Exchange-traded fund provider IndexIQ has launched two new alternative ETFs that fill out its suite of hedge fund strategies. Now, according to CEO Adam Patti, “an investor or advisor can create a portfolio with a wide range of risk-return characteristics from conservative to moderate to aggressive.”

The IQ Hedge Event-Driven Tracker ETF (NYSE Arca: QLE) and the IQ Hedge Long/Short Tracker ETF (NYSE Arca: QLS) were launched on March 24 and join the IQ Hedge Market Neutral ETF (NYSE Arca: QMN) and the IQ Hedge Macro Tracker ETF (NYSE Arca: MCRO) to cover the bases on the hedge fund infield (IndexIQ’s flagship IQ Hedge Multi-Strategy Tracker (NYSE Arca: QAI) has been providing broad-based exposure to the panoply of hedge tactics since 2009).

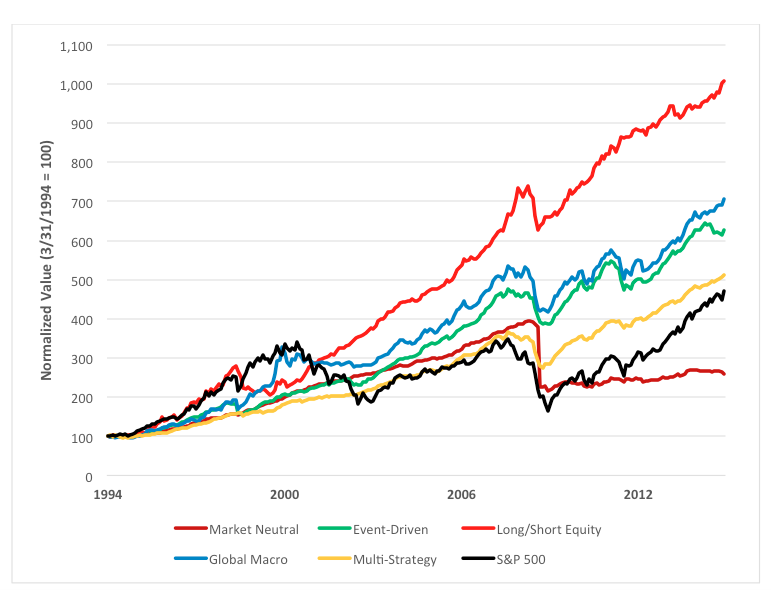

Mixing and matching strategy certainly works to dampen volatility, if long-term hedge fund results are anything to go by. Fund performance, measured by Credit Suisse Hedge Fund Indexes, have varied mightily over the past two decades, with the multi-strategy approach, at the cost of a relatively middling return, yielding the lowest annualized volatility.

| Strategy | 21-Year Return | Annualized Volatility |

|---|---|---|

| Long/Short Equity | 907% | 9% |

| Global Macro | 605% | 9% |

| Event-Driven | 527% | 6% |

| Multi-Strategy | 411% | 5% |

| Market Neutral | 160% | 10% |

| S&P 500 | 372% | 15% |

This year, history seems to be repeating itself, at least at the top of the table. Through February, long/short equity’s up five percent, nearly double the S&P’s gain. February’s most-improved award goes to event-driven which gained more than two percent, reflecting this year’s busy M&A calendar.

In light of the above, IndexIQ’s launch timing is propitious. Nothing like a little wind at your back when you float new products. IndexIQ hopes to attract “completion” business from users of alternative investment products aiming to build customized portfolios. Already got market neutral exposure? Here, add dollops of long/short equity. Global macro already covered? Slather on a little event-driven.

So why not just buy the multi-strategy product and be done with it? Well, there’s certainly cost to be considered. All of the IndexIQ products have a base cost of 75 basis points (0.75 percent), but because they’re funds-of-funds, there are acquisition fees layered atop. The QAI multi-strategy fund’s net cost is actually 91 basis points. The carrying costs for most of the other ETFs are slightly north of 100 basis points. Only the market neutral QMN portfolio, at 85 basis points, is cheaper than QAI.

Budget-minded investors and their advisors will need to rely on some keen optimization skills to find a mix that betters QAI on cost and potential reward.

Brad Zigler is REP./WealthManagement's Alternative Investments Editor. Previously, he was the head of marketing, research and education for the Pacific Exchange's (now NYSE Arca) option market and the iShares complex of exchange traded funds.

{kind=link}