This report is one of a series on the adjustments we make to convert GAAP data to economic earnings. This report focuses on an adjustment we make to convert the reported balance sheet assets into invested capital.

Reported assets don’t tell the whole story of the capital invested in a business. Accounting rulesprovide numerous loopholes that companies can exploit to hide balance sheet issues and obscure the true amount of capital invested in a business.

Converting GAAP data into economic earnings should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

We’ve performed unrivalled due diligence on 5,500 10-Ks every year for the past decade.

Deferred compensation plans delay employee compensation until a later date. The assets held for these plans are used to compensate employees in the future, not to generate profits for the company. As such, they should not be factored into the calculation of a company’s return on invested capital (ROIC).

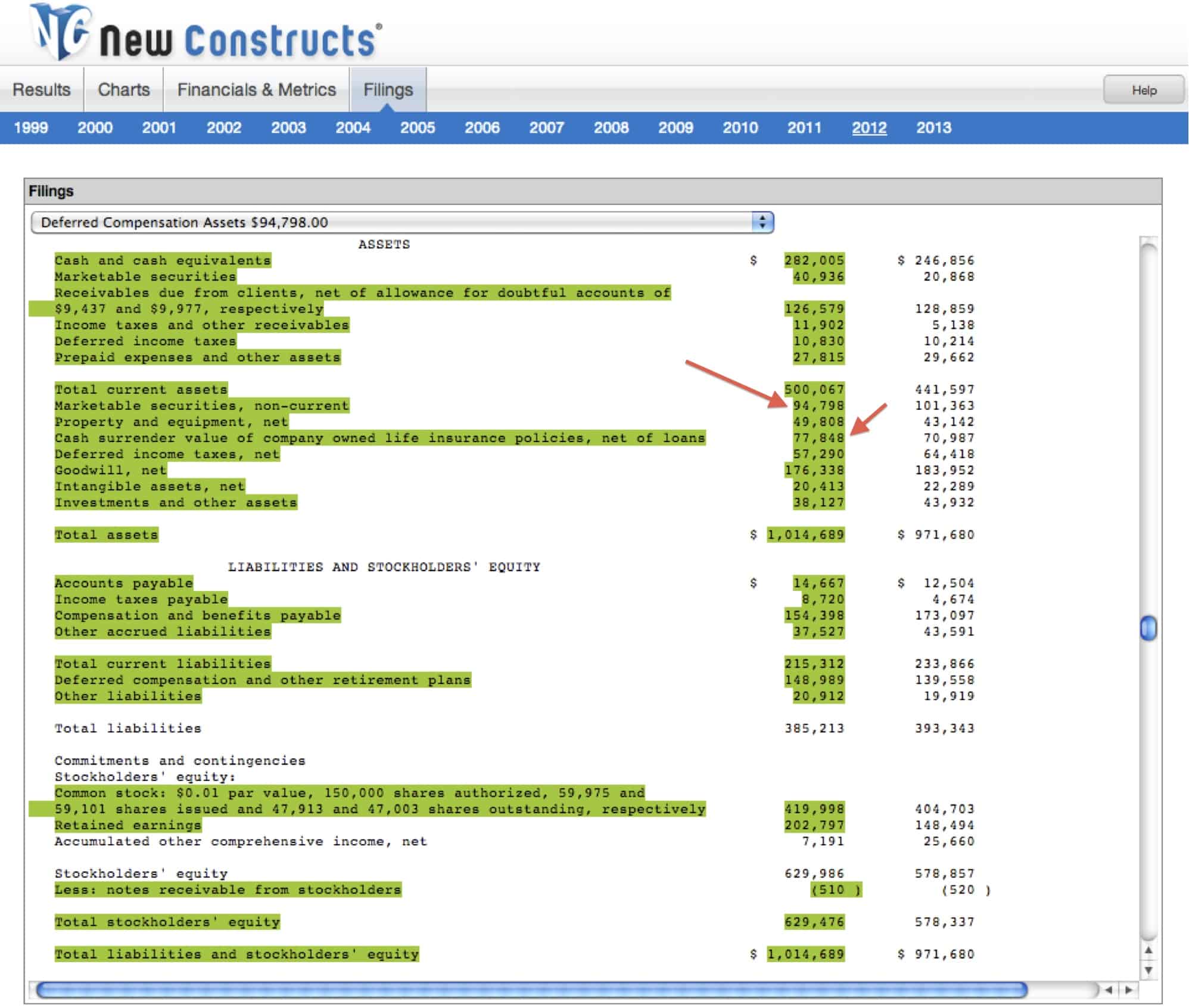

Sometimes, companies declare their deferred compensation assets directly on the balance sheet. Korn/Ferry International (KFY) lists the assets to fund its deferred compensation plan under “Marketable securities, non-current” and “Cash surrender value of company owned life insurance policies, net of loans” on its consolidated balance sheet.

