This report is one of a series on the adjustments we make to GAAP data so we can measure shareholder value accurately. This report focuses on an adjustment we make to our calculation ofeconomic book value and our discounted cash flow model.

We’ve already broken down the adjustments we make to NOPAT and invested capital. Many of the adjustments in this third and final section deal with how adjustments to those two metrics affect how we calculate the present value of future cash flows. Some adjustments represent senior claims to equity holders that reduce shareholder value while others are assets that we expect to be accretive to shareholder value.

Adjusting GAAP data to measure shareholder value should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

We’ve already covered how employee stock options are a compensation expense and how GAAP standards required companies to record that expense starting in 2006. Employee stock options (ESO) don’t just affect the current profitability of a company, though. They also represent a liability based on future share dilution as employees exercise their options and add to the total number of shares outstanding. Using the Black-Scholes model, we account for the fair value of all outstanding employee stock options and subtract this value from the present value of future cash flows in our discounted cash flow model and economic book value calculation.

Companies with rapid appreciation in their stock prices can be especially susceptible to having high outstanding ESO liabilities as options granted at a cheap price quickly become much more valuable. Tesla Motors (TSLA) is a good example. Buoyed in the first quarter of 2013 by its first-ever reported profit and a short squeeze, the stock is up over 350% this year. Unfortunately for current equity investors, TSLA has over 25 million options outstanding as of December 31, 2012. Using the current stock price as well as key inputs provided by the company (e.g. stock price volatility, risk-free rate etc.), we calculate the value of the liability of outstanding ESOs to be over $2.9 billion, or nearly 20% of the market cap.

Without careful footnotes research, investors would never know that employee stock options decrease the amount of future cash flow available to shareholders by diluting the value of existing shares.

Figure 1 shows the five companies with the largest outstanding employee stock option liability removed from shareholder value as of August 6, 2013 and the five companies with the largest outstanding ESO liability as a percent of market cap.

Figure 1: Companies With the Largest Outstanding ESO Removed From Shareholder Value

Sources: New Constructs, LLC and company filings. Excludes stocks with market caps under $100 million and PAMT due to pending merger.

Many high tech companies find their way onto Figure 1. However, they are far from the only companies that are affected by employee stock options. Our database shows 2,652 companies with combined outstanding ESO of over $200 billion as of August 7, 2013.

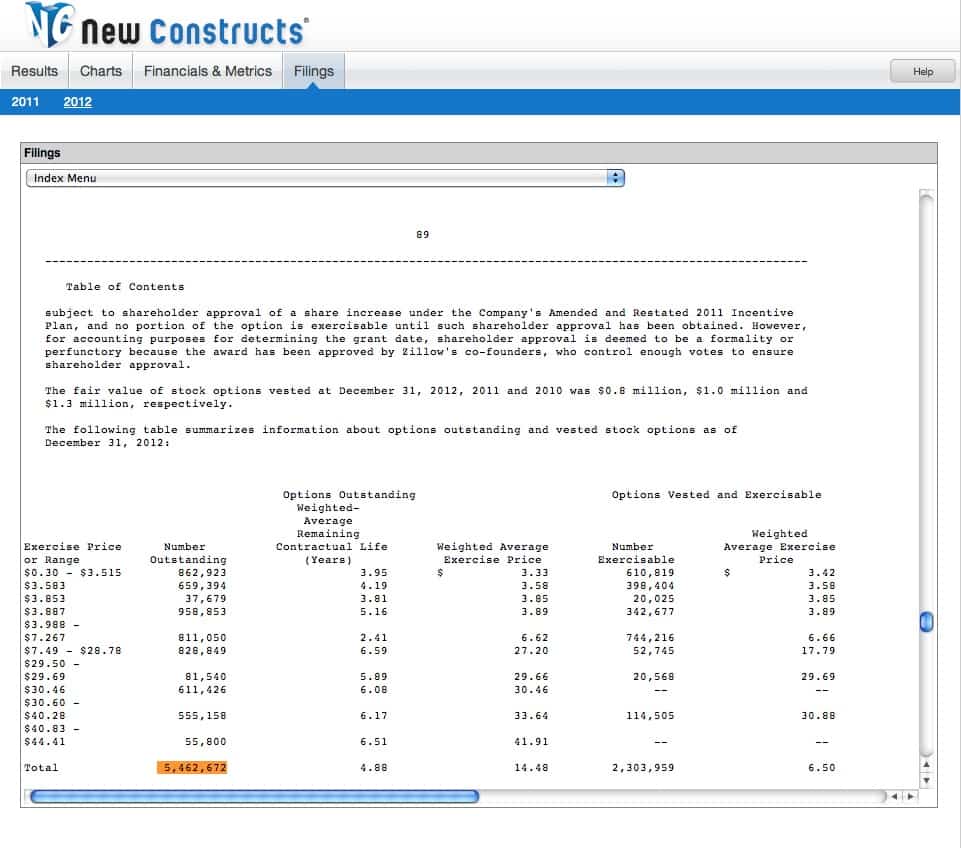

Since outstanding ESO decreases the amount of cash available to be returned to shareholders, companies with significant ESO will have a meaningfully lower economic book value when this adjustment is applied. Real estate website Zillow (Z) had nearly 5.5 million outstanding ESO’s at the end of 2012, which we currently value at $418 million. Without subtracting that $418 million liability, Z would have an economic book value per share of ~$8 instead of its true economic book value per share of around -$4.

{kind=link}

Investors who ignore outstanding employee stock options are not getting a true picture of the cash available to be returned to shareholders. By subtracting the value of outstanding ESO, one can get a truer picture of the value that the company can create for shareholders. Diligence pays.

Sam McBride contributed to this report.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.