This report is one of a series on the adjustments we make to convert GAAP data to economic earnings. This report focuses on an adjustment we make to convert the reported balance sheet assets into invested capital.

Reported assets don’t tell the whole story of the capital invested in a business. Accounting rulesprovide numerous loopholes that companies can exploit to hide balance sheet issues and obscure the true amount of capital invested in a business.

Converting GAAP data into economic earnings should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

We’ve performed unrivalled due diligence on 5,500 10-Ks every year for the past decade.

Companies require a certain amount of cash on hand to pay bills, buy raw materials, pay employees, etc. Investors should demand a return on the “required cash” for use in operations. Cash that is not required for operations is excess cash.

For most companies, we estimate the amount of required cash to be 5% of sales. We increase this amount for companies with large operating losses and decrease it for companies with large operating profits to better reflect the cash needs of those companies.

Most companies hold some cash—or cash equivalents in the form of investments—above this required amount. Companies hold excess cash in order to cushion against economic downturns, prepare for acquisitions, or any number of other reasons. Sometimes, past profits pile up on balance sheets and are a form of excess cash. Excess cash is not needed for the operations of a company. It is removed from our calculation of invested capital because it is not part of the investment required for a company to grow its business. We want our calculation of return on invested capital (ROIC) to reflect the operations of the business and not be distorted by past profits.

Google (GOOG) has $49.6 billion in cash and investments on its balance sheet. Since GOOG is an extremely profitable company, we estimate that it only needs 2% of its revenues in cash, about $971 million. The remaining $48.6 billion is classified as excess cash and removed from invested capital.

{kind=link}

Cash and equivalents are listed on the balance sheet. However, investors still need to calculate the amount of required cash to understand the true amount of capital a company uses to generate returns.

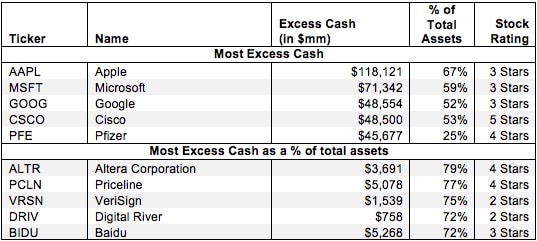

Figure 1 shows the five companies with the most excess cash removed from invested capital in 2012 and the five companies with the most excess cash as a percent of total assets.

Figure 1: Companies With the Most Excess Cash Added Back to Invested Capital

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

Figure 1 contains mostly tech companies that have very high ROICs and, therefore, high historical profits. However, they are far from the only companies that are affected by excess cash. In 2012 alone, we found 1,685 companies with nearly $1.4 trillion in excess cash. Over the history of our coverage we have found almost $9.9 trillion in excess cash in 17,554 annual filings.

Since removing excess cash decreases invested capital, companies with significant excess cash will have a meaningfully higher return on invested capital (ROIC) when this adjustment is applied. Our models assume that excess cash is available to be returned to shareholders in the form of dividends or share buybacks. High levels of excess cash are usually nice to see. However, these is risk that excess cash burns a hole in management’s pocket and leads to unwise investments or acquisitions.

