This report is one of a series on the adjustments we make to convert GAAP data to economic earnings.

Reported earnings don’t tell the whole story of a company’s profits. They are based on accountingrules designed for debt investors, not equity investors, and are manipulated by companies to manage earnings. Only economic earnings provide a complete and unadulterated measure of profitability.

Converting GAAP data into economic earnings should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

We’ve performed unrivalled due diligence on 5,500 10-Ks every year for the past decade.

We make two historical adjustments to a company’s invested capital related to goodwill. The first deals with unrecorded goodwill.

Goodwill arises when one company pays more than the market price for another company. Prior to 2002, the recognition of goodwill (as well as the fair value of the assets acquired) could be avoided using the “pooling of interests method” of accounting for acquisitions or mergers. Under this method, only the book value of the assets of the company acquired is added to the books of the acquiring firm. There is no accounting record of the actual purchase price paid, which often exceeded the market value. Any premium paid for the company over its market value was “unrecorded” along with the fair market value of the assets acquired.

Firms liked this pooling method because it helped them keep EPS higher by avoiding goodwill amortization expenses. ROEs were higher too as only the book value of assets acquired got added to balance sheets.

To reverse the discrepancy between the accounting for companies that used the pooling method instead of the purchase method of accounting, we add the difference between the purchase price of the acquisition and the book value of assets acquired to the invested capital of all companies that did pooling acquisitions.

The second historical goodwill adjustment we make to invested capital deals with accumulated goodwill amortization. Accumulated goodwill amortization is the gross amount of goodwill amortization that has been expensed over a company’s lifetime. Prior to the introduction of SFAS 142 in 2001, goodwill was amortized using straight-line depreciation. After SFAS 142, the system of goodwill impairment is used to value intangible assets and reduce their value via an annual test. Although goodwill amortization no longer takes place and the accumulated amount no longer changes, we add back accumulated goodwill amortization prior to SFAS 142 to a company’sinvested capital calculation.

These adjustments ensure an apples-to-apples comparison between companies that recorded acquisitions under the pooling versus the purchase methods. They also provide a far more accurate measure of the amount of capital that has gone into businesses, which means a more accurate invested capital and ROIC.

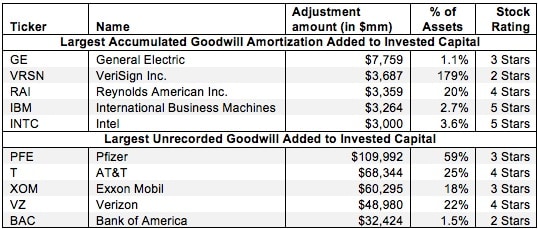

For example, VeriSign Inc. (VRSN) has accumulated almost $3.7 billion in goodwill amortization over the years. We add back this asset to provide a more accurate picture of the total amount of goodwill and capital invested in VRSN over its lifetime. This adjustment raises VRSN’s invested capital in 2012 from $15 billion to almost $19 billion.

Figure 1 shows the five companies with the largest gross values of accumulated goodwill amortization and unrecorded goodwill adjusted out of invested capital for 2012.

Figure 1: Companies Most Affected By Goodwill Amortization and Unrecorded Goodwill in 2012

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

However, these companies are far from the only ones affected by accumulated goodwill amortization and unrecorded goodwill. The accumulated goodwill amortization adjustments apply to 1041 different companies, while unrecorded goodwill adjustments apply to 281 different companies. Our database contains a total of over $10 trillion in unrecorded goodwill adjustments and over $1 trillion in goodwill amortization adjustments across more than 3000 companies.

Though the addition of accumulated goodwill amortization and unrecorded goodwill can increaseinvested capital and lower ROIC, it does not always mean the company’s stock will earn an unfavorable rating. For instance, Verizon (VZ) still earns an Attractive or 4-star rating despite its almost $49 billion in unrecorded goodwill added back to invested capital.

In other cases, however, overlooking unrecorded goodwill can result in artificially lower invested capital, which in turn overstates ROIC and can make a stock look undervalued. Case in point: Pfizer Inc (PFE). Per Figure 1, Pfizer had a total of $110 billion in unrecorded goodwill added back to invested capital in 2012.

PFE has owed much of its growth since 2000 to a number of high-profile mergers, including Warner-Lambert in 2000. This $90 billion deal was Pfizer’s last (and most expensive) merger before the elimination of the pooling method of accounting. This purchase in 2000 helped contribute to PFE’s $110 billion in unrecorded goodwill over the years.

Last year, PFE’s invested capital was $250 billion, but without the addition of this unrecorded goodwill, it would have been just $141 billion. Using this unadjusted invested capital, PFE’s return on invested capital in 2012 would be 10%, but with this adjustment it comes out to under 6%, just shy of half of PFE’s unadjusted ROIC value. This lower ROIC helps explain why PFE earns my Neutral 3-star rating. Diligence pays.

André Rouillard contributed to this report.

Disclosure: David Trainer and André Rouillard receive no compensation to write about any specific stock, sector, or theme.