This report is one of a series on the adjustments we make to convert GAAP data to economic earnings. This report will focus on an adjustment we make to convert the reported balance sheet assets intoinvested capital.

Reported assets don’t tell the whole story of the capital invested in a business. Accounting rulesprovide numerous loopholes that companies can exploit to hide issues and obscure the true amount of capital invested in a business over its life.

Converting GAAP data into economic earnings should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

We’ve performed unrivalled due diligence on 5,500 10-Ks every year for the past decade.

Reserves are contra asset accounts that reduce asset values for probable future losses (in the case of inventory reserves or loan-loss provisions) or resolve the difference in accounting treatments (in the case of LIFO reserves). Reserves are for probable rather than actual losses. Since probable losses are calculated at management’s discretion, companies can use reserve accounts to manipulate earnings and the carrying values of the assets to which the reserves apply.

Inventory reserves are included in our calculation of invested capital. We also add back the change in reserves to net operating profit after tax (NOPAT), which we covered in a prior report.

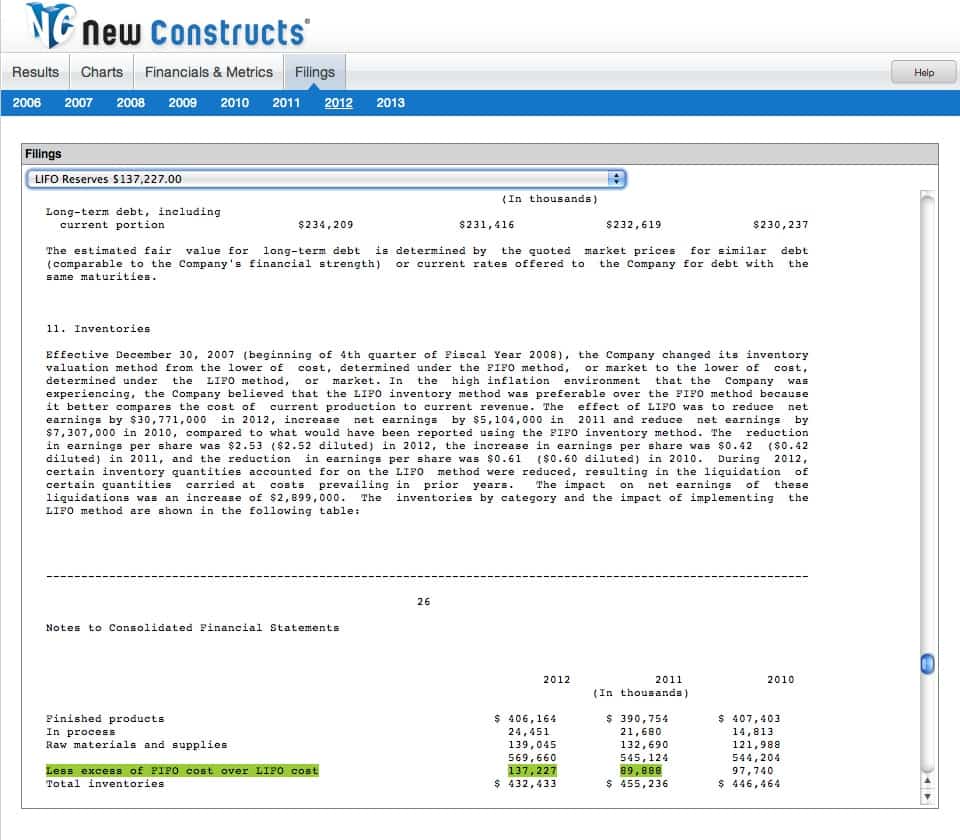

Accounting standards allow companies to choose how they expense inventory when it is sold, which means different expenses are reported when companies choose different accounting methods. To ensure comparability of companies using different accounting methods, our models convert all companies to the FIFO (First In First Out) method of inventory accounting by including the LIFO Reserve (the difference between the LIFO and FIFO method) in invested capital. LIFO reserves are found almost exclusively in the footnotes (see an example from SENEA).

{kind=link}

Without careful footnotes research, investors would never know that total assets exclude a significant portion of reserves due to loss provisions and alternative accounting practices.

