This report is one of a series on the adjustments we make to GAAP data so we can measure shareholder value accurately. This report focuses on an adjustment we make to our calculation ofeconomic book value and our discounted cash flow model.

We’ve already broken down the adjustments we make to NOPAT and invested capital. Many of the adjustments in this third and final section deal with how adjustments to those two metrics affect how we calculate the present value of future cash flows. Some adjustments represent senior claims to equity holders that reduce shareholder value while others are assets that we expect to be accretive to shareholder value.

Adjusting GAAP data to measure shareholder value should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

Companies and employees will sometimes agree to defer compensation until a later date. The company then holds assets in trust to pay out later to their employees. However, there is no requirement for the amount of assets held in trust to be equal to the value of future obligations. Often, companies will have a significant difference between assets and liabilities in their deferred compensation plans.

We discussed the treatment of deferred compensation plans for invested capital in a previous report.

The net amount of deferred compensation is included in shareholder value. If assets are greater than liabilities, we add the net asset to shareholder value. If the liabilities are greater than the assets, we remove the net liability from shareholder value. If a company has a net liability, future cash flows will be diverted to pay for that obligation. If a company has a net asset, then any future increases in the obligation will not need to be met with new contributions from the company. Instead, the company can return that cash to shareholders.

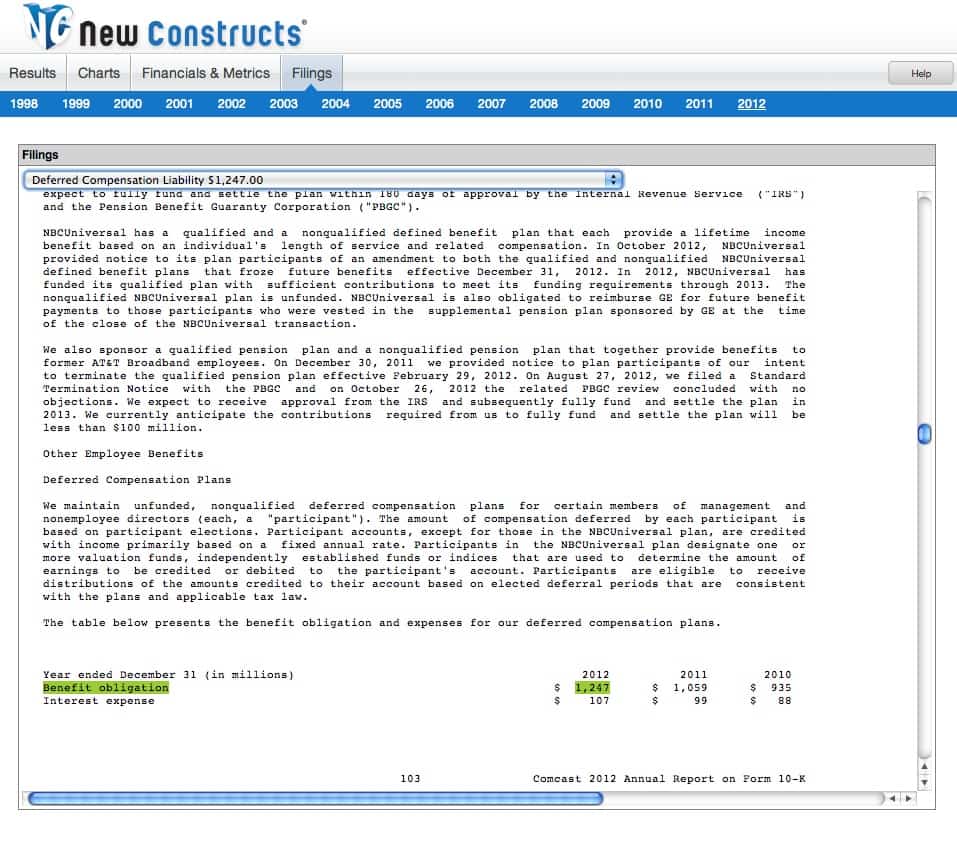

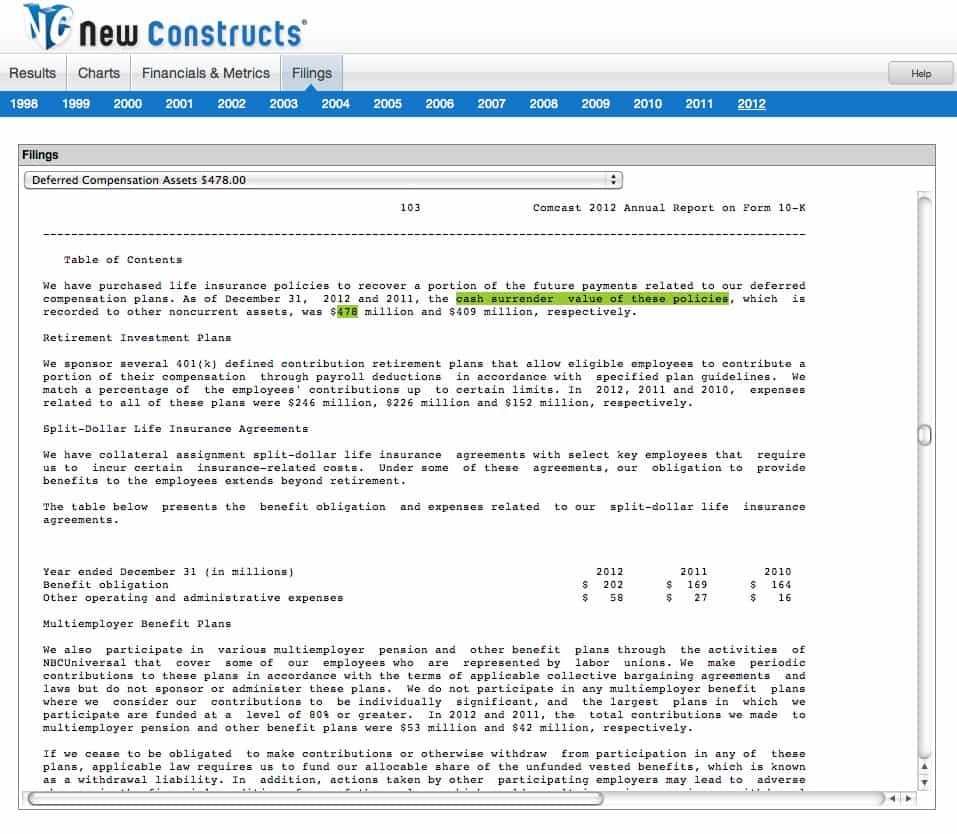

