According to The Chronicle of Philanthropy, 12 of the 50 most generous donors in 2014 are from the technology industry, and a stunning number of them are under age 40. The amount contributed by tech entrepreneurs increased tenfold from 2010 to 2014 and accounted for nearly half of all donations made by the top 50 philanthropists in 2014.1 Young tech donors are taking The Giving Pledge.2 Charitable giving is no longer an afterthought for young tech clients, but an integral part of these young clients’ wealth planning.

Estate planners know that each client poses his own unique challenges to overcome. But, when it comes to young tech industry entrepreneurs in private companies considering their charitable giving options, the challenges can be extraordinary. To provide value to these clients, planners must navigate tax and non-tax considerations unique to this market segment. Often, a well-timed charitable contribution will bestow significant tax benefits.

Typical Client Characteristics

These clients are typically in their 20s or 30s. While they may be single or married, their family aspirations usually aren’t fully realized. They may not have children but plan to have them, or they may have one or more young children. They often have modest current net worth but tremendous “upside potential.” It isn’t uncommon for these clients to have $1 million or $2 million of net worth but own shares and options in a start-up company that have the potential to catapult their net worth to

$30 million or more in a year or two.

To Give or Not to Give?

The first consideration for young clients is whether they wish to make any significant charitable gifts given their present circumstances. For some, no matter how significant their wealth or anticipated wealth, they won’t be inclined to make significant charitable gifts for purely practical reasons. Sometimes, young clients generating significant wealth for the first time aren’t yet willing to consider giving portions of it away. Some of the factors they might consider in deciding whether to make significant charitable transfers include:

(1) Current and anticipated wealth level.

(2) Needs of children or anticipated children born or adopted later, including support and schooling.

(3) Anticipated living expenses, including possible changes in lifestyle.

(4) Possible need for new business opportunities and start-ups.

(5) Possible gifts to other family members.

(6) Tax benefits of charitable gifts.

(7) Possible “rainy days.”

These and other practical considerations present an initial threshold question for young clients considering current charitable gifts. Assuming a client believes a significant charitable gift is desirable, other factors will come into play.

Selecting the Assets to Give

Tech industry clients often hold a concentration of private company stock and options. As a result, it’s important to understand the rules of charitable giving generally and how those rules apply to their unique assets.

Charitable giving tax rules—background. The Internal Revenue Code permits donors to claim an income tax deduction for contributions to eligible charities as defined in IRC Section 170(c).3

When appreciated assets are contributed, the amount deductible is generally limited to the donor’s basis (that is, no deduction is allowed for the appreciation component).4 But, when a sale of the asset would produce long-term capital gains (LTCGs), a full fair market value (FMV) deduction is allowed for contributions to public charities, but generally limited to basis for contributions to private foundations (PFs).5

In addition, all contributions in a given calendar year are subject to a limitation based on a donor’s adjusted gross income (AGI).6 Contributions to a public charity will generally be limited to 50 percent of the donor’s AGI for the year.7 Contributions to a PF will generally be limited to 30 percent of AGI.8 The limitations are further reduced if the donor is contributing appreciated assets that would, if sold, be taxed as LTCGs. When appreciated assets are contributed, the limitations are reduced from 50 percent to 30 percent for public charities, and from 30 percent to 20 percent for PFs.9 Unused deductions may be carried forward for five years.10

Giving stock options. Stock options are a common form of equity compensation for tech industry clients working in private companies. Stock options refer to an employee’s right to purchase shares of stock for a fixed price after a period of time that’s often dependent on continued employment. The price at which the employee may purchase the underlying stock (the “exercise price”) is generally the FMV of the shares on the date the stock option was granted. There are two types of stock options: (1) incentive stock options (ISOs); and (2) nonqualified stock options (NSOs).

ISOs are special. They aren’t taxed when issued or exercised. Rather, the client is taxed when the shares obtained from exercising the options are sold.11 If the client holds the underlying shares for longer than two years from the date the options were granted and for longer than one year from the date the options were exercised, a sale of the shares will trigger LTCGs.12 Therefore, a contribution of those shares to a public charity would result in an FMV charitable contribution deduction. If the client hasn’t held the shares long enough, a sale of the shares will trigger ordinary income,13 and any deduction for contribution of those shares would be limited to basis. While ISO shares may be transferable, the options themselves aren’t transferable during the client’s lifetime.14

NSOs are stock options that don’t qualify as ISOs. While an NSO may be transferable, it’s usually not advantageous to give them to charity. When the options are exercised, the client will need to include in gross income the difference between the FMV of the shares and the exercise price.15 This is so even if the client transfers the options to charity, and the charity later exercises them. As a result, the tax implications to the client will be the same as if the client had exercised the NSO and subsequently transferred the shares to charity. The client will have ordinary income, the shares will receive a tax basis equal to FMV and the client will receive an equal and offsetting deduction for completing a gift of the shares to charity.16

As a result of these rules, clients generally don’t make gifts of stock options (whether ISOs or NSOs) to charities during the client’s lifetime. However, it’s very common to exercise options and contribute the underlying shares.