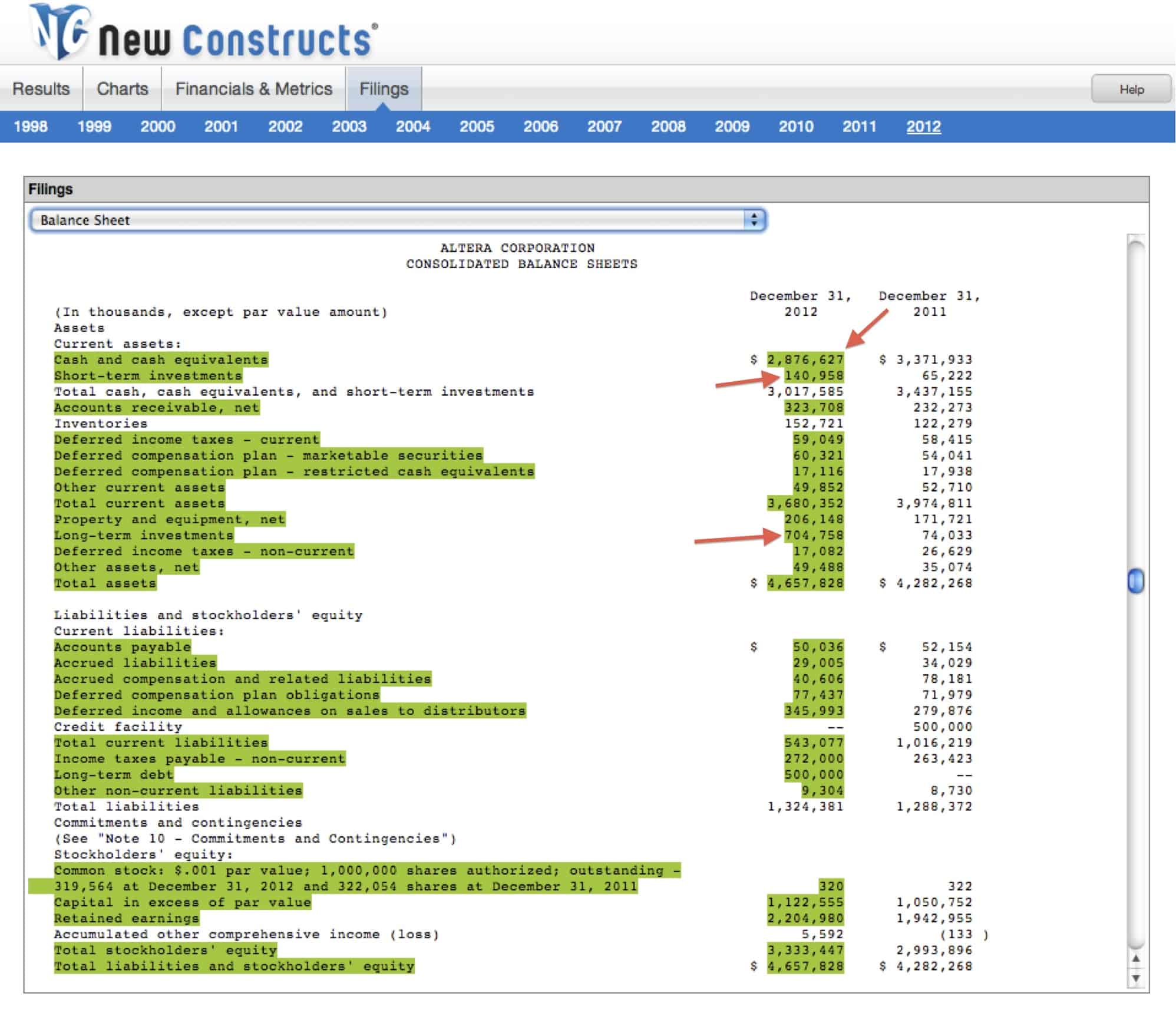

Altera Corporation (ALTR) earns our Attractive rating. ALTR has $3.7 billion in cash and investments. ALTR only requires 2% of its revenue, $36 million, in cash. Without removing the remainder of the cash from invested capital, ALTR would have an ROIC of 14%. Adjusting excess cash out of invested capital increases ALTR’s ROIC to an impressive162%.

