Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life and MarketWatch.com.

Rite Aid (RAD) is in the Danger Zone this week. Investors and analysts have focused on the aging U.S. population, the increasing sales of higher margin generic drugs, and the many newly insured potential customers as factors creating growth potential for RAD. The stock is up over 150% this year, and David Einhorn’s Greenlight Capital recently disclosed a $70 million long position. Lost in the excitement, however, are some significant competitive issues and long-term liabilities that make RAD a dangerous stock at its inflated valuation.

Small Fish in a Big Pond

RAD competes with much larger companies like CVS Caremark (CVS), Walgreens (WAG), and Wal-Mart (WMT) in the pharmacy segment. WAG, the smallest of those three competitors, still had nearly three times the revenue of RAD last year. Scale is important to success in retail, and RAD lacks the scale of its main competitors.

Looking deeper at the numbers, RAD shows up at even more of a disadvantage. Last year, RAD earned about $300,000 in revenue per employee. CVS made nearly $600,000 for every employee. The two companies have a very similar mix of products and employ about the same percentage of part-time and full-time labor, but CVS is twice as efficient at turning that labor into sales.

The bullish case for RAD rests on growth in prescription drug sales, which make up nearly 70% of its revenue. The problem with this thesis is that RAD is not as profitable as it appears in its reported results.

Figure 1 reveals the extent of RAD’s inefficiency in recent years. Along with stagnant sales, the company has significantly been increasing asset write-downs, a sign that management is destroying value for shareholders. Over the past five years, accumulated write-downs as a percent of net assets have increased from 15% to 80%

Figure 1: Revenue and Write Downs as a Percent of Net Assets

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

If more drug companies start selling their products directly to consumers online like Pfizer (PFE) is now doing with Viagra, RAD’s sales could suffer even more.

Red Flags in the Footnotes

It’s no secret that RAD is a highly leveraged company. The carrying value of the company’s long-term debt is currently ~$5.8 billion, or 130% of total current assets. What many investors are missing, however, is the further $5.2 billion in off-balance sheet debt due to operating leases. The details on these leases are buried on page 93 of the company’s Form 10-K and are not even mentioned in its quarterly filings.

{kind=link}

The Financial Accounting Standards Board is currently considering a proposal to require companies to include the present value of lease obligations on the balance sheet as New Constructs already does. If the FASB passes this standard in early 2014 as many expect, RAD’s significant off-balance sheet debt should receive much more attention from investors and analysts.

With $11 billion in total debt, investors should have serious questions about how RAD is going to finance its future operations. With any further borrowing likely to be very expensive, there is a real possibility that RAD could be forced to issue more equity simply to stay afloat. A secondary stock offering would dilute the value of shares currently held by investors.

The executives of RAD don’t appear to have a lot of faith in the stock. So far in 2013 insiders have sold over 2 million shares of RAD stock without buying a single share. With the company’s financial situation so precarious and the stock price surging, it’s no surprise that insiders are cashing in while they have the chance.

Valuation

With its 150% gain this year, RAD’s valuation has gotten way ahead of its fundamentals. The company’s meager profits and significant debt mean that it currently has a negative economic book (zero growth) value of ~$1.25/share.