Giving stock. Tech industry clients often own stock in a private company. Specifically, the client might hold:

(1) Founder’s shares from the initial formation of the company.

(2) Shares received as compensation.

(3) Shares purchased that don’t represent compensation.

(4) Shares from the exercise of options.

As planners, we’ll always need to know which of these we’re dealing with when considering charitable contributions.

The first consideration in contemplating a gift of private company stock is whether any restrictions apply to the shares that would prevent transfer. If the shares can’t be transferred due to restrictions imposed by the company, the client’s options will be to wait until the restrictions expire, seek a modification of the restrictions or give other assets.17

The next consideration is whether any part of the contribution will be limited due to ordinary income or short-term capital gains potential. In essence, we need to know that any ordinary income potential in the stock has been cleared by taking the stock into income18 and that any capital gains potential in the stock will qualify for LTCGs treatment. If the shares are “founder’s shares,” they’ll generally be capital assets and will have a tax basis close to zero.19 If the shares were purchased and weren’t compensation even in part, they’ll have a basis equal to the purchase price paid for the stock, and there’ll be no ordinary income potential. If the shares were obtained on the exercise of an option, they’ll generally have a tax basis equal to the exercise price plus any gross income recognized on exercise.20 Often, the client’s accountant and/or financial advisor will know the status of the shares, and confirming that status is critical to the planning.

Once the planner has ascertained that the shares are capital assets, the next step is to determine if the shares have been held long enough to qualify for LTCGs on a sale.21 If the shares qualify for LTCGs treatment on a sale, contributing those shares to a public charity will give rise to an FMV charitable contribution deduction (subject to AGI limitations). Otherwise, a deduction for a contribution of the shares will be limited to basis.

Timing of Gifts

When it comes to charitable gifts of private company stock, timing can be everything. The planner will need to understand the client’s goals and any upcoming income tax events to determine the best course of action.

In general, the client will want to time a charitable gift to take place in a calendar year when the client will have substantial income or capital gains to offset with the deduction. For example, if a client has 100,000 shares with zero basis and constituting LTCGs property, the client might decide to sell 50,000 shares and, in the same calendar year, contribute 10,000 shares to a public charity. The client will receive an FMV charitable contribution deduction (subject to AGI limitations) and avoid capital gains on the sale of the contributed shares. Also, the deduction from the contribution will soften the impact of the client’s sale of shares.

If the taxable event is an upcoming company transaction, extra caution is necessary to avoid the assignment of income doctrine. Under this judicial doctrine, when a taxable event is deemed to have been complete enough prior to the contribution of shares, the client will remain taxable on the gains from the sale even though the sale is ultimately consummated by the charity, and the charity gets the money. The application of this doctrine hinges on whether the charity is legally obligated to proceed with the sale after receiving the shares.22

