This report is one of a series on the adjustments we make to convert GAAP data to economic earnings.

Reported earnings don’t tell the whole story of a company’s profits. They are based on accountingrules designed for debt investors, not equity investors, and are manipulated by companies to manage earnings. Only economic earnings provide a complete and unadulterated measure of profitability.

Converting GAAP data into economic earnings should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

We’ve performed unrivalled due diligence on 5,500 10-Ks every year for the past decade.

Employee stock option expense and goodwill amortization adjustments are two adjustments that impact past years in our model but no longer have an impact due to changes in accounting standards. The Financial Accounting Standards Board (FASB) ended the practice of goodwill amortization in 2002 and required businesses to record expenses related to employee stock options beginning in 2006.

Employee stock option (ESO) expense is the cost of the issuing (at-the-money) stock options. Prior to 2006, businesses were not required to record any cost for issuing ESOs. During that time, many companies exploited that loophole to overstate reported earnings by compensating employees with ESOs.

Using data provided only in footnotes, we determined the cost of all ESO issuances long before FASB required companies to report them in 2006. This adjustment is important not only for getting a true view a company’s profits versus other firms but also for comparability of profits before and after 2006.

Goodwill amortization is a gradual, formulaic reduction in asset value using any of the several GAAP amortization methods. In 2002, this system was done away with and replaced with the practice of goodwill impairment, which calculates any depreciation in the value of an asset based on performance tests. We account for the use of amortization expense prior to 2002 by adding the charge back to net income to determine NOPAT. Synergies should never depreciate, so goodwill amortization is not a true operating cost. In addition, this adjustment enables comparability between companies with different amortization methods or that have no goodwill amortization because they used the now defunct Pooling Method of accounting for an acquisition.

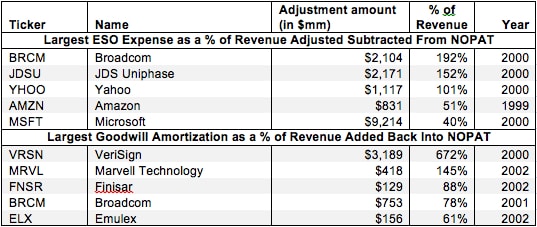

Figure 1 shows the five companies with the largest ESO expense as a % of revenue deducted from NOPAT and the five companies with the largest goodwill amortization expense as a % of revenue adjusted out of NOPAT.

Figure 1: Companies Most Affected By Employee Stock Options and Goodwill Amortization

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

Note: Results exclude companies with revenues under $1 billion for ESOs and less than $100 million for goodwill amortization.

Unsurprisingly, tech companies make up the top five companies for ESO expense as a percent of revenue. Stock-based compensation has long been a favorite practice of Silicon Valley, and tech companies were vocal in their resistance to FASB’s efforts to mandate the expensing of ESO.[1]Former FASB chairman Robert Herz (who we interviewed last month) has an interesting chapter about the controversy over ESO expensing standards in his recent book Accounting Changes: Chronicles of Convergence, Crisis, and Complexity in Financial Reporting.

Before expensing was mandated, employee stock options were widely used to help companies record artificially higher earnings. The practice declined after 2006 when companies could no longer hide that expense from investors. In 2012, BRCM recorded an employee stock option expense of only $543, less than 7% of revenues.

You are not alone if you are surprised by the huge amounts of unreported ESO expense that took place during the tech bubble. I don’t think I am reaching when I say that overstated EPS helped fuel the tech bubble. These numbers also show how doing proper diligence in the footnotes can help prevent the major losses so many investors experienced during the tech bubble. Of the five companies in the top half of figure 1, four saw their stocks fall by over 90% when the tech bubble burst (MSFT being the lone exception).

Lastly, Figure 1 shows how important it is to pay close attention to accounting rules so that you are aware of the true economic earnings of businesses and not surprised by accounting loopholes after the stocks have blown up.

However, tech companies are far from the only ones affected by ESO expenses. In our database, ESO expense adjustments to NOPAT occurred 14,493 times a total of $398 billion in adjustments. Likewise, goodwill amortization affected many more companies than the ones in the bottom half of Figure 1. We recorded 668 adjustments totaling $26 billion for goodwill amortization between 1996 and 2001.

Hidden employee stock option expense can make a company appear significantly more profitable than it really is. The 608 million employee stock options granted by Microsoft (MSFT) in 2000 gave it an estimated ESO expense of over $9.2 billion (Note on that link how few options Microsoft granted once it became clear they would have to start recording that expense). Microsoft recorded a GAAP net income of $9.4 billion in 2000, but accounting for ESO expense helped to reveal its true NOPAT of only $1.2 billion.

On the flipside, significant amortization of goodwill can reduce a company’s reported earnings significantly. Emulex (ELX) amortized $156 million of goodwill related to its acquisition of Giganet in 2002. The company was forced to record this as an expense, causing it to report -$48 million in GAAP net income. Adding back that amortization (which is not truly an expense) helped bring ELX’s NOPAT up to $24 million.

{kind=link}

Even though ELX’s NOPAT in 2002 and 2003 was fairly similar, investors just looking at reported earnings would have seen a huge difference due to the fact that ELX didn’t have to amortize goodwill in 2003.

Accounting rules are always changing. Currently, FASB is considering a standard that would force companies to account for operating leases on the balance sheet (an adjustment we already make). When assets and income can be changed with the stroke of a pen, investors need to dig deeper to truly understand the profitability of a company. Diligence pays.

André Rouillard and Sam McBride contributed to this report

Disclosure: David Trainer owns MSFT. David Trainer, Sam McBride and André Rouillard receive no compensation to write about any specific stock, sector, or theme.

[1] Herz, Robert. Accounting Changes: Chronicles of Convergence, Crisis, and Complexity in Financial Reporting. Durham, NC: American Institute of Certified Public Accountants, 2013. p. 64