{kind=link}

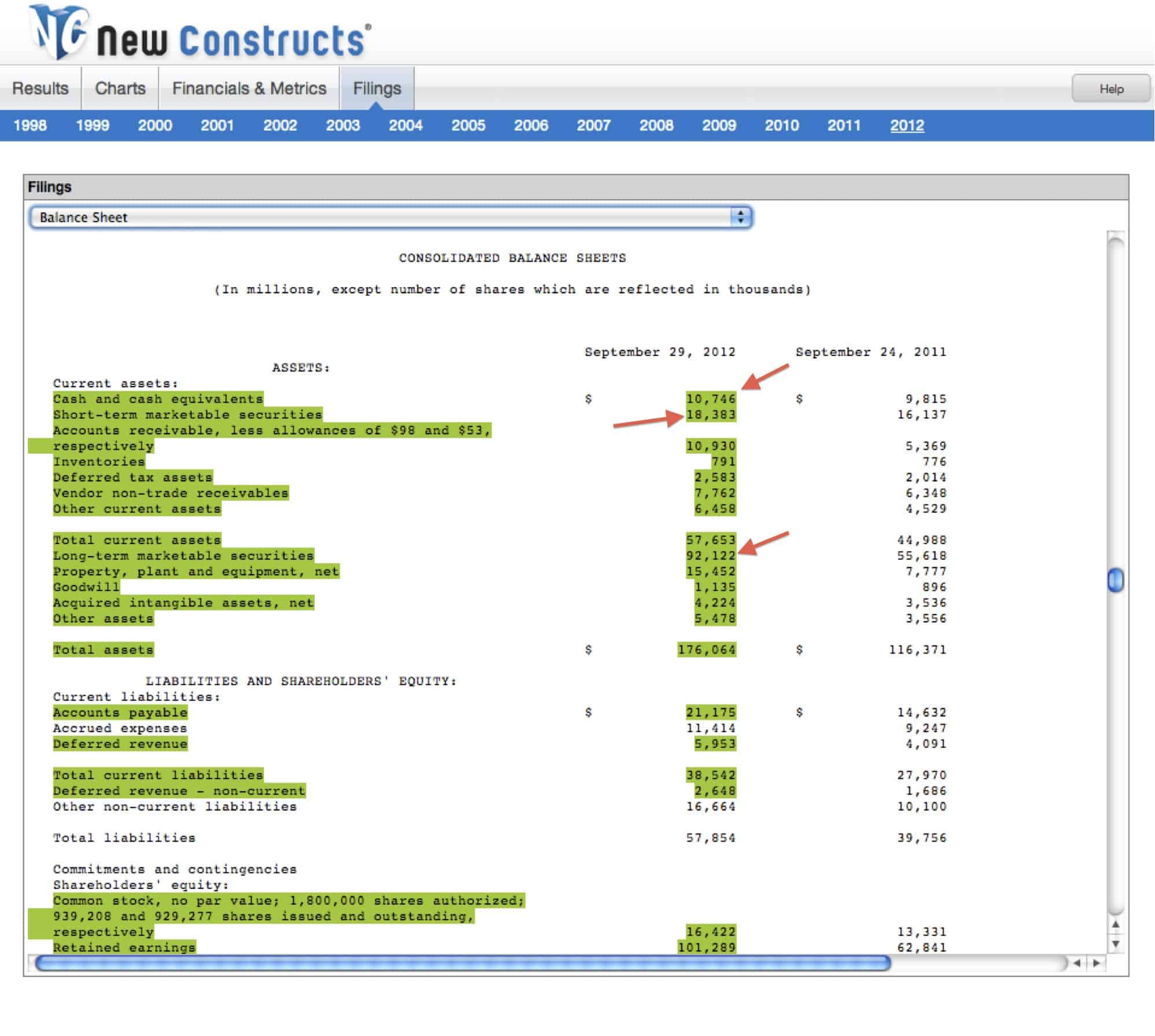

While excess cash can be a good thing for a company, it can also signal a lack of productive growth opportunities in which a company can invest. I wrote an article on Apple (AAPL) back in May highlighting the danger in the stock as its sky-high ROIC of 271% comes back to earth. AAPL’s $118 billion and growing stockpile of excess cash, along with its declining ROIC, suggests that the company lacks avenues for expansion and growth. Removing excess cash from Apple’s invested capital reveals how high its current returns are and how unlikely it is to continue raking in such massive profits.

{kind=link}

Investors who ignore excess cash are holding companies accountable for capital that is not being used to generate operating revenue. By removing excess cash, one can get a truer picture of the value that management is creating for shareholders. Diligence pays.

Sam McBride contributed to this report.

Disclosure: David Trainer owns MSFT. David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.