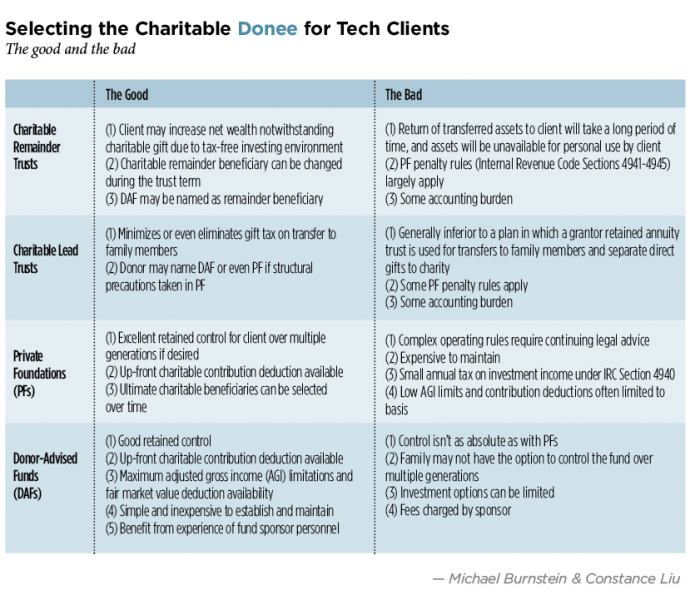

Selecting the Donee

Once the client has decided to make a contribution and selected the asset to give, the next step is to select the appropriate donee. The client’s choices will include charitable remainder trusts (CRTs), charitable lead trusts (CLTs), PFs and public charities (including donor-advised funds (DAFs)). The vehicle choice is partially driven by the client’s short and long-term goals and partially by tax considerations. A complete review of these techniques is beyond the scope of this article, but the following are highlights of each. For more information, see “Selecting the Charitable Donee for Tech Clients,” p. 56.

CRTs. CRTs make sense for a client who wishes to defer the income tax on the sale of low basis stock in exchange for a modest contribution to charity and accompanying income tax deduction. The client will typically set up a charitable remainder unitrust (CRUT)23 and contribute the low basis stock. The trust instrument will typically provide that the client will receive an annual payout equal to 5 percent of the value of the trust from year to year for a period not to exceed the life or lives of the donors or 20 years.24 At the end of the trust, an amount calculated to equal 10 percent or more of the initial contribution passes to one or more public charities.25 The sale of appreciated stock by the CRUT won’t be immediately taxable, but payments back to the client will be subject to income tax when received, and the payments will carry out the highest tax items first.26

CLTs. CLTs can make sense for clients who would like to make a transfer to children or others over time, minimize the gift tax associated with the gift and benefit charity along the way. The client contributes assets to the CLT, and the CLT is obligated to make annual payments (usually a guaranteed annuity amount) to the charity for a period of years, after which the remainder passes to children or other non-charitable beneficiaries.27 The CLT may be structured to yield an income tax deduction up front for the charitable payments, but the trade-off is the trust must be structured as a grantor trust, and thus all income and gains over the coming years will be taxed to the client.28

PFs. PFs may appeal to clients who are in need of a current year income tax deduction but would like to select the ultimate charitable recipients over time. PFs can be structured as trusts or corporations. They’re generally required to distribute 5 percent of their net assets each year to public charities or other qualified recipients.29 Due to the complexity and expensive ongoing maintenance costs,30 these are generally unattractive to all but the wealthiest clients, and even those will often opt for a DAF instead.

DAFs. DAFs compete with PFs when the client wishes to obtain a current deduction while retaining the ability to select the ultimate charitable recipients later. These are offered by community foundations and increasingly by financial institutions (through affiliated public charities). While the client doesn’t have an absolute right to select charitable beneficiaries, the client has the ability to advise the sponsor as to desirable beneficiaries, and these recommendations are generally followed.31 Due to their simplicity and excellent tax benefits, these have become very popular in recent years.

Endnotes

1. Alex Daniels and Maria Di Mento, “Young Tech Donors Take Leading Role in Philanthropy 50,” The Chronicle of Philanthropy (Feb. 8, 2015).

2. www.givingpledge.org.

3. This article will focus on the federal income tax rules of charitable giving. Charitable contributions are deductible against the regular income tax and the alternative minimum tax (AMT). See Internal Revenue Code Sections 55-59 for AMT rules. The deductibility of charitable gifts against state income tax varies from state to state.

4. IRC Section 170(e)(1)(A).

5. Ibid and Section 170(e)(1)(B)(ii). A full fair market value (FMV) deduction is allowed for contributions of publicly traded stock to private foundations (PFs). Section 170(e)(5).

6. IRC Section 68, which limits itemized deductions claimed by high income individuals, would also limit the deduction for charitable contributions in a particular tax year.

7. IRC Section 170(b)(1)(A). The deductibility of gifts to private operating foundations, flow-through foundations and foundations maintaining common funds are treated in a similar manner as gifts to public charity. For purposes of this article, references to public charity include these types of PFs. Sections 170(b)(1)(A)(vii) and (F)(i)-(iii).

8. Section 170(b)(1)(B). This limitation can be even tighter if the 50 percent of adjusted gross income (AGI) limitation category has been used in the same year.

9. Sections 170(b)(1)(C) and (D).

10. Sections 170(b)(1)(B)-(D) and (d)(1)(A).

11. IRC Section 421(a).

12. IRC Section 422(a). The client must also be an employee of the company when the options were granted and continue to be an employee until three months before exercising the options.

