Interest rates dominate charitable gift planning. In particular, high interest rates and high inflation create a bias against fixed-payment “life income” gift plans, such as the charitable remainder annuity trust (CRAT) and the charitable gift annuity (CGA). Low interest and low inflation rates, on the other hand, favor such plans, as well as the charitable lead annuity trust (CLAT). To understand all this in depth, it’s necessary to grasp basic compound interest theory and some tax law wrinkles.

Compound Interest Theory

Ben Franklin called compound interest the eighth wonder of the world.1 In the realm of U.S. tax law, which Franklin would have abhorred, compound interest theory plays a central role. The formula to figure out the compounded value of one dollar is (1 + i)n, where “i” is the assumed interest rate and “n” is the number of investment years. So, for example, if $X is invested at 8 percent compound interest for two years, at the end of two years, the $X will have grown to $X(1.08)2, or $1.17X. Present value is simply the reciprocal of compound interest.

Present value example. Suppose Ben invests $0.93 at 8 percent compound interest. At the end of Year 1, Ben has $0.93(1.08)1, which is $1 (rounded to the nearest penny). We can say that the present value of $1 to be received in one year is $0.93, assuming 8 percent interest (or an 8 percent discount rate). Note the reciprocal relationship between present value ($0.93) and compound interest ($1.081): 1/$1.081 = $0.93.

The present value of an amount of money to be received in the future is the amount of money that has to be invested today at the assumed discount rate, so as to produce the targeted amount of money on the future date.

Let’s play with this example. Suppose Ben is to receive a $1 payment at the end of two years. What’s the present value of this payment? It turns out the present value is just $0.86: 1/(1.08)2 = 0.86.

On an Excel spreadsheet, we can calculate the $0.93 figure by entering this formula in a spreadsheet cell:

=1/1.08^1,

where “^1” means 1.08 is raised to the first power. Taking 1.08 to the first power yields 1.08, so 1/1.08^1 is equal to 0.93. Likewise, one can calculate the $0.86 figure by entering this formula in a spreadsheet cell:

=1/1.08^2,

where “^2” means that 1.08 is raised to the second power; that is, 1.08 is multiplied by itself or is squared. Multiplying 1.08 by 1.08 yields 1.17, meaning 1/1.08^2 = 1/1.17 = 0.86.

Changing the discount rate. Let’s now assume a discount rate more realistic to the time this article is being written, late summer 2016. Let’s try a discount rate of

1.8 percent. Here’s how the numbers play out for Ben:

Present value of $1 to be received at the end of:

Year 1 $0.98

Year 2 $0.96

Very interesting. We see that the present value of $1 to be received in the future is considerably greater if we assume a 1.8 percent discount rate than if we assume an 8 percent discount rate. This makes perfect sense logically, because more money needs to be invested today at 1.8 percent compound interest than at 8 percent to produce $1 in the future.

The present value of annuity-type payments. We’re ready now to apply the present value concept to annuity-type payments, which I’ll represent as the payment of $X at the end of each year for a prescribed number of years. The present value of the annuity (PVA) is equal to the sum of the present value of each annuity payment. If we assume a 1.8 percent discount rate, PVA = 0.98X + 0.96X +.... If we assume an 8 percent discount rate, PVA = 0.93X + 0.86X +.... It’s no surprise that the annuity discounted at 1.8 percent has a greater present value than the annuity discounted at 8 percent.

Interest rates and inflation. Interest rates and inflation tend to go hand in hand. In the 1980s, for example, the United States experienced high inflation and high interest rates. During the 1980s, as a consequence, charitable donors established relatively few gift CGAs and CRATs. The annuity-type payments these plans made had too little present value to make them attractive to anyone who wasn’t elderly (that is, who wasn’t an individual with a relatively short future life span). Put another way, the value of annuity-type payments eroded badly in the 1980s over any except a short period of time.

Fast forward to 2016, and the situation is reversed. As of Summer 2016, the United States has been experiencing low interest rates and low inflation for some years. In this environment, annuity-type payments hold their value well and are attractive to certain charitable donors. For example, donors aged 75 or older tend to be drawn to the CGA. In some cases, very wealthy donors are drawn to the CLAT as a way to transfer wealth downstream at little or no transfer tax cost. It’s worth noting that the typically small dollar gift transaction (CGA) and the typically large dollar gift transaction (CLAT) both tend to work well in a low interest rate environment.

Tax Calculations and Interest Rates

So far, we’ve explored the present value concept purely from a financial standpoint. Now, we turn to how the tax law uses the present value concept in the realm of charitable giving.

Gift plans that involve annuity-type payments. For the three charitable gift plans that involve annuity-type payments (CRAT, CGA and CLAT), the tax law imposes a two-step calculation. First, the PVA is calculated. Second, the PVA is subtracted from the amount the donor has transferred. The difference is a gift—either to charity or to some other party. In mathematical terms, GIFT = A - PVA, where “A” is the amount transferred by the donor.

