This report is one of a series on the adjustments we make to GAAP data so we can measure shareholder value accurately. This report focuses on an adjustment we make to our calculation ofeconomic book value and our discounted cash flow model.

We’ve already broken down the adjustments we make to NOPAT and invested capital. Many of the adjustments in this third and final section deal with how adjustments to those two metrics affect how we calculate the present value of future cash flows. Some adjustments represent senior claims to equity holders that reduce shareholder value while others are assets that we expect to be accretive to shareholder value.

Adjusting GAAP data to measure shareholder value should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibility.

Preferred stock is a hybrid instrument that carries no voting rights but has a senior claim on assets and cash flows to common stock. Dividends usually must be paid out to preferred stock owners before common stock owners can receive any money. In the event of liquidation, preferred shareholders also have priority. Many preferred shares also come with an option to convert into multiple basic shares at any time, making them a potential source of dilution.

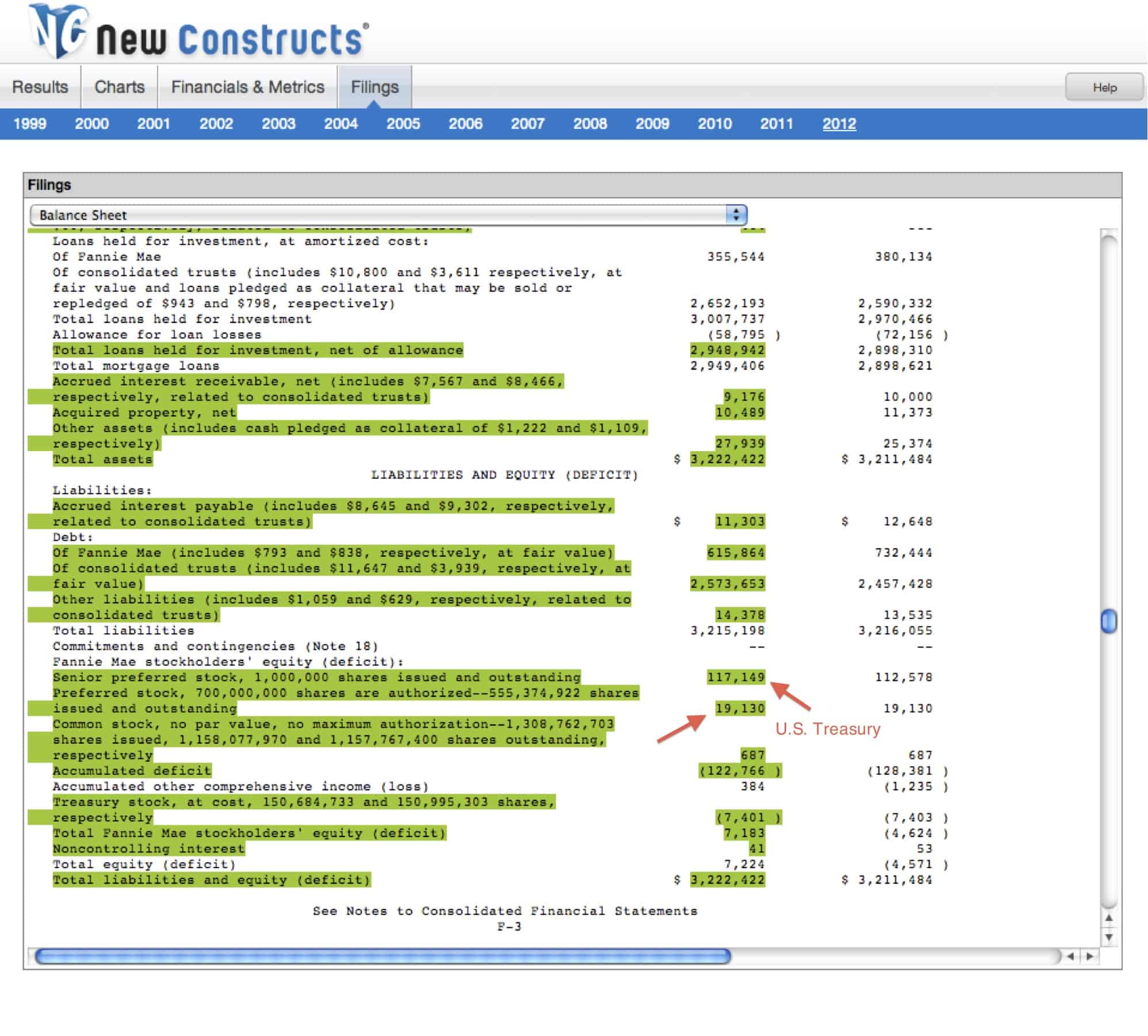

Fannie Mae (FNMA) and Freddie Mac (FMCC) have billions of dollars worth of preferred stock held by the U.S. government due to their bailout in 2008. Any common equity investment in FNMA or FMCC is purely speculative at the moment as all of their profits flow directly into the U.S. Treasury. FNMA has $136 million in preferred stock, $117 billion of which is held by the Treasury. Common shareholders have no rights to any of the profits unless the government relinquishes its preferred stock.