Comcast (CMCSA) has $1.25 billion in benefit obligations from its deferred compensation plans but only $478 million in assets in those plans. The $769 million gap will need to be made up by future cash flows, which means less money making its way to shareholders.

{kind=link}

{kind=link}

Without careful footnotes research, investors would never know that deferred compensation plans can increase/decrease the amount of future cash flow available to shareholders due to over or under funding

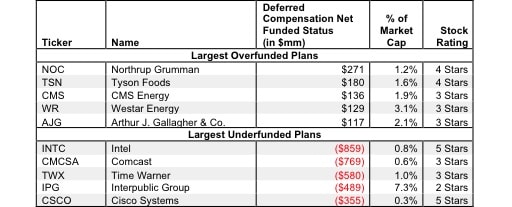

Figure 1 shows the five companies with the largest overfunded deferred compensation plans added to from shareholder value in 2012 and the five companies with the largest underfunded plans.

Figure 1: Companies With the Most Over/Under Funded Deferred Compensation Plans

Sources: New Constructs, LLC and company filings

The ten companies in Figure 1 are far from the only companies that are affected by deferred compensation plans. In 2012 alone, we found 122 companies with overfunded plans totaling nearly $3 billion and 239 companies with underfunded plans totaling over $7 billion.

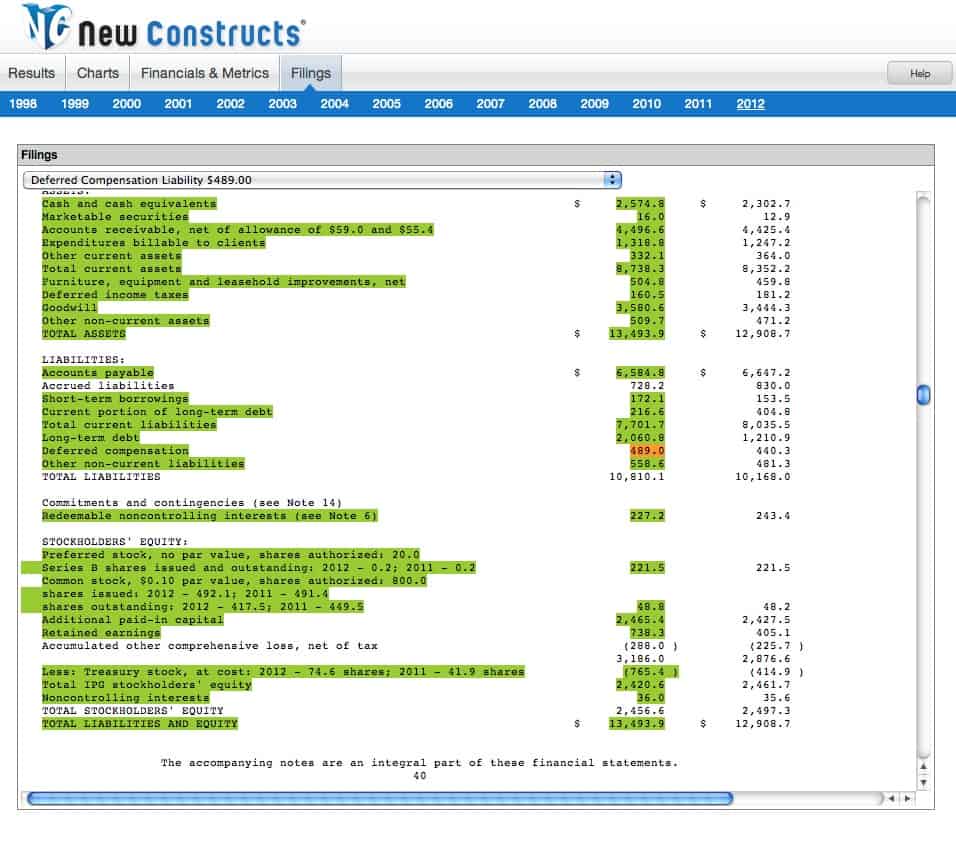

Since removing deferred compensation liabilities reduces shareholder value, companies with underfunded deferred compensation plans will look less valuable after this adjustment is applied. For instance, Interpublic Group (IPG) records a $489 million deferred compensation liability on its balance sheet. Without adjusting for this liability in its deferred compensation plan, IPG would appear to have a market-implied growth appreciation period (GAP) of 42 years. After that $489 million is removed, we see that the company has 58 years of growth embedded in its stock price.

{kind=link}

Investors who ignore deferred compensation plans are not getting a true picture of the cash available to be returned to shareholders. Diligence pays.

Sam McBride and contributed to this report.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.