“Mean reversion” is an oft-touted phrase in financial parlance. It simply describes a tendency, real or perceived, for interest rates, security prices or economic indicators to return to their long-term averages after short-term excursions. Often, mean reversion’s a self-fulfilling prophesy: as market participants take note of abnormal movements, they start to trade against the crowd. And, when enough contrarians tip the balance, the market moves to historically “correct” levels.

Interest rates nowadays are at depressed levels. They’ve been sent lower by Fed action, but they’re being kept low by market forces. Consider ten-year Treasury yields. Over the past 25 years, they’ve averaged five percent. At last look, though, the ten-year T-note was bid at just 2.5 percent.

And what of stocks? What’s normal for dividends? Since 1990, S&P 500 dividend yields have averaged 2.1 percent. The blue chip payout now? About 1.9 percent. There’s been digression, too, in the S&P earnings yield. Since the ‘90s, the norm’s been 4.8 percent, a few ticks below the current five percent level.

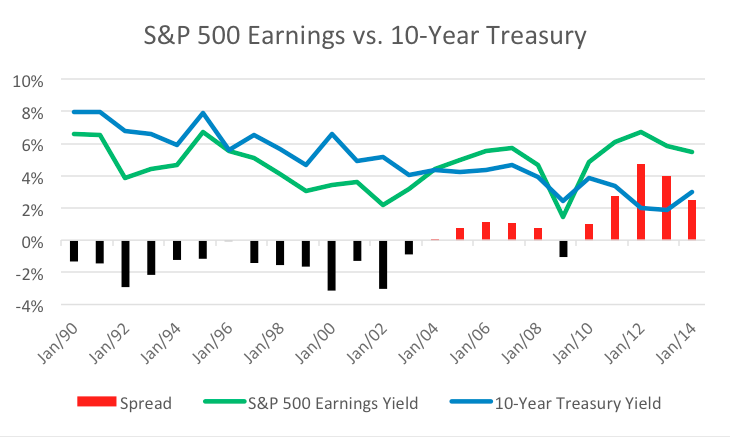

When you map the spread between the S&P earnings yield and ten-year Treasury rates, you can more readily see the development of an anomaly in the relationship. And a possible denouement.

{kind=link}

Earnings yields are typically lower than Treasury rates but for very limited periods of time—now being one of them—the situation’s reversed. Right now, the spread favors stocks by 2.6 percent versus a quarter-century average deficit of 22 basis points.

Believers in mean reversion must be itching still. Though the earnings yield premium has shrunk from its historic 2012 high, there’s still plenty of room for further contraction. Reversionistas would likely say that stocks are still cheap and bonds dear. And that, for them at least, makes a bullish case for stocks and a bearish one for bonds. For the spread to narrow or invert, Treasury rates will have to rise, blue chip earnings will have to fall or stock prices will have to turn up.

Wanna bet against that?

Brad Zigler pens Wealthmanagement.com's Alternative Insights newsletter. Formerly, he headed up marketing and research for the Pacific Exchange's (now NYSE Arca) option market and the iShares complex of exchange traded funds.