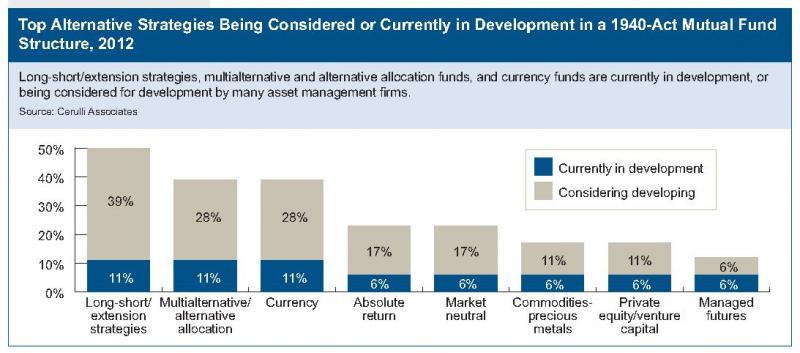

Over the last couple years, we’ve written time and again about the mainstreaming of alternative investments with the rise of alternative mutual funds and ETFs. But data released by Cerulli Associates gives even more credence to the argument that alternative mutual funds will one day likely stand side-by-side with traditional investments such as stocks and bonds.

Over the last couple years, we’ve written time and again about the mainstreaming of alternative investments with the rise of alternative mutual funds and ETFs. But data released by Cerulli Associates gives even more credence to the argument that alternative mutual funds will one day likely stand side-by-side with traditional investments such as stocks and bonds.

According to a Cerulli report, 70 percent of retail asset managers said they believe alternative products to be as important as or more important than other initiatives. As it is now, alternative mutual funds account for 2.8 percent of overall mutual fund assets. But Cerulli projects this to grow to 9.7 percent of all mutual fund assets in five years, and 15.8 percent of assets in 10 years.

High-net-worth wealth providers, such as Tiedemann Wealth Management or Convergent Wealth Advisors, are expected to boost their allocation to alternative investments from 17 percent now to 20.3 percent in three years, Cerulli said.

There’s no doubt investors today are still looking for a way to manage downside risk in their portfolios, especially after a more traditional method—diversification—failed during the 2008 market meltdown. The demand is there—alternative mutual funds have grown from $30 billion in assets in 2003 to $214 billion at the end of 2011.

But I don’t think we should be dropping ‘alternative’ from the name of such products just yet. While, indeed, these funds have grown their assets significantly over the last 10 years, it still represents a small portion of the overall retail market. According to Cerulli, alternative mutual funds made up only 3 percent of total mutual fund assets at the end of 2011, and grew only 2 percent last year.

Further, asset managers still face challenges to capitalizing on investors’ demand, Cerulli said:

Indeed, Cerulli has heard time and again that the primary challenges for managers looking to capitalize on the demand for alternatives stem from creating trusting relationships with financial advisors and providing them education on effectively employing alternatives within their clients’ portfolios—this is not a “build it and they will come” scenario.

Speaking of Field of Dreams.

Also, I don’t see how we can start calling them mainstream when many of these funds are still very young and untested.

Many of these funds were launched after the market crisis and have yet to establish a three-year track record. Given the unique strategies many of these firms are attempting, establishing proven success is often a necessity before significant assets can be gathered.

Don’t get me wrong. Many alternative funds have very good track records, and the 40-Act structure can offer investors greater liquidity, transparency and lower fees. There are many advantages, and I expect to see growth and demand accelerate. But I think it requires more homework and time before we can call these funds, “mainstream.” What do you think?