The PVA is calculated using the IRS discount rate (Internal Revenue Code Section 7520(a)).2 The IRS discount rate is based on the interest rates yielded by U.S. Treasury obligations having maturities of three to nine years. The IRS discount rate is currently 1.8 percent, which is historically quite low. In the 1970s, the IRS discount rate was a fixed 6 percent. For much of the 1980s, the discount rate was a fixed 10 percent. In 1989, when the monthly determined IRC Section 7520(a) rate was introduced, the discount rate rose to over 11 percent. In those years of relatively high discount rates, any PVA was relatively small.

A PVA, small or large, cuts two ways. Given that GIFT = A - PVA, the larger the PVA, the smaller the gift. Thus the charitable contribution (gift to charity) for creating a CRAT or a CGA is relatively small in a low interest rate environment. The smallness of the gift can be a problem with these two gift plans, as we’ll see. Yet, although a large PVA means a small charitable contribution with these two plans, a large PVA is good financially for the individual receiving the annuity-type payments. That’s how the PVA cuts two ways.

Because the PVA is relatively large in a low interest rate environment, the gift to the remainder beneficiary(ies) of a CLAT is relatively small, which is good in terms of avoiding transfer taxes. Low interest rates provide powerful tax leverage for a CLAT.

The problems of low interest rates for a CRAT or a CGA. A low IRS discount rate can pose two potential tax problems for a CRAT and CGA.

Problem 1. The charitable contribution (“GIFT” in our formulation) must be at least 10 percent of the amount transferred by the donor (“A” in our formulation).3 For example, assuming a 1.8 percent discount rate, a 55 year old can’t set up a 5 percent payout CRAT that’s to make payments to the 55 year old for life; the trust flunks the 10 percent test. Fortunately for both charities and donors, the 10 percent test tends not to be a problem, because both CRATs and CGAs are usually created by and for the benefit of much older individuals.

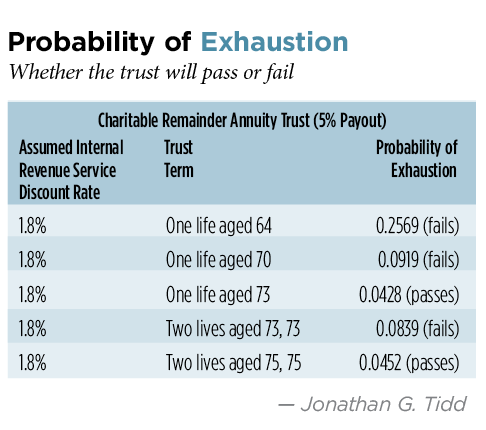

Problem 2. This problem applies only to CRATs for a life or lives. It’s a much more serious problem in a low interest rate environment. It’s the 5 percent probability test, which requires that there not be more than a 0.05 probability on the date the CRAT is created that a CRAT established for one or more lives will be exhausted before it terminates.4 Mathematical probability, by the way, is a number ranging from 0 to 1, not a percentage amount. A full description of how the probability of exhaustion is calculated is beyond the scope of this article. “Probability of Exhaustion,” this page, however, shows the probability of exhaustion for several CRAT scenarios.

There are several traditional ways to avoid the 5 percent probability test: (1) Create a CRAT for a fixed number of years, up to 20 years. Such a CRAT isn’t subject to a life contingency, and, on the day it’s created, lacks an actuarial probability of being exhausted;5 (2) Establish a CGA. CGAs aren’t subject to the 5 percent probability test, basically because they’re backed by all of the issuing organization’s assets, not merely by a trust fund that possibly may be exhausted;6 or (3) Establish a charitable remainder unitrust (CRUT). CRUTs aren’t subject to the 5 percent probability test.7 Internal Revenue Service to the rescue: On Aug. 8, 2016, the IRS issued Revenue Procedure 2016-42, which contains an optional sample CRAT provision aimed at dealing with low interest rates. If the provision is inserted into a CRAT instrument, the CRAT won’t be subject to the 5 percent probability test. Instead, the CRAT will be tested to see if making a payout would cause the CRAT to fail a new 10 percent test. If so, the CRAT will terminate the day before the payout is made. The new sample CRAT provision will function as a qualified contingency as defined in IRC Section 664(f)(1). Here’s the new sample provision for a one-life CRAT:

The first day of the annuity period shall be the date the property is transferred to the trust and the last day of the annuity period shall be the date of the Recipient’s death or, if earlier, the date of the contingent termination. The date of the contingent termination is the date immediately preceding the payment date of any annuity payment if, after making that payment, the value of the trust corpus, when multiplied by the specified discount factor, would be less than 10 percent of the value of the initial trust corpus. The specified discount factor is equal to [1 / (1 + i)]t, where “t” is the time from inception of the trust to the date of the annuity payment, expressed in years and fractions of a year, and “i” is the interest rate determined by the Internal Revenue Service for purposes of section 7520 of the Internal Revenue Code of 1986, as amended (section 7250 rate), that was used to determine the value of the charitable remainder at the inception of the trust. The section 7520 rate used to determine the value of the charitable remainder at the inception of the trust is the section 7520 rate in effect for [insert the month and year], which is [insert the applicable section 7520 rate].