{kind=link}

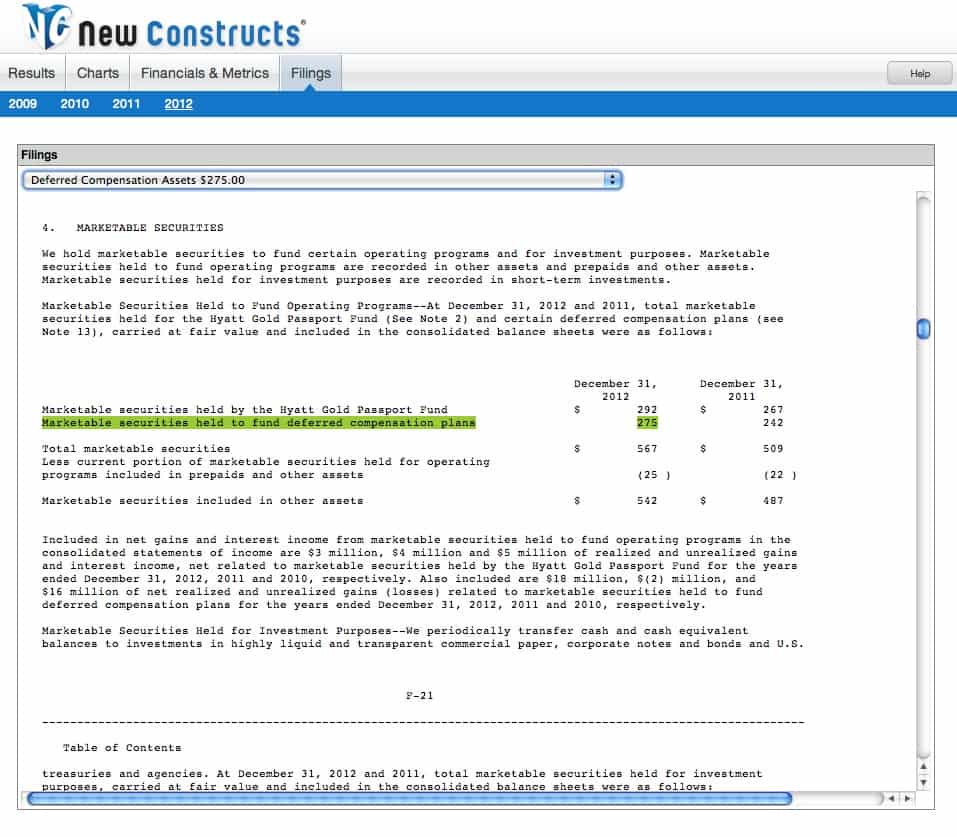

In other cases, discovering deferred compensation assets can be much more difficult. Without looking in the footnotes, investors would never know that Hyatt Hotels (H) has $275 million in securities to fund its deferred compensation plan. On the balance sheet, these securities are unmarked and bundled in the line item “Other Assets”.

{kind=link}

For companies like KFY, finding the value of deferred compensation assets simply requires an understanding of what the items on the balance sheet mean. For companies like H, the process is more complicated. Without careful footnotes research, investors in H would never know that total assets include a significant portion of non-operating assets in deferred compensation plans.

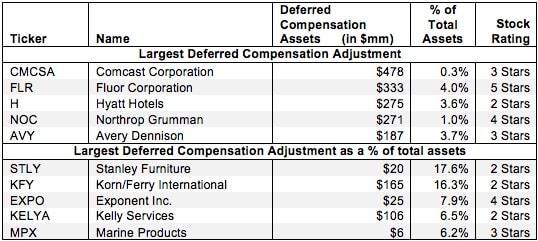

Figure 1 shows the five companies with the most deferred compensation assets removed frominvested capital in 2012 and the five companies with the most deferred compensation assets as a percent of total assets.

Figure 1: Companies With the Largest Deferred Compensation Assets Removed From Invested Capital

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

As one would expect, the companies in Figure 1 come largely from labor-intensive industries like retail and service. These companies are far from the only companies that are affected by deferred compensation. In 2012 alone, we found 212 companies with deferred compensation assets totaling over $7 billion.

Since removing deferred compensation assets decreases invested capital, companies with significant deferred compensation assets will have a meaningfully higher return on invested capital (ROIC) when this adjustment is applied. For instance, Fluor Corporation (FLR) has $333 million in deferred compensation assets clearly broken out under “Deferred Compensation Trusts” on its consolidated balance sheet. Removing these assets from invested capital increases FLR’s ROIC from 26% to 32%.

{kind=link}

Investors who ignore assets used to fund deferred compensation plans are holding companies accountable for capital that is not used to generate revenue. By removing deferred compensation assets, one can get a truer picture of the value that management is creating for shareholders. Diligence pays.

Sam McBride contributed to this report.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.