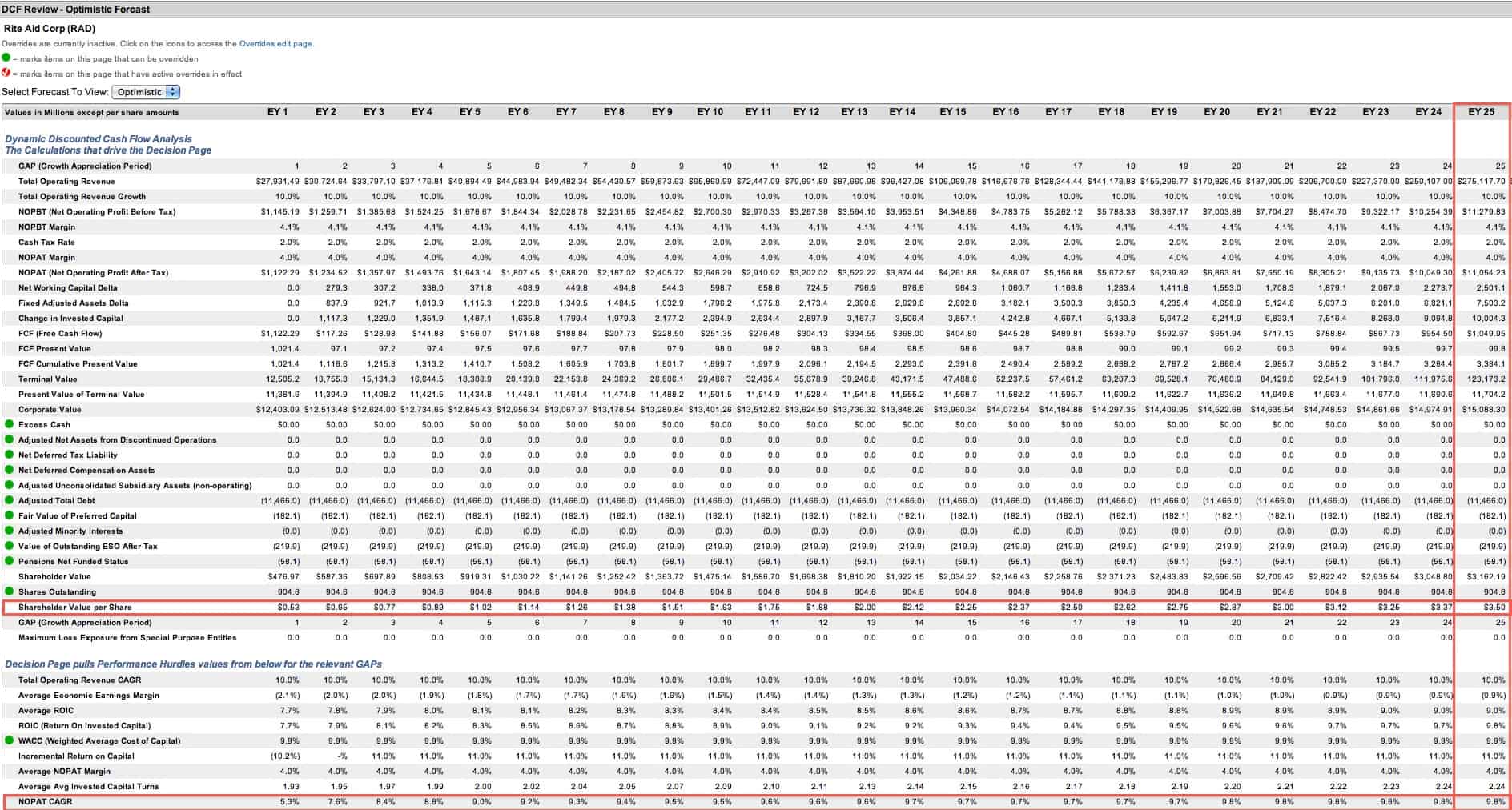

To justify its current valuation of ~$3.50/share, RAD would need to grow after-tax profit (NOPAT) by 10% compounded annually for 25 years. Even with growing prescription drug sales, that high of a growth expectation seems excessive given the company’s recent struggles.