Rev. Proc. 2016-42 contains other valuable information, including sample language for a two-life CRAT. This revenue procedure is required reading for all CRAT drafters. In a low interest rate environment, it allows many CRAT arrangements to pass muster that would otherwise fail up-front, including all the arrangements that fail in “Probability of Exhaustion.”

Example: Jane, age 64, sets up a $100,000, 5 percent CRAT for her life in Year 1, when the applicable IRS discount rate is 1.8 percent. Jane’s up-front charitable contribution is $24,015, which means the CRAT satisfies the 10 percent minimum charitable remainder requirement. Jane’s CRAT, however, would flunk the 5 percent probability test except that Jane’s CRAT instrument contains the new optional provision. Exactly 10 years later, the trustee is getting ready to make a $1,250 annuity distribution to Jane; at this time, the CRAT has assets of $81,250, which means if the distribution is made, the CRAT assets will be reduced to $80,000. The trustee calculates the discount factor under the new optional provision: discount factor = 1/(1 + 0.018)10 = 0.837. Multiplying $80,000 by 0.837 yields $66,929, which is far more than 10 percent of the initial trust asset value ($10,000), so the trustee can go ahead and make the annuity payment.

A ray of sunshine for CGA recipients. There’s another up-front tax calculation made for gift annuities besides the calculation of the charitable contribution. It’s the calculation of how much of each annuity payment is treated as a tax-free return of investment. For the period of life expectancy (L.E.), a portion of each annuity payment equal to PVA/L.E. is considered to be a tax-free return of investment.8 Because in a low interest rate environment, PVA is relatively large, the tax-free portion of each annuity payment for the L.E. period is relatively large.

That’s a ray of sunshine. There’s a possible rain cloud, however, which appears when the CGA is funded with appreciated stock held long term.9 The donor realizes gain equal to:

(PVA/FMV) x (FMV - B),

where “FMV” is the fair market value of the stock, and “B” is the donor’s basis in the stock.10 The amount of this gain is directly proportional to PVA, meaning that a relatively large PVA causes a relatively large amount of gain to be realized. The donor gets to spread this gain ratably over his L.E. if the donor is the only annuity recipient or is the first of two successive recipients.11 The gain is ratably reported each year and displaces a corresponding amount of tax-free return of investment, so that a large PVA doesn’t help the donor as much when the donor uses appreciated stock as when the donor uses cash to fund the annuity.12

Other Gift Plans

Plans that make a unitrust payout. There are two charitable gift plans that make a yearly unitrust payout—the CRUT and the charitable lead unitrust (CLUT).13 A CRUT may be set up to pay out whichever is less for the year, the unitrust percentage amount or CRUT net income.14 This type of CRUT is called a net-income CRUT (NICRUT).

Low interest rates have negligible effect on the present value of the remainder following a unitrust payout.15 This means low interest rates have a negligible effect on the charitable contribution made by creating a CRUT or a CLUT. The driving consideration in determining the present value of the remainder following a unitrust payout is the unitrust payout percentage; the higher the unitrust payout percentage, the higher the initial present value of the payout interest and the lower the present value of the CRUT’s remainder interest and vice versa. All this is true for NICRUTs for tax purposes, but of course, if a NICRUT earns little income due to low interest rates, the financial benefit of the NICRUT payout will be small, which may cause the recipient of a small NICRUT payout to want to relinquish his right to receive it.16

This brings us to a significant change made to the tax law in December 2015. Beginning in 2007, the IRS took the position that the value of a relinquished payout interest in a NICRUT was to be calculated using the IRS discount rate applicable at the time of relinquishment, not the NICRUT payout percentage.17 If, for example, the payout percentage was 7 percent and the applicable IRS discount rate was 2 percent, the donor’s up-front charitable contribution of the NICRUT remainder interest would have been calculated using 7 percent as the payout percentage, but the subsequent contribution of the payout interest would be calculated using the 2 percent IRS discount rate as the payout percentage. This inconsistent approach assured the value of each contribution would be low . . . arguably unfair to a donor who got a relatively small up-front charitable deduction because of the relatively high 7 percent unitrust payout percentage, and then got another relatively small charitable deduction because of a payout value based on a 2 percent IRS discount rate. Congress corrected this arguably unfair treatment in December 2015, by amending the tax law so as to require that a NICRUT payout interest that’s relinquished early be valued using the NICRUT’s stated unitrust payout percentage rate (7 percent in our example).18

Life estate arrangements. A federal income tax charitable deduction is allowed for giving to charity a remainder interest in a personal residence or farm subject to an intervening estate for life or a term of years.19 The present value of the remainder interest is determined using the IRS discount rate applicable to the gift. In a low interest rate environment, this present value is relatively large, meaning the gift arrangement plays out relatively well from a tax standpoint.

