By Jim Bianco

(Bloomberg Prophets) --For most of the post-crisis period, stock market bulls have wished for inflation to return. They claimed it would be a validation of a strong economy and good earnings, and would lead to a rotation out of fixed-income assets and into riskier investments such as equities.

Stock bulls should be careful what they wish for. The chart below shows that the U.S. 10-year inflation breakeven rate, or the bond market’s expectation for the average inflation rate over the next 10 years, is the highest since 2014. But rather than acting as a tailwind to stocks, the return of inflation may actually prove to be a headwind.

To understand why, it's important to consider the bear case for stocks. It argues that risk markets have been manipulated higher via central banks' quantitative easing programs. These purchases of bonds push down interest rates, forcing investors to take on more risk to generate decent returns. The fear is that any balance-sheet reduction would have the opposite effect. The Federal Reserve has promised a reduction in its balance sheet that would be gradual as a way to avoid disrupting markets. While this sounds great in theory, any whiff of inflation could force the Fed to move at a much faster pace.

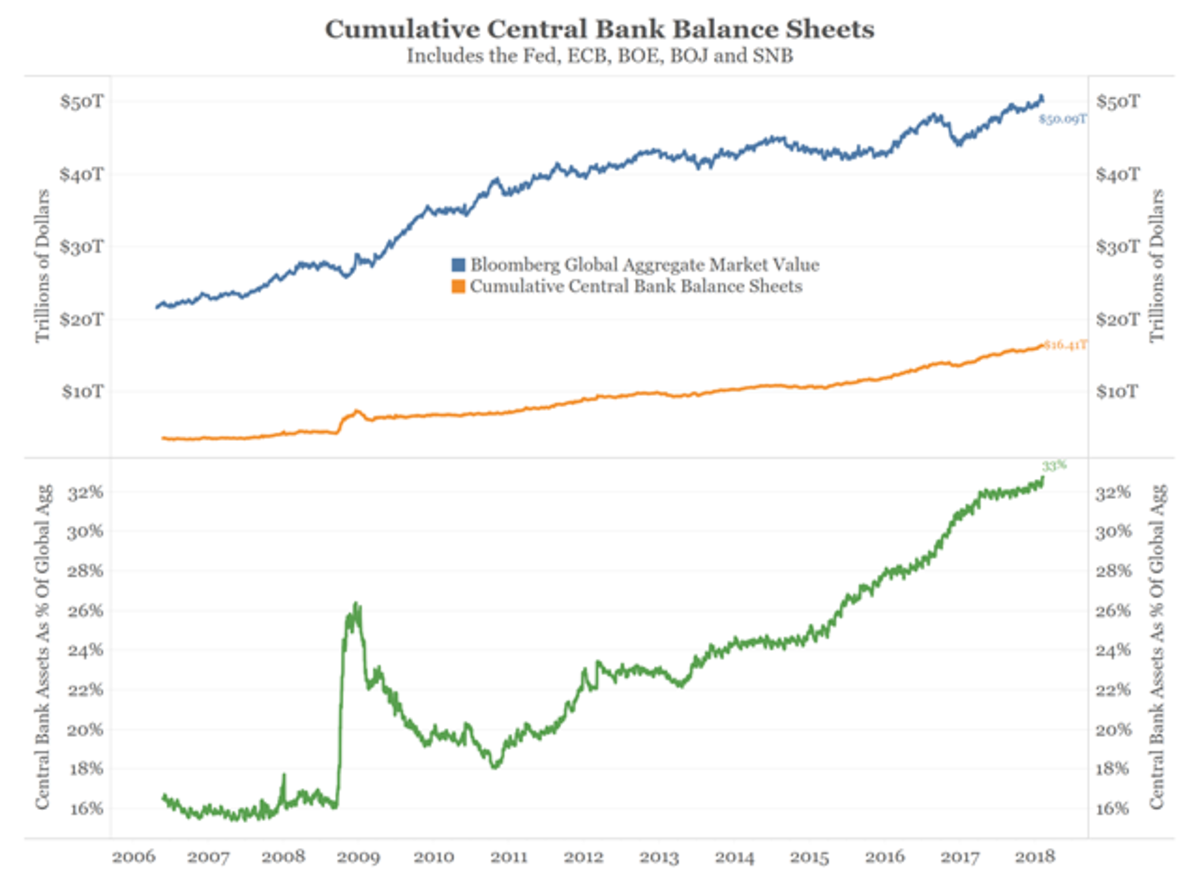

The chart below shows the cumulative size of the five largest central bank balance sheets is a record $16.4 trillion (China is excluded since they do not have a freely convertible currency). Simply put, central banks have never owned more securities. This means their collective policies have never been easier.

As the next chart shows, QE has bloated central banks’ balance sheets so much that they now hold the equivalent of 33 percent of all sovereign debt worldwide, up from roughly 15 percent pre-crisis.

Evidence that the central banks have been too easy can be seen in the next chart. Despite the Fed’s five rate hikes and an announced taper of its balance sheet, financial conditions recently set a new “easy” extreme.

So, global central bank policy is still very accommodative. The European Central Bank and Bank of Japan are still expanding their balance sheets, more than offsetting any reduction in the Fed’s balance sheet.

When central banks say they will take an extremely gradual approach to reducing their balance sheets, they are making a major assumption that inflation will remain tame. Unfortunately, the markets now perceive inflation to be returning and fear central banks can no longer be gradual.

The chart below shows the rolling six-month correlation between the Chicago Board Option Exchange Volatility Index, or VIX (a measure of risk), and U.S. 10-year Treasury Inflation-Protected Securities breakeven rates (inflation expectations). The correlation between these metrics turned negative in the late 1990s and went deeply negative in the post-crisis era. In other words, higher inflation expectations coincided with lower market risk.

In the last year, however, this correlation has risen to its highest level in more than a decade and is almost positive. This means higher inflation expectations would be perceived as a problem for risk markets.

If inflation is on the verge of becoming a problem, then central banks are running easy policies that will foster more of it! If they choose to combat inflation by dramatically slowing their bond purchases, global bond markets lose their largest buyer. Who will take central banks’ place? If, on the other hand, central banks ignore inflation concerns and keep buying, inflation and risk may move higher in tandem.

This week has featured extreme volatility tied to derivatives based on the VIX. These types of unwinds do not create a trend, they merely exacerbate it. The VIX started higher on concern that inflation would force central banks to reduce their balance sheets at a much faster pace than anticipated.

Our fear is that investors, and even the new Fed chair, Jerome Powell, may be missing the larger message as one VIX fund after another closes shop. The return of inflation could be a huge problem for risk markets.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Jim Bianco is the President and founder of Bianco Research, a provider of data-driven insights into the global economy and financial markets.

To contact the author of this story: Jim Bianco at [email protected] To contact the editor responsible for this story: Robert Burgess at [email protected]

For more columns from Bloomberg View, visit bloomberg.com/view