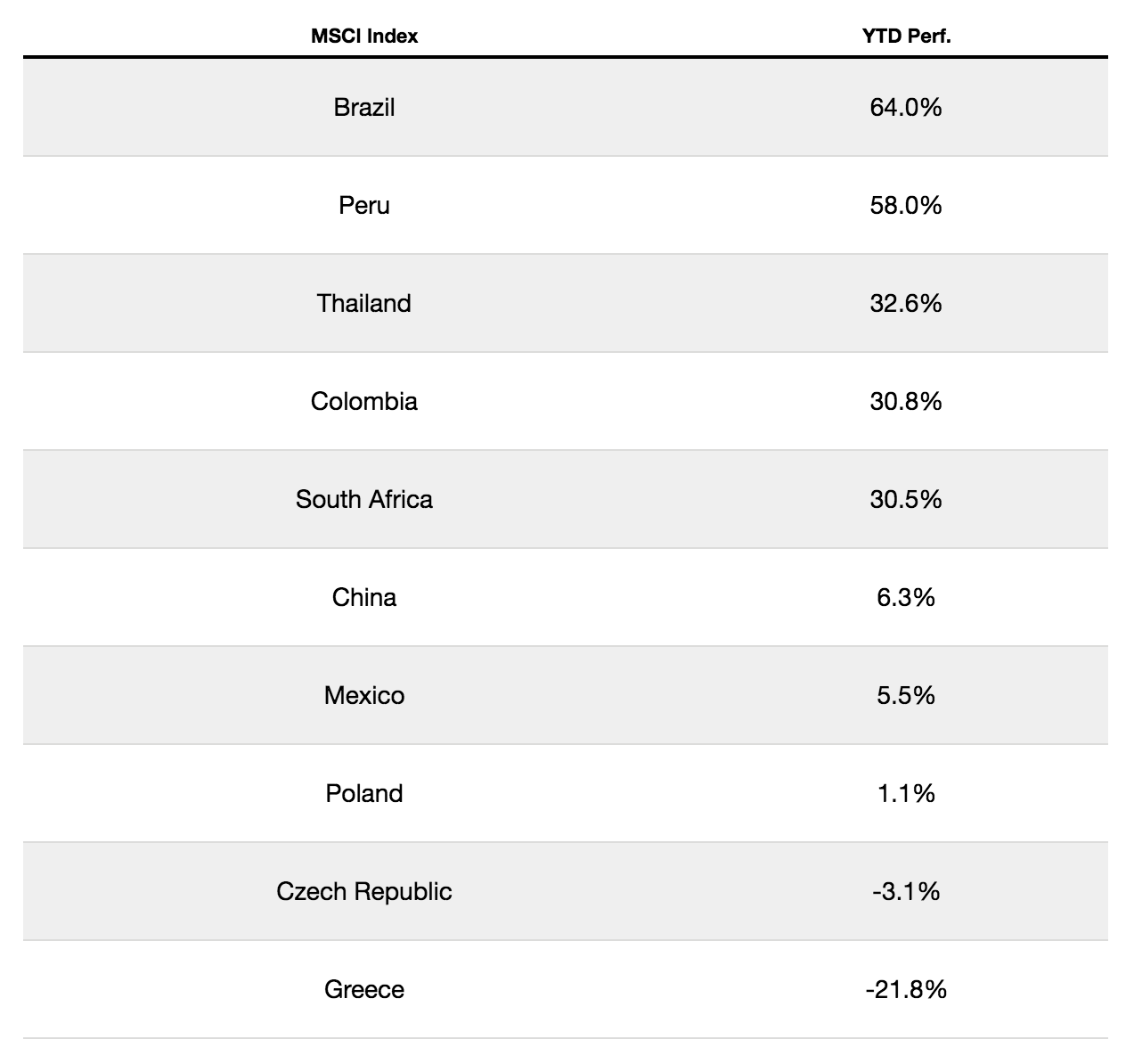

The distribution of performance across EM equity markets reflects this basal reality. Outperformance - as the chart below shows - is largely centered in “high-yield” countries and/or those with significant commodity exports. Indeed, one could make the philosophical extension that commodity price gains also reflect the relatively weak dollar environment, which is itself a manifestation of low nominal rates.

Source: MSCI 8/23/16 | Click to Enlarge

Source: MSCI 8/23/16 | Click to Enlarge

If we decompose equity returns in some of the best-performing EM countries YTD, the currency component is enormous.

The Brazilian real has rallied over 20 percent this year. The South African rand, Colombian peso and Russian ruble have also made big gains. Turkey is another interesting illustration of this disconnect. The currency has been rock solid, despite a presumptive military coup and an unusually capricious effort to subvert dissent across media, the judicial system and the economy - effectively all the significant checks on power.

EM equity gains that have been driven by the global hunt for yield rather than any meaningful improvement in fundamentals resulted in mixed outcomes for Oppenheimer Developing Markets Fund’s (ODMAX) shareholders.

In all market climates, our focus remains unchanged. We are long-term investors in extraordinary companies across the developing world - companies with sustainable competitive advantages, real options and durable growth. While we have trailed the index in this momentum-driven year, we remain committed to fundamentals, which like gravity, exert a long-term pull on asset prices. Always have, always will.

While we do not claim any prescient ability to predict inherently complex variables like global rates, oil prices or short-term currency movements, we do believe that the stabilization trade will ultimately run its course and a return to fundamentals will eventually emerge.

Multiples in many of the “high-yield” outperformers (e.g., Brazil) look unsustainably expensive, unless there is a material expansion of earnings, which seems unlikely. Much of the EM rally - in equities and currencies - has little to do with long-term earnings power or competitive advantage.

In the long term, however, these are what ultimately matter to equity investors.

Justin Leverenz, CFA, is Director of Emerging Markets Equities, Portfolio Manager, for Oppenheimer Funds. More information about Oppenheimer Funds’ emerging market strategies can be found here.

{kind=link}