This report is one of a series on the adjustments we make to GAAP data so we can measure shareholder value accurately. This report focuses on an adjustment we make to our calculation ofeconomic book value and our discounted cash flow model.

We’ve already broken down the adjustments we make to NOPAT and invested capital. Many of the adjustments in this third and final section deal with how adjustments to those two metrics affect how we calculate the present value of future cash flows. Some adjustments represent senior claims to equity holders that reduce shareholder value while others are assets that we expect to be accretive to shareholder value.

Adjusting GAAP data to measure shareholder value should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibility.

Minority interests (or non-controlling interests) are a significant but non-controlling ownership of a company’s voting shares. The portion of the parent company’s income attributed to the minority interests is subtracted from reported profits, i.e. the minority interest expense. The parent company’s balance sheet will also show a liability for the minority interest.

We subtract the fair value of the minority interest liability from shareholder value in our DCF model as the minority interest shareholders have the rights to that portion of the cash flows. Without careful research, investors would never know that these minority interest liabilities distort GAAP numbers.

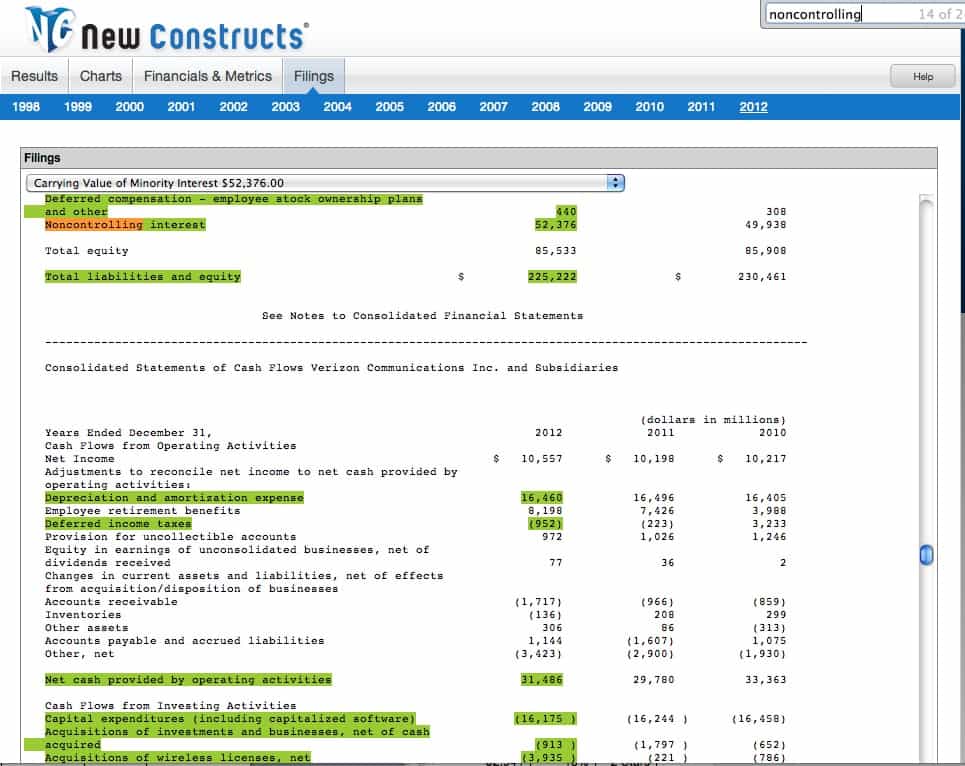

For example, Verizon (VZ) has over $130 billion in minority interest ownership, mostly due to its partnership with Vodafone (VOD), which owns a 45% stake in VZ’s wireless communication business. While the carrying value of VZ’s non-controlling interests is only $52 billion, we use information from the footnotes to calculate the fair value of this equity from 2000, which is now $130 billion. The removal of this amount from our economic book value calculation gives VZ an economic book value of ~$51/share as opposed to its unadjusted value of ~$97/share.

{kind=link}

Figure 1 shows the five companies with the larges (gross value and as a % of market value) minority interest liability adjusted out of shareholder value for 2012. Whenever it is disclosed in the footnotes, we subtract the fair value of minority interests instead of the reported value for a more accurate measure of shareholder value.

Figure 1: Companies Most Affected By Minority Interest Liability

Sources: New Constructs, LLC and company filings. Excludes stocks with market caps under $100 million.

Sources: New Constructs, LLC and company filings. Excludes stocks with market caps under $100 million.

However, these companies are far from the only ones affected by minority interests. In the last fiscal year, deduction of minority interest liabilities from shareholder value occurred for 2,671 different companies for a total gross adjustment value of over $337 billion.

Since minority interest liabilities decrease the amount of cash available to be returned to shareholders, companies with significant minority interest liabilities will have a meaningfully lower economic book value when this adjustment is applied. Case in point: Kinder Morgan (KMI), which had a total of $10 billion in minority interest liability removed from shareholder value in 2012. This adjustment lowered KMI’s economic book value from $1.6 billion to -$8.6 billion. Its economic book value or no-growth value per share also dropped from ~$2/share to a negative ~$8/share.

{kind=link}

When investors ignore these often-significant minority interests, like in the case of KMI, they are not getting the full picture of a company’s cash available to be returned to shareholders. By adjusting for minority interest liabilities, one can better understand the value of the stock to shareholders.

André Rouillard contributed to this report.

Disclosure: David Trainer and André Rouillard receive no compensation to write about any specific stock, sector, or theme.