Pooled income funds. Pooled income funds (PIFs), which provide a remainder interest to charity and pay fund net income to life income beneficiaries, were popular in the 1980s, when investment grade bonds were yielding double-digit interest.20 In the current low interest rate environment, PIFs have fallen out of favor.

The problem isn’t low interest rates per se. A low IRS discount rate doesn’t have any effect whatsoever on the federal income tax charitable deduction allowed for giving to a PIF. The deduction is calculated using the fund’s highest rate of return for the past three years as the discount rate.21 A low historic rate of return produces a relatively large remainder value, which is good in terms of the donor’s charitable deduction.

The problem stems from a conservative bond/equity approach to investing that’s standard for PIFs. Given this investment approach, most PIFs pay out too little income (dividends and interest usually) to be attractive to potential donors in today’s low interest rate environment.

Endnotes

1. Natalie Turbiville, “Eighth Wonder of the World? Compound Interest and Benjamin Franklin,” Walking in Mathland (Dec. 18, 2012).

2. The calculation of the present value of the annuity (PVA) also takes into account the probability of living from one year to the next when the annuity is to be paid for a life. This probability is determined using the Internal Revenue Service mortality table, Table 2000CM.

3. For charitable remainder annuity trusts (CRATs), Internal Revenue Code Section 664(d)(1)(D) provides that the initial value of the charitable remainder must be at least 10 percent of the amount used to fund the CRAT. For charitable gift annuities (CGAs), IRC Section 514(c)(5)(A) provides the same rule.

4. The 5 percent probability test was made applicable to CRATs in Revenue Ruling 77-374. In Private Letter Ruling 9532006 (Aug. 11, 1995), the IRS ruled that a trust failing the 5 percent probability test couldn’t be a CRAT.

5. The 5 percent probability test aims at determining whether the probability that a CRAT payout recipient will live to the point of CRAT exhaustion exceeds 0.05. The test is based on Table 2000CM. This table doesn’t apply to a CRAT for a term of years, unless the CRAT is established, for example, for 20 years or a life, whichever is shorter (or longer); in which case Table 2000CM does apply to the CRAT, as does the 5 percent probability test.

6. In this regard, it’s important to grasp that a gift annuity is a contractual arrangement, not a trust arrangement.

7. In theory, a charitable remainder unitrust (CRUT) can’t be exhausted, because the unitrust payout can never exceed the value of CRUT assets on the trust valuation date. That’s mere theory, but the tax law adheres to the theory.

8. See Treasury Regulations Section 1.1011-2(b), Example (8).

9. Ibid.

10. The formula here tracks Treas. Regs. Section 1.1011-2(b), Example (8). The logic of the formula is that the donor sells the stock to the charity for a price equal to PVA (which the tax law regards as a bargain sale). The larger the PVA, the more gain realized by the donor, and the smaller the donor’s charitable contribution.

11. Treas. Regs. Section 1.1011-2(a)(4)(ii).

12. When the donor uses cash to fund a CGA, no bargain sale occurs, and therefore no gain is realized.

13. Relatively few charitable lead unitrusts (CLUTs) are established compared to charitable lead annuity trusts (CLATs). CLUTs are typically used to transfer wealth to grandchildren or other generation-skipping transfer (GST) tax skip persons. The reason is that the GST tax applicable fraction can be calculated for a CLUT when it’s created, whereas the applicable fraction for a CLAT can’t be determined until the CLAT terminates. See IRC Section 2642(e).

14. Section 664(d)(3).

15. A low IRS discount rate affects only the calculation of a CRUT’s adjusted payout rate. The unitrust payout percentage, as adjusted, is the discount rate used to calculate the present value of the charitable remainder interest. The adjustment based on the IRS discount rate is relatively minor.

16. The right to receive the payout from a charitable remainder trust is a capital asset. Relinquishment of such right is a deductible charitable contribution assuming the creator of the right didn’t contemplate relinquishing it when the trust was created. See, for example, PLR 8805024 (Feb. 5, 1988).

17. PLR 200733014 (April 26, 2007).

18. Section 664(e).

19. IRC Section 170(f)(3)(B)(i).

20. Pooled income funds are defined in IRC Section 642(c)(5).

21. Ibid.