{kind=link}

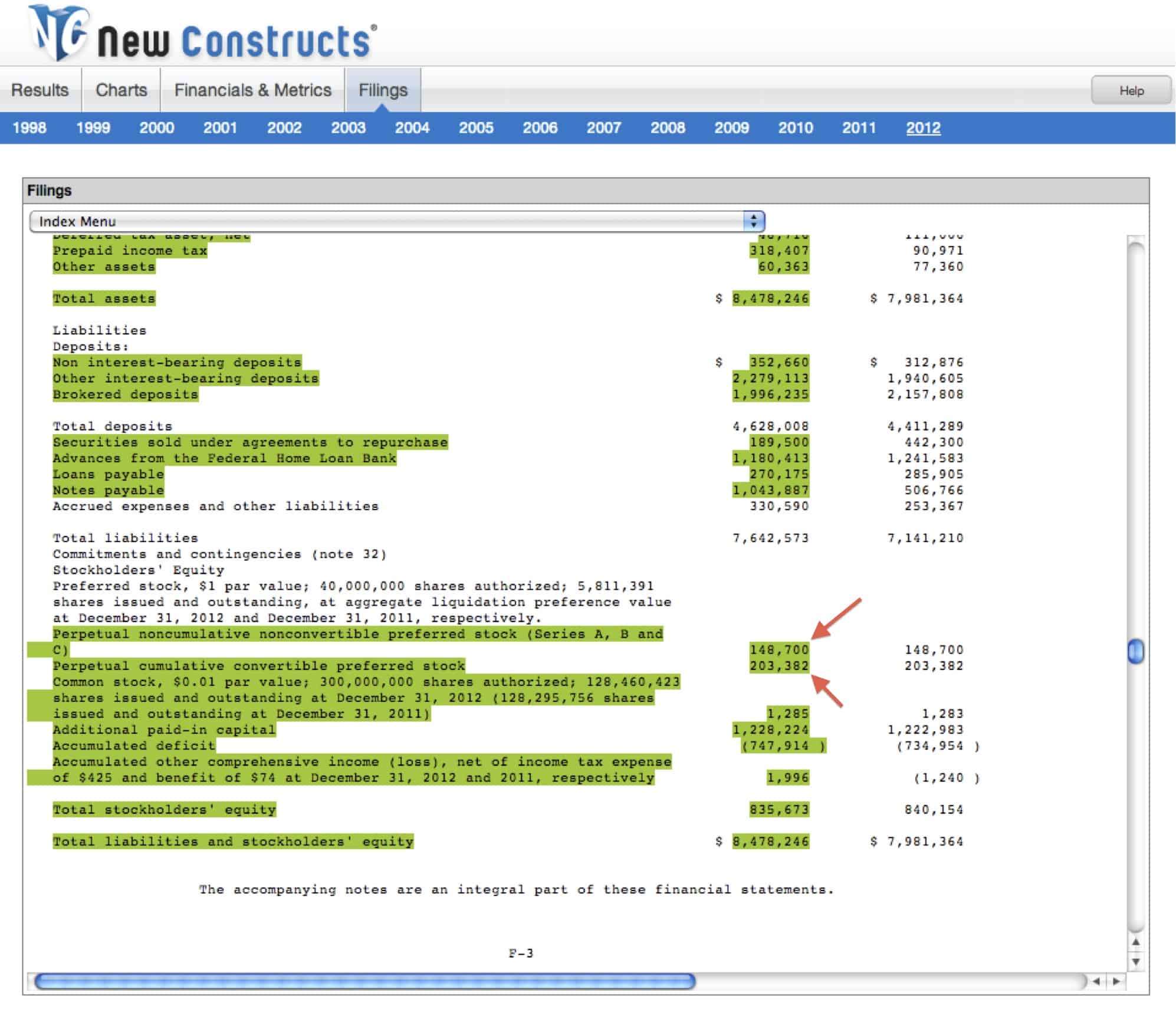

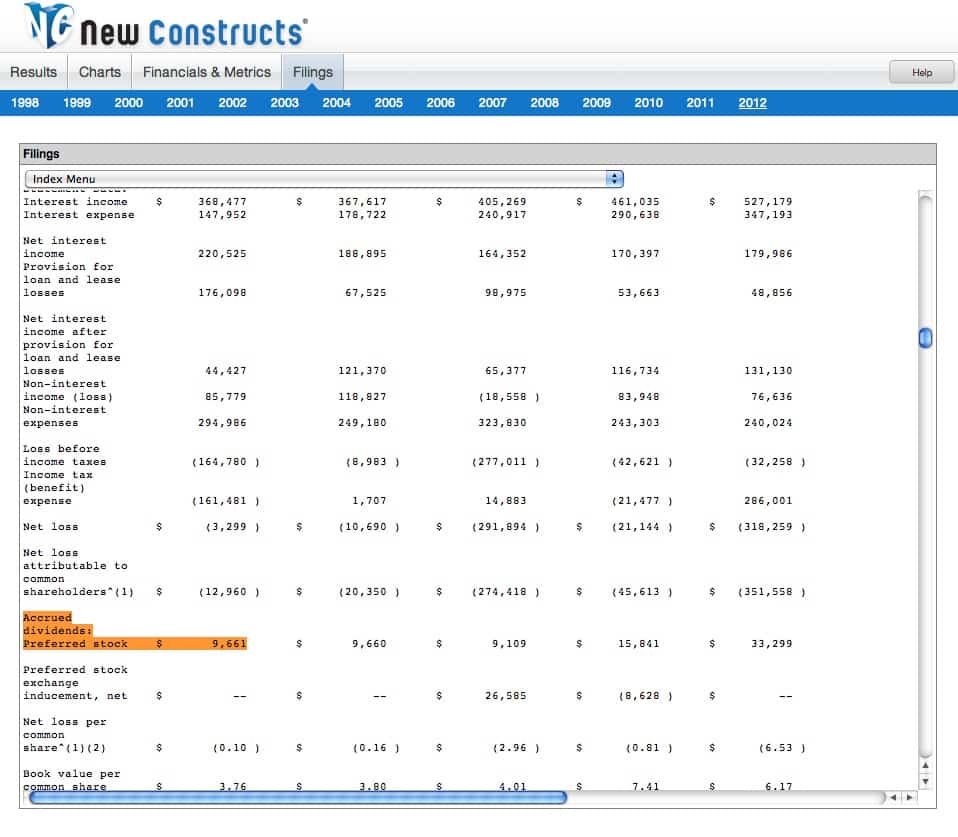

While the preferred stock issues for FNMA and FMCC are well known, other companies have less publicized liabilities related to their preferred stock. Doral Financial Corp (DRL) has $352 millionliabilities related to its preferred stock, including $10 million in unpaid dividends that need to be paid out before common stock holders can receive any money. Without careful research, investors would never know that preferred stock decreases the amount of future cash flow available to shareholders due to its senior claim.

{kind=link}

{kind=link}

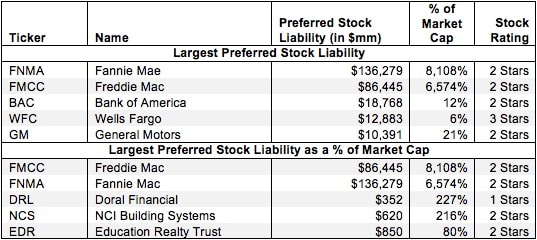

Figure 1 shows the five companies with the largest preferred stock liability removed from shareholder value in 2012 and the five companies with the largest preferred stock liability as a percent of market cap.

Figure 1: Companies With the Largest Preferred Stock Liability Removed From Shareholder Value

Sources: New Constructs, LLC. Excludes companies with market caps under $100 million.

Sources: New Constructs, LLC. Excludes companies with market caps under $100 million.

Financial companies make up over half of Figure 1. They are far from the only companies affected by preferred stock, though. Our database currently contains $354 billion in preferred stock liabilities affecting 330 companies.

Since preferred stock decreases the amount of cash available to be returned to shareholders, companies with significant preferred stock will have a meaningfully lower economic book valuewhen this adjustment is applied. For instance, NCI Building Systems (NCS) has $620 million in liabilities due to its preferred stock. Without removing this liability from shareholder value, NCS would have a zero-growth (economic book) value just above 0. After the adjustment is applied, NCS’s economic book value declines to -$615 million, which means that the company needs to significantly grow profits before it has any value to owners of its common stock.

{kind=link}

Investors who ignore preferred stock are not getting a true picture of the cash available to be returned to shareholders. By removing preferred stock liabilities, one can get a truer picture of the value of the stock for shareholders. Diligence pays.

Sam McBride and contributed to this report.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.