{kind=link}

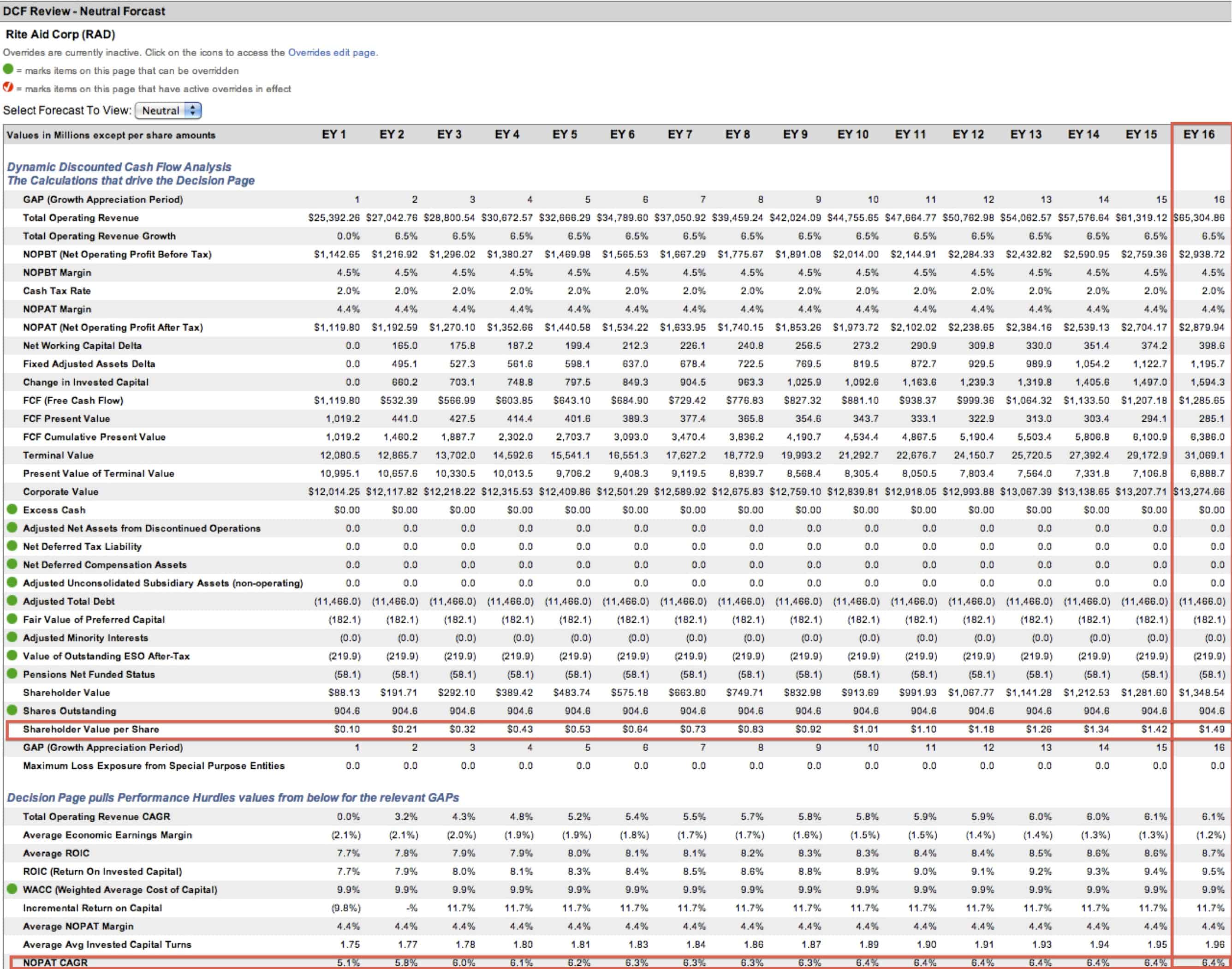

Even in a best-case scenario I see significant potential downside for this stock. With slight margin expansion and 6.5% NOPAT growth for 16 years, RAD would be worth about $1.50/share, or 60% less than its current valuation.

{kind=link}

Catalysts

There are many potential catalysts lurking out there to send RAD stock down, some of which I’ve already mentioned. The four biggest potential catalysts are:

1) Revenue and earnings growth failing to meet analyst expectations

2) The company being forced to issue more equity to fund operations

3) Increased awareness of operating lease liability due to FASB standards

4) Any change in the enforcement of the Affordable Care Act that would decrease the number of newly insured or the benefits they receive

RAD is up against the ropes right now. The company has to contend with larger, more efficient competitors, significant debt, and declining sales. Don’t be fooled by the 150% growth in the share price this year. RAD is much worse off than its stock suggests.

Avoid These Funds

Investors should avoid the following ETFs and mutual funds due to their significant allocation to RAD and Dangerous-or-worse rating.

1) Oceanstone Fund (OSFDX): 6% allocation to RAD and Dangerous rating

2) PowerShares Dynamic Retail (PMR): 3% allocation to RAD and Dangerous rating

Sam McBride contributed to this article.

Disclosure: David Trainer is long WMT. David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.