13. Section 421(b).

14. Section 422(b)(5); Treasury Regulations Section 1.421-1(b)(2).

15. IRC Section 83(a). A Section 83(b) election to recognize income on the date the options are granted is possible if the options have a readily ascertainable FMV. See Treas. Regs. Section 1.83-7(b)(2) for factors determining whether options have a readily ascertainable FMV.

16. If the client decides to transfer nonqualified stock options to charity, the structure set forth under Private Letter Rulings 9737014 (June 13, 1997), 9737015 (June 13, 1997) and 9737016 (June 13, 1997) should be followed so that the timing of the charitable contribution is simultaneous to the income recognition event.

17. Transfer restrictions can be found in the company’s bylaws and shareholder agreements. Examples include: (1) limiting the transfer of shares to a group of permitted transferees, which may not include charities; (2) limiting the number of shares that a shareholder can transfer in a certain period; and (3) granting the corporation or shareholder a right of first refusal that prevents transfers to outsiders.

18. Shares received in exchange for performance of services are taxed as compensation under IRC Section 83. The value of the shares is included in income when the shares are fully vested, but a Section 83(b) election, filed within 30 days of the grant date, can be made to include in income the value of the shares on the grant date.

19 On the formation of a start-up company, founders may: (1) contribute property in exchange for shares (a tax-free exchange under IRC Section 351); and

(2) receive shares in exchange for contribution of services. Shares received when property is contributed are capital assets. Shares received for contribution of services are usually subject to a vesting schedule, and therefore, subject to Section 83. A Section 83(b) election is routinely made to include the value of the shares (usually minimal when the company is formed) in income, and the shares convert to capital assets.

20. The tax basis of shares received from exercising nonqualified stock options is the FMV at the time of exercise because the difference between the FMV and the exercise price was included in income when the options were exercised. Treas. Regs. Section 1.83-7(a). The exercise of incentive stock options (ISOs) won’t result in income for regular income tax purposes, but the difference between the FMV and exercise price is included in income for calculating AMT. Therefore, the tax basis of shares received from the exercise of ISOs is the exercise price for regular income tax purposes and FMV for AMT. IRC Sections 421(a)(1) and 56(b)(3).

21. Capital assets held for over one year qualify as long-term capital gains property. IRC Section 1222(3).

22. The Internal Revenue Service asserted the assignment of income doctrine in Palmer v. Commissioner, 62 T.C. 684 (1974), in which stock donated to a PF was redeemed by the corporation one day following the gift. The donor had voting control of the corporation and served as trustee of the foundation. The court held that the donor contributed stock and not the proceeds of redemption because the PF wasn’t obligated to have the stock redeemed. While the donor served as trustee of the PF, there was no evidence of a breach of fiduciary duty. The IRS subsequently stated that the Palmer decision will be followed only if the donee isn’t legally bound to surrender the shares for redemption. Revenue Ruling 78-197, but see Blake v. Comm’r, 697 F.2d 473 (2d Cir. 1982) (holding gain recognition on gift of stock when there’s an advance understanding that a contribution of appreciated stock, later sold by the charity, would be used to purchase an asset from the donor, regardless of whether the understanding is legally enforceable).

23. A charitable remainder unitrust (CRUT) is one of two types of charitable remainder trusts (CRTs) permitted and defined by IRC Section 664. Under a CRUT, the non-charitable beneficiary will receive annual payments equal to a fixed percentage of the value of the trust principal (revalued annually). The second type of CRT is the charitable remainder annuity trust (CRAT). Under a CRAT, a specific dollar amount must be distributed annually to the non-charitable beneficiary. CRUTs are preferable to hold appreciating assets because the annual payments to the donor will increase as the value of the CRUT asset appreciates.

24. Section 664(d)(2)(A).

25. Section 664(d)(2)(D). The 10 percent remainder interest to charity requirement usually prevents young clients from creating CRTs that will continue for two lifetimes.

26. Section 664(b).

27. Payments to the charity may be a guaranteed annuity (a charitable lead annuity trust (CLAT)) or a fixed percentage of the FMV of the trust property determined each year (a charitable lead unitrust). CLATs are more popular because the amount going to charity is fixed. To the extent the CLAT assets appreciate at a higher rate than the IRC Section 7520 rate used to calculate the charitable gift, the appreciation is transferred to the remainder non-charitable beneficiaries free of gift tax.

28. Section 170(f)(2)(B).

29. IRC Section 4942.

30. PFs are subject to excise taxes under IRC Chapter 42 (Sections 4940 through 4948).

31. IRC Section 4966(d)(2).