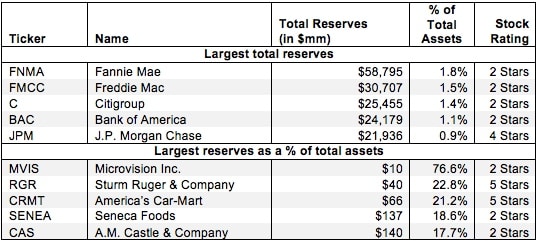

Figure 1 shows the five companies with the largest total reserves included in invested capital in 2012 and the five companies with the larges reserves as a percent of total assets.

Figure 1: Companies With the Largest Total Reserves Added Back to Invested Capital

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

The first 5 companies in Figure 1 are exclusively large financial companies, as these companies engage in a large amount of lending and therefore require significant loan-loss reserves. However, they are far from the only companies that are affected by total reserves. In 2012 alone, we found 991 companies with reserve adjustments that decrease asset values, totaling over $324 billion and 7 companies with reserve adjustments that increase asset values (when FIFO is lower than LIFO) totaling over $455 million. For all years, our database contains 11,452 instances of reserve adjustments that increase asset values totaling over $2.6 trillion and 147 instances of reserve adjustments that decrease asset values totaling over $4.2 billion.

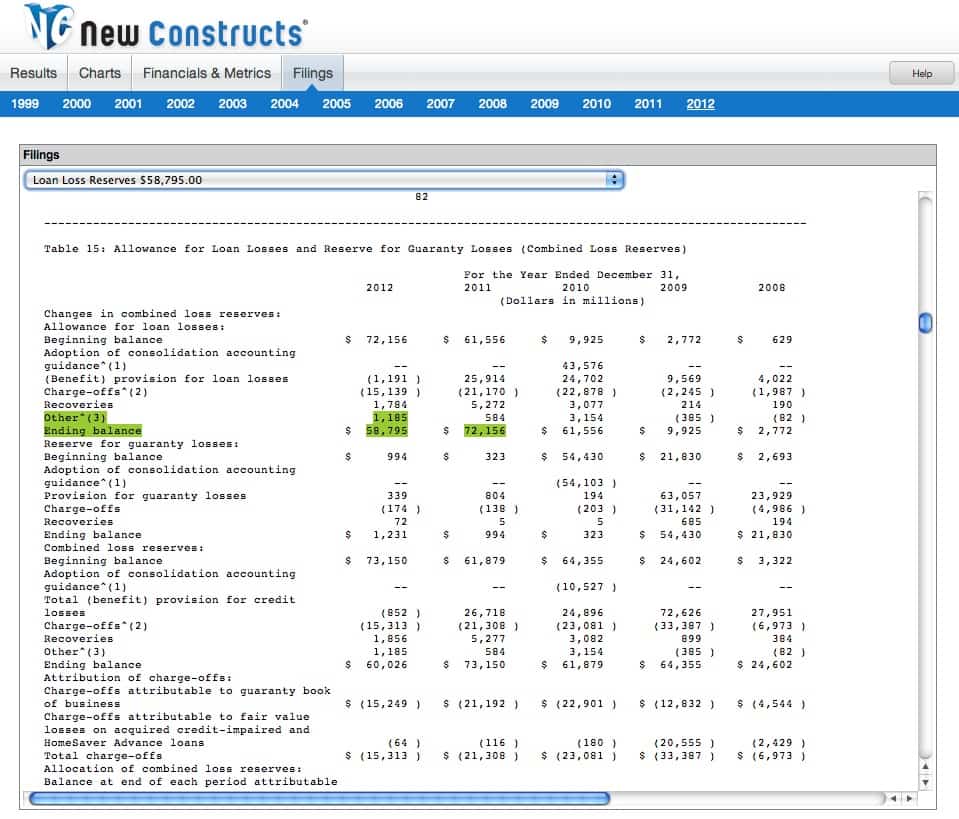

Since adding back reserves increases invested capital, companies with significant reserves will have a meaningfully lower return on invested capital (ROIC) when this adjustment is applied. Case in point: Fannie Mae (FNMA). FNMA had a loan-loss provision of over $58 billion in 2012. Without adding back these reserves, FNMA would have an invested capital of only $29 billion and an ROIC of over 11%. Adding back these reserves brings FNMA’s average invested capital up to nearly $88 billion and it’s ROIC down to 4%. By taking a large loss on loans in previous years, FNMA is able to ensure subsequent years seem more profitable than they really are.

{kind=link}

Investors who ignore reserves are not holding companies accountable for all of the capital invested in their business. By adding back reserves to invested capital, one can get a truer picture of the value that management is creating for shareholders. Diligence pays.

Sam McBride contributed to this report

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.